Introduction

|Today's banking experience is vastly different for corporationsthan it has been in the past. Customer experience, rather thanproduct functionality is a key focus for banks today. Whilecustomers can use any number of channels to access the bank, theindustry is seeing more use of the web, mobile, and tabletinterfaces as the lines blur between how personal and commercialusers interact with the bank via the web.

|Over the past decade, treasury management services have becomemore commoditized, pushing banks to focus on a key point ofdifferentiation, the client experience. This focus not onlyenhances the banks' relationship with corporate clients, but alsodrives revenue and customer retention, particularly throughservices offered through the bank. Given these points of focus,banks can use these tangible benefits to build a business case forinvestment in the web portal.

|In this light, the web portal has become an essential channelfor both providers and corporate clients. Treasury Strategies hasseen a decline in corporate requests for operational site tours, anuptick in requests for detailed demonstrations of the bank's webchannel, and a higher degree of rigor in the testing of files andmessage integration. Corporations are seeking efficiency and aremore satisfied when the online channel allows them to achievehigher efficiency. With the web portal becoming “the face of thebank,” increased investment is directed to the online channel.

|In this white paper, we will discuss the full scope of the webportal and treasury services/cash management today, corporate needsand benefits, the business case for the build-out of the commercialweb platform, and the future of web portal functionality.

|Evolution of Treasury Services and Cash Management:Treasury 3.0

|The scope of treasury services and cash management is evolving.Historically, both banks and corporations defined theirrelationship on a transactional basis. The bank had products thatallowed corporations to complete transactions around payables,receivables, and credit. Corporations relied on the banks to ensuretheir transactions occurred and provided the credit needed toenhance their business operations. Today, banks look to providesolutions, and the scope has expanded to include three primarytypes of services and revenues:

- Liquidity Management Revenue: account services,payables/receivables/liquidity/card products, float

- Deposit Revenue: spread revenue from current accounts/operatingbalances and savings/short term investments

- FX Payments and Trade Revenue: FX spread generated from paymenttransactions, import/export letters of credit, document managementand collections, credit spread

Additionally, banks are expanding their services globally tosupport corporate growth into emerging markets. The web portaltechnology is essential in this strategy — it allows subsidiariesand employees all over the world to access the same screens,information, and rely on consistent support. Today even smallercompanies have a global reach, and banks must expand their servicesto meet the demands of this growing segment.

|This evolution from products to solutions mirrors the evolutionof the relationship between banks and their clients. TreasuryStrategies terms this development “Treasury 3.0.” Banks have gonefrom accommodating clients and their transactional needs tocreating comprehensive solutions and serving as an advisor toclients. The way that banks have provided these services to clientshas changed over time as well. Historically, banks built up systemsby functional areas of the bank, as needed. Over time, acomprehensive bank-wide treasury services and cash managementsystem developed and continues to evolve.

|

Web Portal Transformation

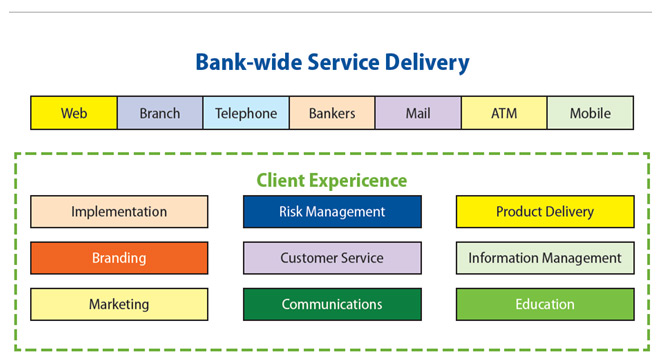

|With these changes in services and relationships comes a changein how clients interact with the bank. Historically, clientsinteracted with their banks by coming into a physical branch orreaching out to their relationship manager or service team on aperiodic (sometimes daily) basis. This has drastically changed, andtoday, clients' primary method of interaction with their banks isthrough the web portal. This fundamental shift is due to multiplemarket forces. Clearly, the availability of technology is a strongforce in the development of the web portal. Additionally, retailcustomers have increased their use of the web portal. Thiscomfort in using technology instead of a representative at the bankbranch on the retail side has spread to the commercial space. Thus,retail clientele have shaped corporations' usage of the web channeland corporations prefer to use the web channel today versusprevious methods of interaction.

