A man and woman looking through a magnifying glass at financial documents over an abstract skyline background. The people & magnifying glasses, financial documents, and the background are on a separate labeled layers.

A man and woman looking through a magnifying glass at financial documents over an abstract skyline background. The people & magnifying glasses, financial documents, and the background are on a separate labeled layers.

Liquidity forecasts are a vital tool that treasury can use to support management decision-making. To ensure organizational leaders are equipped to respond effectively and promptly to changes in strategy and business outlook, the corporate treasury team must base their forecasts on robust and dynamic processes. However, like all finance processes, forecasting is vulnerable to legacy "drag"—including one-off reporting add-ons that become permanent and manual workarounds to deal with offline data manipulation. These can reduce the team's efficiency and focus. The problem is exacerbated in environments where teams are constantly being asked to do more with less.

Some current economic trends are reinforcing the need for forward-looking insight, most notably rising costs and volatility resulting from interconnected supply chains in a less-certain world, as well as increasing employment expenses. On the other hand, technology developments offer opportunities for improving efficiency by leveraging more dedicated (and cheaper) applications, as well as artificial intelligence (AI).

Taken together, these trends indicate that it's a good time to re-evaluate corporate liquidity forecasting processes. Are they fit for business purpose, and do they deliver value for the money in terms of effort versus benefits? A two-stage approach enables a treasury function to review current processes: first, a top-down definition of the overarching framework that re-examines the fundamentals of the forecasting process, and second, a bottom-up review of the supporting infrastructure. The treasury team can complete both steps while retaining a pragmatic approach to matching capabilities to requirements.

Design a 'Best Fit' Forecast Framework

First, it's important to recognize that there is no universal best practice for cash forecasting. Specific business needs are driven by the organization's underlying cash dynamics, as well as its risk appetite, operational structures, geographical spread, technology environment, and banking arrangements. All these factors can differ even among similar-sized businesses within the same industry. Instead of pursuing an amorphous best-practice model, a treasury team should look for a "best fit" approach—finding what will work best for their organization.

