The Foreign Account Tax Compliance Act (FATCA) is a new set of U.S. tax rules that will affect many aspects of the day-to-day activities of the corporate treasury function. FATCA was enacted by Congress in 2010 to detect and deter tax evasion by U.S. citizens and businesses hiding money in foreign countries.

The Foreign Account Tax Compliance Act (FATCA) is a new set of U.S. tax rules that will affect many aspects of the day-to-day activities of the corporate treasury function. FATCA was enacted by Congress in 2010 to detect and deter tax evasion by U.S. citizens and businesses hiding money in foreign countries.

The legislation, which has a general effective date of January 1, 2014, is creating a new tax information reporting and withholding regime through which foreign financial institutions (FFIs) are expected to identify their U.S. account holders and report their account balances and other information.

For corporations with operations, activities, business partners, or counterparties outside of the United States, FATCA is creating an array of issues, starting with the fact that some of their entities may qualify as FFIs under the law.

FATCA Basics

FATCA is being implemented directly by the IRS and indirectly through a network of intergovernmental agreements between the U.S. government and certain foreign countries. Under this new regime, FFIs—which include non-U.S. banks, custodians, investment vehicles, and insurance companies—must report to the IRS or to the appropriate foreign government certain information regarding accounts held by “U.S. persons.” Failure by an FFI to provide such reporting will result in the imposition on the FFI of a 30 percent withholding tax on payments of certain categories of U.S.-source fixed or determinable annual or period income (FDAP), and eventually on gross proceeds from the sale of debt or equity interests in U.S. obligors or issuers. Interest and dividends are the types of FDAP most likely to be subject to FATCA.

Entities that make payments (either directly or indirectly) from sources within the U.S., which the law refers to as “withholding agents,” must also provide certain information to the IRS. Specifically, withholding agents may need to identify FFIs and certain non-financial foreign entities (NFFEs) that have substantial U.S. ownership. If an NFFE fails to provide the proper certification, or if an FFI is not compliant, the withholding agent is required to withhold a 30 percent tax on certain payments. The IRS is currently modifying tax withholding certificates, such as the Forms W-8, so that market participants can document their FATCA status to their withholding agents.

Information reporting under FATCA begins with certain data collected for year-end 2013. The withholding provisions of FATCA apply to payments made on or after January 1, 2014, although withholding on gross proceeds and certain foreign payments is delayed until 2017.

Information reporting under FATCA begins with certain data collected for year-end 2013. The withholding provisions of FATCA apply to payments made on or after January 1, 2014, although withholding on gross proceeds and certain foreign payments is delayed until 2017.

Due to the complexity of the rules, many entities have already begun assessing the impact of FATCA on their operations. However, many multinationals whose primary business activities are outside of the traditional financial services industry mistakenly believe that they will not be impacted by the law. Treasurers in these organizations may be surprised to learn that FATCA could have a substantial impact on how they do business, both within and outside the United States.

The Hunt for FFIs

Financial services companies will bear much of the burden of FATCA, but the new regime will affect most multinationals in one way or another. As a starting point, many treasurers will be surprised to learn that their global affiliated group may contain entities that fall within the law's definition of a “foreign financial institution.” Often, these entities have a close nexus with the treasury function, but the treasury team may not think of them as financial institutions. Common examples include:

Deposit-taking institutions. Some multinational corporations have established deposit-taking institutions in order to enjoy low-cost funding provided by third-party depository accounts outside the United States, where regulations are favorable. Others have set up substantial customer deposit programs to secure contract performance. In addition, many multinationals establish special-purpose securitization vehicles as an efficient way to float debt. Each of these types of entities may qualify as an FFI under FATCA, in which case it will need to comply with the new regime.

Stealth FFIs. Under FATCA, the term “foreign financial institution” can include entities that may not be viewed as affiliates of the multinational corporate for non-tax purposes. These “stealth FFIs” may include:

- offshore leasing or financing companies or factoring entities,

- captive insurance companies,

- foreign retirement plans that do not meet the limited exclusions in the FATCA regulations (or in the intergovernmental agreements, as applicable), or

- non-U.S. foundations and other non-U.S. charitable organizations that are not tax-exempt under Section 501(c) of the Internal Revenue Code.

Treasury centers and holding companies. In certain circumstances, holding companies and treasury centers are defined as FFIs under FATCA. There are exceptions that allow certain treasury centers and holding companies to be excluded from the definition of an FFI. These exclusions, however, may not cover all offshore investment treasury centers that invest offshore cash and engage in other similar arrangements.

FATCA was intentionally drafted with a broad definition of “foreign financial institutions” so that the label fits some entities that are not typically considered financial institutions, such as companies engaged in third-party industrial leasing and financing, or in the factoring of receivables. While the law does make exceptions for investment vehicles that are thought of as posing a low risk of tax evasion, such as retirement plans and tax-exempt entities, criteria for these exceptions have been circumscribed to ensure they are limited to low-risk vehicles.

Multinational corporations have only a few months to identify all the prospective FFIs within their organization because they need to undertake some key activities in mid to late 2013 to avoid the substantial tax consequences of noncompliance. For one thing, every legal entity that meets the definition of a “foreign financial institution” must register through an IRS website that will open later this month. Most companies with affiliated groups that contain FFIs will want to register with the IRS before October 25, 2013, to ensure timely receipt of FATCA-related information by counterparties and other business partners.

FATCA's Effects on Global Cash Management

Even if a multinational company contains no entities that qualify as FFIs, FATCA may have a substantial impact on the organization's treasury function, potentially affecting its relationships with counterparties, banks, and external stakeholders. In general, certain payments made by a treasury center in the U.S. may be treated as U.S.-source income. If they are, FATCA reporting may apply, and withholding may apply if recipients of the payments fail to provide proper FATCA documentation.