|Corporate clients are able to use the web channel for the fullscope of their relationships with their banks. This includesproducts and services (credit, trade, liquidity, payments, info,servicing) and also integration and interaction with the bank(servicing, implementation, training, industry knowledge).

|For corporations, the web portal has increased in popularity dueto the convenience and efficiency it allows. Historical pain pointsincluded issues around disparate business units and geographiesthat were unable to provide reliable information. Today, the webportal is critical in solving these issues for corporations. Itallows corporations to have one integrated platform through whichto do business around the world.

|Key benefits include:

- Accurate, comprehensive data: Clients canaccess data for their business worldwide and know that it iscorrect

- Real-time information: Being able to accessreal-time data is a huge advantage for treasurers who are nowexpected to report on a real-time basis to senior management

- Customized reporting and analytics: Today, theweb portal offers advanced analytics and the ability for users tocustomize reports as needed

- Increased efficiency: Access to thisinformation and reporting is a huge time-saver for corporatetreasury departments who, with more responsibility, are alwayslooking to streamline processes

- More flexibility: The web portal allowscorporations to go online and access their information at all timeswhich gives them the flexibility to conduct work outside ofbusiness hours when a branch is open

- Greater insight: Banks are able to provideanalytics through the web portal that give corporations fast andeasy access to insight into their cash positions and liquidity

- Global integration: The web portal serves as aplatform that allows banks to give their customers access toproducts, services, and features across the world

Corporate Online Treasury Services and Cash ManagementNeeds

|Much of banks' evolving offerings have been a reaction tocorporate needs. When evaluating “Treasury 3.0” from a corporateperspective, Treasury Strategies observes that corporations' needsused to be based around data, evolving to information, and todaymoving to intelligence. The word “intelligence” implies thatcorporations are demanding functionality such as dynamicinformation reporting and analytics/tools to optimize cash. Also,clients expect banks to provide a broader array ofsolutions/information in an integrated fashion. This includesnon-financial activities like electronic administration, mobileintegration, security features, social networking, and customerservice. All of this is more easily accessible through a webportal.

|Corporations' need for intelligence converges with theirliquidity management and cash pooling needs. Intelligence allowsthem to clearly view their liquidity position and pooling allowsthem to efficiently manage their cash. Intelligence is especiallyneeded to manage global needs and the web portal's ability todeliver a global view to users all over the world is critical tocorporations.

|Bank Online Channel Enhancements

|Banks have, and are responding to, corporate needs with advancedweb portal functionality. One example is online management andreporting on pooling (physical and notional), which is the use ofsurplus cash balances to fund any deficits and maximize efficientuse of funds. The web portal is the ideal channel for managing theflow of these funds and the administrative rules alongside. Thistype of online management is not only ideal for corporate clients,but helps banks to reduce back-office support costs as well. Forexample, eBAM, or electronic bank account management, allowsclients to automatically generate documents and workflows that makethe process of managing accounts more efficient.

|While corporations are looking for this robust functionality,when taking a holistic view of the web channel, three othercomponents come into play: a dynamic accessible interface, a singleplatform that can deliver insights and expand flexibly, andintegration.

|Web 2.0 functionality is frequently used to refer to a widevariety of new online functionality and user experiences. The threeprimary components are a dynamic, customizable user interface, aweb chat, and online self-service. Banks are providing all of thisfunctionality to address corporate needs in a single platform. Theimportance of integration is explored in the following section.

|Bank Integration Trends

|Integration is a critical theme in supporting the web channel.There are different kinds of integration: integration within bankchannels, across geographic data, and between corporate technologyand bank interfaces.

|Banks are putting emphasis on consistency and integration acrossall channels of interaction with the bank. If the web portal is the“face” of the bank, the bank wants to ensure that “face” looksconsistent no matter what channel of interaction a customer usesand no matter where the user is physically located when accessingthe web portal (e.g., online, mobile, app, tablet, etc.).

|Banks also have to ensure all systems with client data are fullyintegrated. If a customer goes into a branch, goes to an ATM, oraccesses the web portal, they must see the exact same informationregarding their accounts and services.