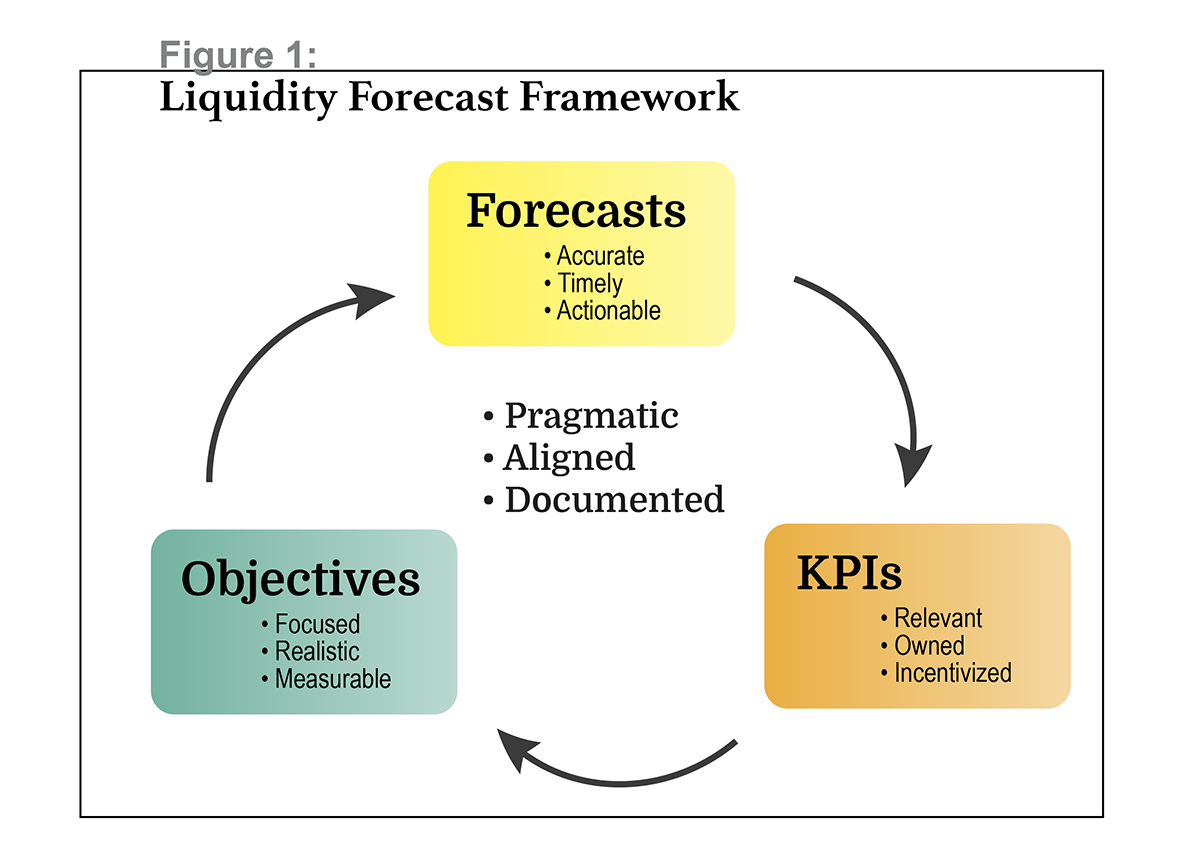

This approach goes back to first principles: The forecast's outputs should support relevant business objectives, and should be measured against appropriate key performance indicators (KPIs). Figure 1 illustrates such a framework, which has three core components.

1. Objectives: What is the forecast for? The first step in evaluating a cash-forecasting process is to set out the objectives behind the forecast. This may seem obvious, and it's true that core objectives will normally focus on maintaining adequate liquidity over given time horizons, as well as efficient use of cash assets. However, to ensure the end design aligns with overall business strategy, forecasting-process planners must consider broader business goals and policies that may relate to cash and debt. For example, a company's liquidity forecast may need to identify and manage foreign exchange (FX) transactional exposures, address the organization's ability to meet financing covenants, evaluate financial counterparty risk, and even take into account corporate policies in relation to who should "own" cash—e.g., should liquidity decisions be centralized or decentralized? The list will necessarily be organization-specific.

For clarity and focus, it may be helpful to prioritize and sort objectives into buckets—for example, labeling business-critical items, such as avoiding breach of a debt covenant, as "necessary"; tagging performance-improvement targets like reduction of idle cash as "efficiency" goals; and identifying longer-term objectives, such as lining up strategic funding, as "opportunities." To be useful, the objectives must be pragmatic—both realistic and achievable—and must relate to measurable outcomes. This will naturally help to identify appropriate KPIs in the next step.

Defining a forecast's objectives is the fundamental starting point for the framework design, and investing adequate time and effort up front will ensure that it lays a robust foundation for the resulting forecast. The final list of objectives should have board-level input and approval.

2. KPIs: How do we measure the effectiveness of the forecast in supporting achievement of our objectives? The next element of the framework is determining relevant KPIs for the liquidity forecast. These metrics should serve two purposes: one, to measure progress against objectives and thus inform decision-making; and two, to determine whether the process is functioning as intended (e.g., evaluate the timeliness and accuracy of forecast data to indicate whether improvement is needed). The KPIs should be explicitly linked to the defined objectives in order to demonstrate how business goals are embedded within the process.

Next, the treasury team needs to create specific performance targets for each KPI. These targets are typically defined as threshold limits, range bands, and the like. They should ideally involve time-horizon–based parameters to enable appropriate and timely management action. Each should be assigned to a named business owner to ensure it will get traction, and ideally it will also come with incentives for achieving the targets. After all, what gets measured gets done—especially if it's recognized.

For more complex organizations, the KPIs and targets may be cascaded down the business hierarchy. Note, however, that if such a hierarchy of targets is not carefully structured, it may reduce accountability at the overall level. Designers of the liquidity-forecasting process must also take care to ensure that potentially conflicting KPI targets are effectively balanced—for example, liquidity buffer vs. cash management efficiency—so that the forecast does not lead to unintended results.

One common mistake many organizations make is to regard accuracy as an objective rather than a KPI. There is little point in pursuing greater accuracy unless that improvement will drive effective action. Accuracy, measured via variance analysis, is a vital KPI in assessing the forecast's reliability, especially over a limited time horizon; variance analyses can clarify for treasury how far out the numbers can be trusted. Such an analysis can also help pinpoint which elements of forecast data may need attention.

Investing time and effort to improve accuracy is worthwhile so long as doing so genuinely improves confidence in decision-making, enables extended investment horizons, or leads to other desired results. Keep in mind, though, that increases in accuracy are eventually subject to the law of diminishing returns.

3. Forecasts: What outputs do we require to enable decision-making that supports our objectives? The cash forecast's outputs should be directly relevant to its objectives and should feed into the desired KPIs.

A treasury team defining the dimensions of their cash forecast should consider questions including:

- Reporting level: Can the forecast be matched to business accountability?

- Currencies (and conversion rates to be used, if applicable): Is there a reporting threshold?

- Reporting scale: Does the forecast effectively balance materiality vs. transparency?

- Forecast time horizon: Does it provide enough forward visibility, while also aligning with decision-making activities such as the corporate investment horizon?