Where a corporate treasury department uses third-party foreign banks to assist with cash management, treasurers ought to work closely with their tax teams to examine their legal relationships and assess whether each relationship creates FATCA-relevant responsibilities. If it does, the business must determine whether the FFI/advisor will be FATCA compliant. This is relevant for two reasons: First, to determine whether the multinational corporation or its subsidiaries might be required to withhold under FATCA, and second, to ensure that the multinational's investment with the foreign bank or advisor will not be subject to the 30 percent withholding tax as a result of the service provider's noncompliance.

Common transactions that may be impacted by FATCA include cash sweep arrangements (physical, zero-balance, and notional) and treasury investments held by a foreign custodian. In some cases, the treasury department's derivatives, swaps, and other hedging arrangements might also be affected. These types of transactions frequently involve counterparties outside the U.S., whether directly or through assignment through a multibranch or multiparty International Swaps and Derivatives Association (ISDA) agreement.

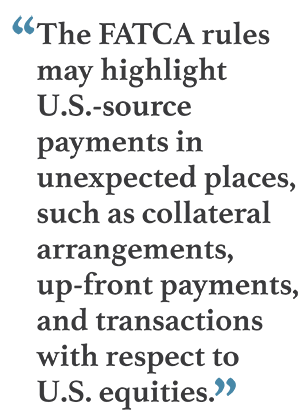

Prior to FATCA, most ISDA agreements required the exchange of tax documentation and provided certain indemnifications if withholding were imposed. Because FATCA changes the scope of the payments that may be subject to withholding, these provisions are more important now. If a multinational corporation or its subsidiary makes U.S.-source payments to an FFI that is not in compliance with FATCA, it will need to withhold tax at the rate of 30 percent. Although the FATCA rules do not change the normal U.S. tax rules for determining whether derivatives and foreign currency transactions are sourced within or outside the U.S., they may highlight U.S.-source payments in unexpected places, such as collateral arrangements, up-front payments, and transactions with respect to U.S. equities.

Some nonfinancial payments are excluded from the scope of FATCA, but these types of transactions are unlikely to be undertaken by the typical treasury function. There are also some grandfathering rules that might limit the impact of FATCA; however, these rules are of limited applicability. Many FFIs are already beginning to request changes to their ISDA agreements to address FATCA. Accordingly, companies need to enhance their focus on proper tax documentation and relevant tax representation in order to manage the risk of FATCA noncompliance.

FATCA's requirements are similar to existing information reporting and withholding requirements, but the documentation that multinational corporations will begin receiving from payees (e.g., Forms W-8 and Forms W-9) under the new law will be enhanced to satisfy its requirements. For example, they will include new tax certifications and payee statuses. In addition, the withholding regime will become more complex as the current withholding regime is transitioned to meet these new requirements.

Next Steps

For most multinational corporations, complying with FATCA involves not only identifying and registering their FFIs, but also scrutinizing cash management and banking relationships to ensure that all their banking partners are FATCA-compliant. Multinationals may also be required to provide additional documentation to FFIs with which they have existing cash management, banking, and credit relationships.

Although this article focuses on the impact of the rules promulgated by the IRS in the United States, companies also need to assess the impact of FATCA through the United States' intergovernmental agreements with foreign governments. Financial relationships maintained by a multinational's non-U.S. subsidiaries or non-U.S. branches located in countries where compliance with FATCA conflicts with local law may lead to significant challenges. The expanding network of intergovernmental agreements may help mitigate these challenges, but in some jurisdictions, getting required information or documentation may remain impossible.

As an initial step, multinationals need to assess the status of all their legal entities and determine the impact of FATCA on payments both made and received by their affiliated group. Treasury departments need to coordinate with affected stakeholders, including the legal and tax departments, to ensure that all relevant information is appropriately gathered or provided. Reporting functions will need to be enhanced to capture and report the additional data required by FATCA, and treasury departments that process tax documentation, determine withholding, or ensure proper reporting will have to adapt to these changes.

Because they are already inspecting their global financial structure to determine the application of FATCA, a number of multinationals are taking the opportunity to review the information reporting and withholding processes performed by their treasury departments. Withholding agents that currently make U.S.-source FDAP payments to non-U.S. persons are generally required to report the payments to the IRS and withhold 30 percent. Compliance reviews related to U.S.-source FDAP payments made to non-U.S. persons are occurring because these issues are required to be reviewed during an IRS examination. Consequently, preparation for FATCA presents a good opportunity to verify that the organization is in compliance with current requirements.

Given the impact of these changes, and the fact that FATCA withholding will begin for certain payees on January 1, 2014, it is time now for multinational corporations to begin revising their reporting and withholding policies and procedures, developing new processes for validating payee certifications, and developing training for personnel involved in the reporting and withholding process. Corporate treasurers need to closely coordinate these activities with their colleagues in the tax and legal department to ensure that all relationships and entities are appropriately documented. The cost of failure to comply includes not only a 30 percent withholding tax, but penalties, interest and reputational risk as well.

—————————————-

Rebecca E. Lee is a principal with PwC US (PricewaterhouseCoopers LLP) who specializes in the taxation of complex financial transactions, including treasury activities. Rebecca can be contacted at [email protected].

Rebecca E. Lee is a principal with PwC US (PricewaterhouseCoopers LLP) who specializes in the taxation of complex financial transactions, including treasury activities. Rebecca can be contacted at [email protected].

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.