Wall Street

Wall Street

Investors looking to protect themselves against corporate defaults are helping drive record trading volumes in credit derivatives, as the war in Iran fuels fears of a global recession and artificial intelligence (AI) rattles once-safe industries.

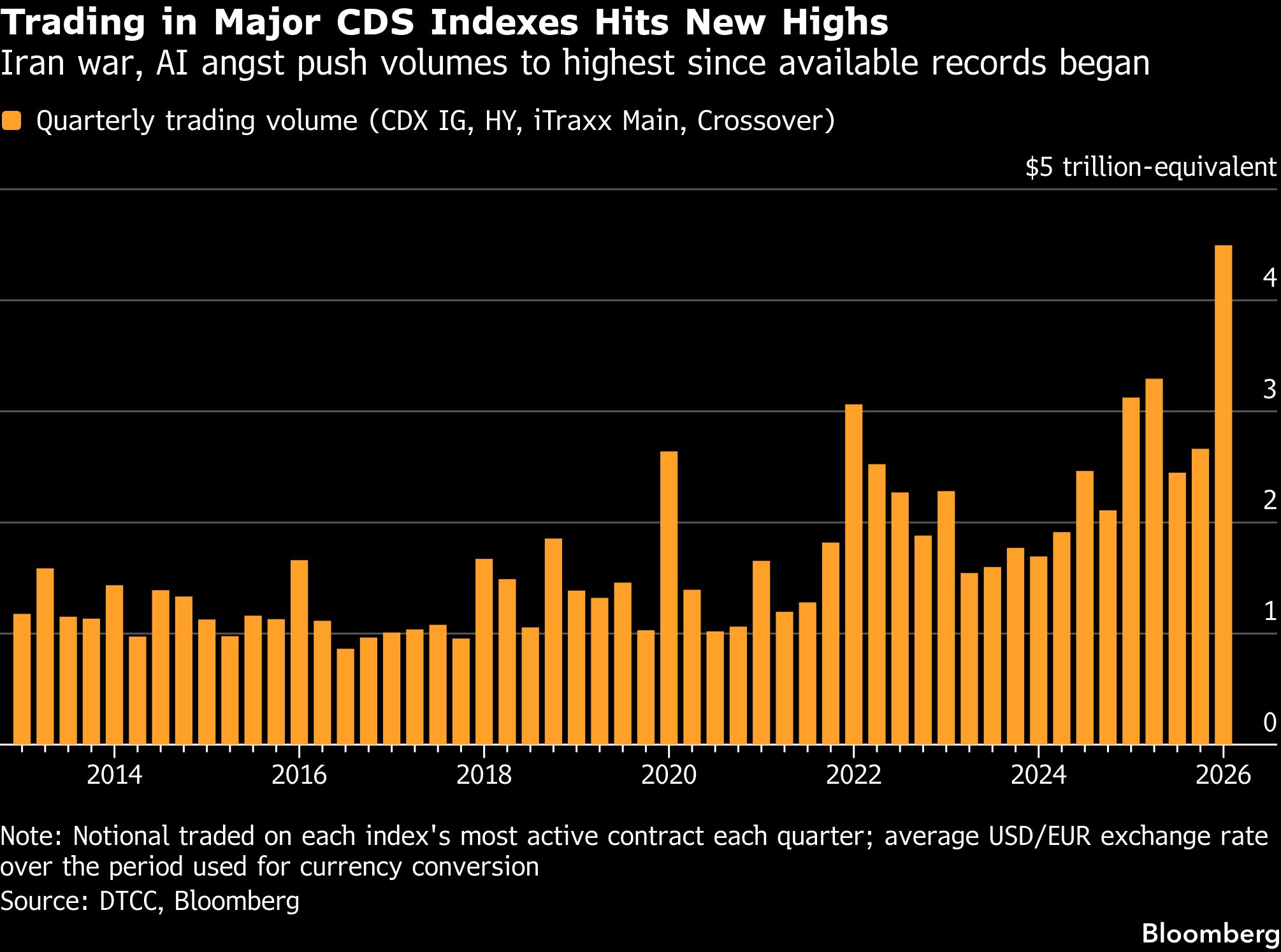

Trading volumes for the most active derivatives that protect bundles of high-grade and junk-rated bonds in the United States and Europe surged to almost $4.5 trillion in the first quarter of the year, according to DTCC data compiled by Bloomberg. That's 36 percent higher than the previous record set by credit default swap (CDS) indexes when U.S. President Donald Trump unleashed trade tariffs in April last year.

Global gauges of credit risk eased significantly this morning following Trump's latest comments that the conflict may end within the next two to three weeks. The sharp gyrations in the indexes underscore the extent of the volatility in trading.

"Every market participant is forced to hedge against two mutually exclusive scenarios simultaneously: a full-scale war and a diplomatic breakthrough," said Elena Nefedova, head of the investment office at Astero Falcon.

Even before the conflict put a chokehold on the flow of energy products, credit investors were fretting about the potential for AI to shake up whole sectors of the economy—and the possible impact on companies' ability to service their debts.

Heavy CDS trading "reflects the high level of uncertainty in the market," said Peter Kaufmann, senior analyst for corporate bonds at Erste Group Bank. "Nobody can really estimate the final fallout of the conflict and how long it will take to resolve some of the situation."

CDS indexes are the most liquid instruments in the entire market for company debt, with tens of billions of dollars of risk routinely changing hands on a daily basis. They work by providing a payout in the event of a corporate default, making them a traditional hedge for corporate portfolios. But investors also use them to speculate on the direction of the broader market, especially when conditions make it hard to immediately buy or sell a big part of their portfolio.

That's what has been happening in recent weeks. After a nine-month rally in global credit markets, the Iran war and AI concerns are prompting traders to reduce what's effectively a giant long position, worth hundreds of billions of dollars.

CDS indexes are bearing the brunt. Net positioning on the latest version of the iTraxx Europe index—which tracks the credit risk of a basket of major European firms—recently turned bearish for the first time since 2018, according to Barclays strategists. Also contributing to the trading volumes is the fact that CDS contracts are rolled into new ones every six months, traditionally boosting activity in the first and third quarters. Meanwhile, the big long position on its North American counterpart—the CDX.NA.IG index—has shrunk by tens of billions of dollars.

It's a dramatic about-face compared with just a few weeks ago, when analysts had to get creative with low-cost hedging ideas in a bid to get investors to spend money on credit protection at all.

From last May until the start of the war in the Middle East, the North American high-grade CDS index moved by just 0.7 basis point (bps) each day, on average, data compiled by Bloomberg show. That shot up to 2.2 bps in March.

Hedging is also heating up in the leveraged loans market, where so-called total return swaps remain one of the most liquid ways to buy and sell protection. Hedge funds and investors can use the derivatives to bet against the asset class without having to own the underlying loans.

To be sure, the cost of default protection—both in Europe and the U.S.—remains well below the levels notched during the previous energy and inflation scare in 2022 and hasn't matched the highs seen during Trump's shock tariff announcement. Still, with the war still dragging on and the Strait of Hormuz remaining shut, there's no sign markets are through the worst.

Markets have rebounded today, extending gains after Trump said he foresaw ending the war on Iran within two to three weeks, suggesting the U.S. has largely accomplished its military goals. At the same time, the prospects for reopening the Strait of Hormuz are uncertain.

"Investors buying protection is a great way to hedge a really damaging move," said Juan Valencia, a credit strategist at Societe Generale. "The conflict in Iran is putting pressure on all risky assets and safe havens and everything in between."

————————————————————

Copyright 2026 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.