- Forecast time buckets (e.g., first week by day, remainder by week): Is this granular enough to support finetuning management action and to meet other objectives?

- Frequency of reforecast: Does this provide sufficient reaction time for changes?

- Core forecast outputs (e.g., net liquid funds): Do the outputs relate directly to KPIs and accountability?

- Component forecast line items: Do the included line items align with the business's main cash drivers, providing visibility over key indicators for remedial action where required?

Since the dynamics underlying the liquidity forecast will differ between organizations, the desired forecast outputs will likely be business-specific. However, treasury groups need to be sure to avoid the temptation of data overkill. For example, consider: Does the forecast need to be broken down by bank account, when cash concentration structures allow cash management at the pooling level? Too much unnecessary granularity can create inefficiencies, both in resources to support the process and in wasted effort if the information is not actually used.

One area that requires consideration throughout the evaluation process is the organization's definition(s) of "cash." Depending on the time horizon and objectives, this could range through actual bank balances (as opposed to the cash book), cash headroom, and net debt. The core forecast outputs should meet all the company's required definitions.

Once the treasury team has fully defined and rationalized the outputs of the liquidity forecasting process, they may see an opportunity to combine separate forecasting processes. For example, splitting out the cash forecast by currency could enable both liquidity and FX transaction exposures to be managed from the same dataset, provided the forecast horizon is sufficient. In this case, consolidating forecasting processes across liquidity and FX might improve efficiency and reduce the chance of inconsistency between forecasts. It's not uncommon for parallel and overlapping forecasts to create confusion; if outputs disagree, that can lead to divergent management responses, and understanding differences—which version of the truth is correct—may require extra effort.

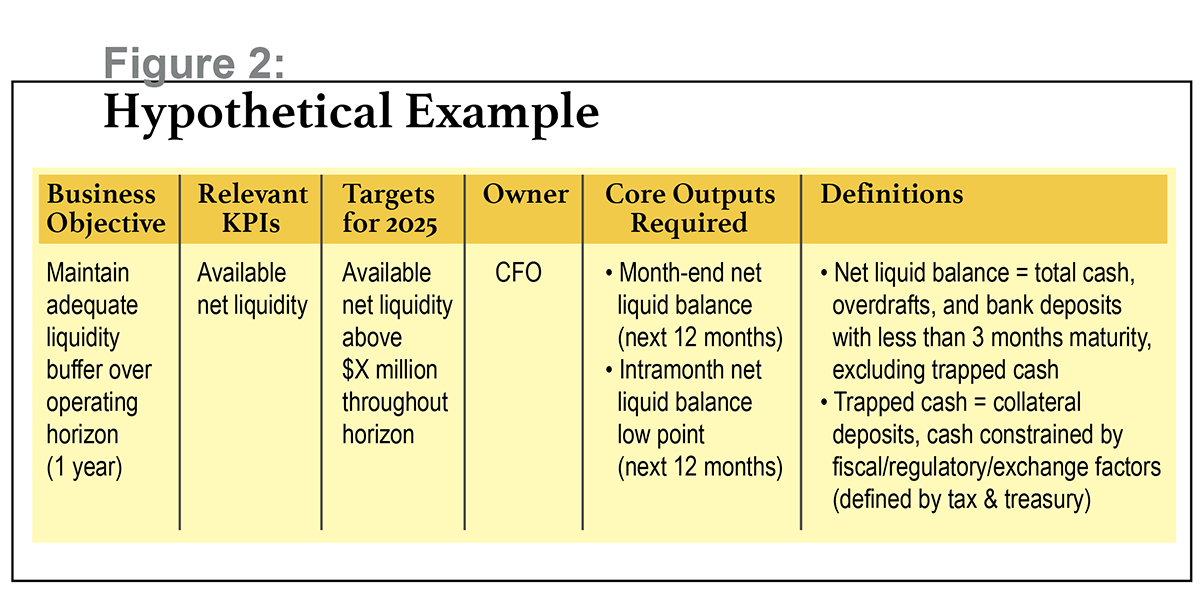

Taking these steps to design a "best fit" liquidity forecasting framework will help treasury ensure the framework's components are consistent and aligned. It will also provide a clear set of output requirements that the liquidity forecasting process needs to meet (see Figure 2)—requirements that should be both documented and communicated to ensure organizational engagement.

A robust liquidity forecasting process requires additional control features, including segregation of duties (e.g., preparation vs. review) and change-control procedures. However, forecasting processes are dependent on the capabilities of the supporting infrastructure.

A review of the organization's existing infrastructure forms the second stage of the assessment. For more on how to conduct this review, look for the second article in this two-part series, which should publish next week.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.