The foreign exchange (FX) market is one of the highest-volumemarkets in the financial world; annualized FX trading equates to anastounding 13 times global GDP. Multinational corporations are,necessarily, major participants in the FX market. In order to hedgetheir currency risk, these companies trade large volumes ofFX-based derivatives. However, the playing field for these tradesis often tilted in favor of their banking partners.

|Multinational corporations usually obtain FX derivatives frombanks through over-the-counter (OTC) trading. The unregulated OTCderivatives market generally offers companies the best selection ofinstruments, but a series of scandals in which banks have beencaught gaming various OTC markets indicates that caution isappropriate.

|In 2011, the Bank of New York Mellon was sued by both the NewYork attorney general and the United States attorney general inManhattan for routinely overcharging customers in the processing ofFX transactions. The AGs claimed that the bank defrauded clients ofmore than $2 billion. In the same year, State Street Bank was suedby several state pension funds and investigated by the SEC forsimilar allegations. A year later, it was determined that many ofthe largest banks were gaming LIBOR (the London Interbank Offered Rate), whichunderpins $350 trillion in derivatives. Some were found guilty andfined, including Barclays ($200 million) and UBS ($1.5billion).

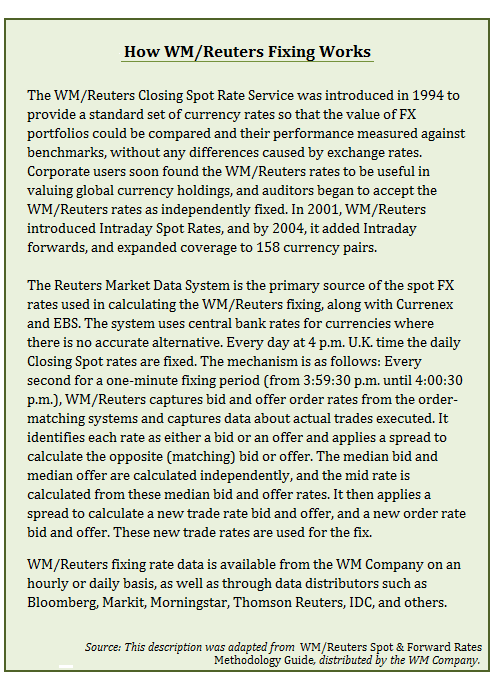

|Then, one year after the LIBOR scandal, a systematic rigging of the WM/Reuters fixing rates was revealed. (See thesidebar How WM/Reuters Fixing Works, below.)Apparently, some major banks were front-running clients' closingspot trade orders, which were large enough to move the market. Abank would sell or buy ahead of the client, then try to move thebenchmark rate in its favor. While one bank alone may not haveenough reserves to substantially change the rate, the four largestbanks—Deutsche, Citigroup, Barclays, and UBS—control more than 50 percent of the market. Traders at these banks would textone another to determine when client orders matched up enough tofacilitate moving the fix. By making a large number of low-volumetrades within the one-minute window during which the WM/Reutersrates are calculated (also known as “banging the close”), the bankscould move the fix and square their positions profitably.

|Price manipulation is not the only way in which banks pose risksfor their foreign exchange clients. Counterparty credit risk isanother concern. When Lehman Brothers moved from investment-gradecredit to bankruptcy over a single weekend in 2008, the company hadmore than 67,000 open trades. While Dodd-Frank, Basel III, andother regulatory changes have reduced this risk by requiring banksto maintain higher Tier 1 capital ratios, multinationalcorporations still risk having their derivatives contracts becomeworthless should a bank default during times of high volatility/lowliquidity.

|Like any corporation, banks are the fiduciary of no one butthemselves. It behooves anyone trading derivatives to do so withcaution and with a defensive attitude. Fortunately, there arespecific actions that a corporate treasurer can take to createtransparency and safety where obfuscation and danger prevail.

|

Guarding Against Price Manipulation

|One of the most effective methods for minimizing costs is to bidout every trade, especially every trade that is a significant size.To guard against price manipulation, multinational corporationsneed to establish trading relationships with multiplecounterparties and ask for bids from each one. For a treasurerwho's shopping around an FX transaction or derivatives trade, it'scrucial to know where the market is. Companies should not depend ontheir banks for quotes of the spot rate or forward points.

| Instead, you need to use independentthird-party sources to determine the spot and forward prices at thetime of each trade. This exposes each bank's true bid-ask spread.Spot rates are easy to verify using services such as TrueFX, but forward points are not aseasy to pinpoint. Subscriptions to Bloomberg, SuperDerivatives,WM/Reuters FX Indices, andInteractiveBrokers are not cheap, but they can pay for themselves byrevealing where the market truly is. Avoiding a misquote of 10basis points (bps) on the forward rate—which consists of the spotrate plus forward points—for a trade worth US$2.5 million per monthwould cover the cost of a typical subscription.