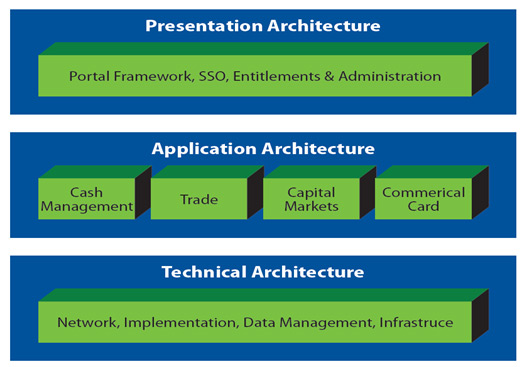

|Additionally, banks are developing their web portal such that itintegrates with clients' enterprise resource planning systems (ERP)and treasury and risk management systems (TRM). This allowscorporations an even more accurate and integrated view.

|Banks are taking integration a step further within their ownorganizations. Banks are integrating product capabilities to allowfor a larger scope of service offerings. FX and payments areconverging, and banks are moving towards the integration ofliquidity tools (cash forecasting/ positioning, optimalconcentration) with trade and post-trade solutions (exposuremanagement/reporting). Liquidity is “king” and the integration ofthese tools allows corporations to fully manage their cashexposures. Furthermore, banks are looking to integrate across thecustomer experience — including sales, implementation/onboarding,transacting, servicing, and relationship management. Integrationimplies that all systems that support these groups are seamless (atleast in how the client views them) and that they are able toprovide consistent data to the client. Today, this is still indevelopment at banks but is a focus, because it will allow forinternal efficiencies.

|Not only are banks focusing on integration with corporations andinternally, they are also very interested in how outside vendorsare integrated with their systems. Bank needs vary based on theirsize and target IT portal architecture, and vendors must offerflexible support based on the unique needs of each institution.Smaller financial institutions prefer portal-like capabilities andcustomization through the presentation layer through a singleapplication vendor. However, larger banks have an integratedapplication and presentation layer and are looking forbest-in-class vendors to “plug-in” easily.

|

Bank Investment in the Web Channel

|Banks are significantly investing in the web channel due to itsincreasing importance and the fact that it is the primaryinteraction channel with clients. Additionally, they are focused onthe global capabilities of the channel because corporate needs arecomplex and clients are interested in moving into emergingmarkets.

|Treasury Strategies has observed that banks invest about 8.5% oftreasury services and cash management revenue (TM fee and spreadrevenue) on IT, on average. A little under half of this investment(45%) is spent on discretionary spending, of which roughly halfgoes to the web channel and supporting infrastructure — essentiallya 2% spend of annual treasury services and cash management revenue.With all the varying pressures on IT departments, this is clearly avital part of bank strategy.

|Bank Business Case

|Given the bank investment in the web portal, a question arises:What benefits are identified and included as part of a businesscase for this investment? The web portal is an important channel ofthe bank but it is often hard to “sell” to internal stakeholders.The web portal has been around for only a decade and the benefits,in some cases, are difficult to quantify. Clearly, the web portalallows banks to strengthen their relationships with corporationsand better solve their clients' complex needs. In addition,Treasury Strategies has observed four key tangible benefits of webportal investment to banks:

|- Share of Wallet: Banks have an opportunity toincrease share of wallet and market penetration. By driving moretraffic to the web channel and integrating services, clients willbe encouraged to use a broader and deeper array of services. If theweb channel is easy to use, customers will be more likely toincrease their use of products and services.

- Increased Fees: The bank has an opportunity toincrease fee-based income (versus spread income) by delivering newcapabilities, reports and analytics to clients. With this increasein product and service usage, the bank will see an increase in feeincome.

- Reduce Back Office Costs: Banks have anopportunity to reduce back-end costs of sales, implementation,training, transacting, servicing, and relationship management. Theweb channel provides further opportunities for customers toself-service, driving down costs for banks. Training andtransacting can be done online, versus with a bank representative,which results in further cost savings. Technology and onlineself-servicing have allowed banks to scale their business to thesmall- and medium-sized enterprises that are recognizing revenueopportunities globally, particularly in the emerging markets.Overall, the SaaS, or software as a service model can deliver thesame requirements, at a lower cost to the bank.

- Change Agent: The web channel is a changeagent, not just an enhancement to existing functionality. The webchannel can and does transform the relationship with the corporateclient by providing access and configuration of data unavailable inother channels, improving time to revenue, decreasing thevolatility of revenue and balances, and ultimately changing theoperating model of the bank to a more cost-effective model.

Bank Decision: Buy versus Build

|When evaluating the overhaul of an online platform or componentof a web platform, banks must decide whether or not to build thefunctionality with internal IT resources or look outside the bankand buy a solution from an outside vendor.

|Today, banks have many cost pressures and are looking to focuson their core competency, banking services. Therefore, banks tendto outsource new IT projects instead of developing newfunctionality in-house. This is due to the increasing pressure froma variety of market challenges for banks that include increasingclient sophistication, globalization, and technologicaldevelopments.

- Increasing Client Sophistication

- |

- Clients are demanding integrated solutions, and the historicaldevelopment of platforms is no longer sustainable for banks.

- In the past, business units have built up web platforms tosupport clients but these have not been integrated across the bank.Bank IT departments are less equipped to staff this new productdevelopment with all the demands on the group for maintenance ofsystems.

- Globalization

- |

- Additionally, treasury departments are being centralized inorder for corporations to achieve efficiencies in their globalbusiness. Banks are challenged to build a global solution on theirown.

- Technological Advances

- |

- Banks must keep up with vastly evolving technologicaldevelopments. Today there are a range of electronic channels andfile formats that banks must support. In addition, SWIFT corporateconnectivity is critical and non-bank competition isincreasing.

As the industry looks to the future, the emergence of SaaS fromvendors becomes increasingly important. The software is accessed asa web browser and it allows for a more efficient implementation andupdate process for banks. There is no need for physical deploymentor testing on individual computers, and information is storedsecurely using cloud technology. Such a solution can not only lowerall-in operating costs, but can speed time to market — a majorfocus of SaaS solutions is not just the outsourcing of relevantcosts, but also an emphasis on improving ease of integration.

|With the explosion of client requirements around the web, bothfunctional and non-functional, corporations need a bank partnerthat both offers this functionality and is nimble. Banks' abilityto address their clients' needs which are increasingly complex andglobal is challenging to do in-house, even if the bank is of alarger size. Banks, both small and large, need experienced vendorsthat can provide a web portal solution with a short time-to-market.Using a cost-effective vendor with expertise to build an onlinesolution can serve as a competitive advantage for banks.

|As a bank considers different vendors, factors to considerinclude:

- Practicality: A solution that closes currentfunctional gaps.

- Cost: A cost comparison between differentvendors (in conjunction with other factors) is important, but it'simportant to look at all-in costs, including support and ongoingdevelopment and maintenance.

- Single sign-on: A single, scalable platformthat can support a diverse customer base of high-end commercialclients as well as retail and small business clients.

- Platform architecture: Architecture alignswith the future state of the web platform. Banks may want thevendor to provide the portal architecture or, at minimum, may wantthe vendor to effectively integrate into the bank's target portalarchitecture.

- User interface: A cutting-edge delivery anddynamic user interface positions banks on the forefront of onlinebanking technology and conveys to clients that the bank isinvesting in its solution set.

- Innovation: Next generation web functionalityincludes intuitive user-driven customization and mobile/otherchannel integration.

- Viability: A vendor should have the financialstrength to remain strong so that it can support ongoingdevelopment of solution architecture and functionality.

Conclusion

|Banks need to continue to address the complex needs of theircorporations and need to do so through the most cost effective andclient-centric channel — the web. The evolution of the web portaland the deepened relationship between corporations and theirbanking providers is here to stay. Corporations find benefits in aninteractive web portal with reliable information and selfservicing, and banking providers are investing significantly tomeet those demands through a cost-effective platform, SaaS.

|As a bank looks to move forward with investment, keyconsiderations include:

- Define Bank Strategy of Differentiation

- |

- Bank needs to decide how to differentiate its web portal andensure that all channels are consistent in format andcapabilities

- Identify Scope of Online Solution:

- |

- Scope of the solution will be determined by the bank's strategyof differentiation

- Assess Key Functional Areas to Improve/Grow

- |

- Compare current capabilities to define scope and identify areasthat need development

- Prioritize Investment and Sequence Build-Out:

- |

- Prioritize necessary development and contract third party ifdecision is to “buy”

- Develop the Business Case for Investment

- |

- Document key drivers that will increase revenue and retentionwith the online solution

- Gather Executive and Organizational Support

- Drive Go-To-Market Strategy

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.