Instead, you need to use independentthird-party sources to determine the spot and forward prices at thetime of each trade. This exposes each bank's true bid-ask spread.Spot rates are easy to verify using services such as TrueFX, but forward points are not aseasy to pinpoint. Subscriptions to Bloomberg, SuperDerivatives,WM/Reuters FX Indices, andInteractiveBrokers are not cheap, but they can pay for themselves byrevealing where the market truly is. Avoiding a misquote of 10basis points (bps) on the forward rate—which consists of the spotrate plus forward points—for a trade worth US$2.5 million per monthwould cover the cost of a typical subscription.

A treasurer may also want to specify that trade pricing will betied to the WM/Reuters fixing rate. Despite the recent scandal,WM/Reuters fixing rates are the most transparent and liquid in theforeign exchange market. Specifying that trades will be priced atthe WM/Reuters spot rate allows a treasurer to bid out the trade'sforward points, preventing any possibility of a skewed spotquote.

|Outsmarting Front-Runners

|Very large corporations must make very large trades to hedgetheir transactional risk, and the size of those trades createsanother kind of pricing risk. Very large trades can actually movethe market, and large companies' banks may be tempted to front-runtheir trades. Banks will usually know the direction a client needsto trade, and this may skew their bid-ask spread for the client'strade.

|A corporation can use several tactics to address this risk. Thefirst tactic is to split the trade among several counterparties.This reduces any one bank's visibility into the size of the overalltrade, which may remove the temptation to front-run it. Tying thetrade's pricing to the WM/Reuters fixing rate and placing the tradejust before the fixing period will prevent banks from communicatingto determine the total size of the trade.

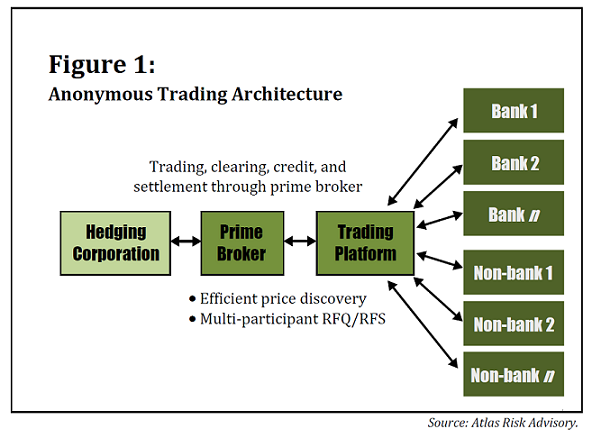

|The second tactic for preventing front-running is to tradeanonymously with multiple liquidity providers. This can be achievedthrough the use of a prime broker and a trading platform, such asFXall or 360T. In this type of transaction, theprime broker places the corporate order anonymously through thetrading platform, which automatically queries the market for thebest pricing. Banks and non-bank FX providers such as Alpha Global Exchange andInfinityInternational can respond to a request for quote (RFQ)/requestfor spread (RFS). (See Figure 1.)

|

Taking Advantage of Exchanges

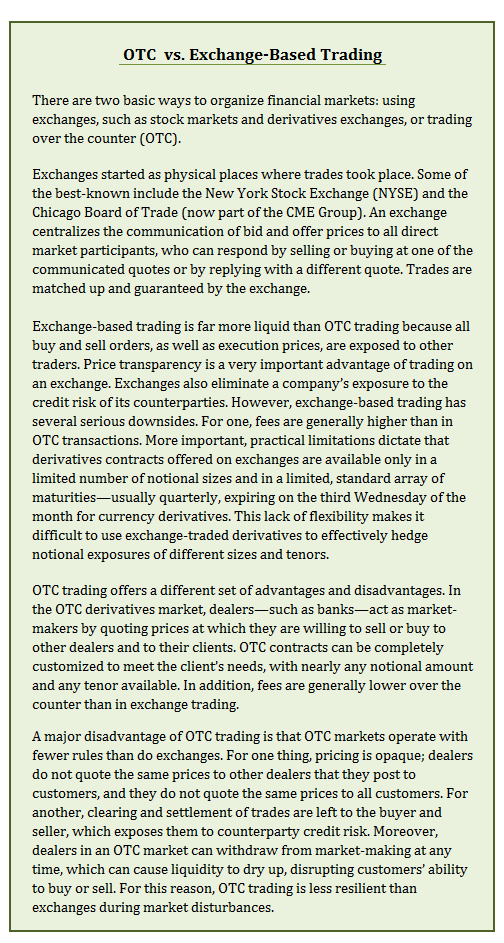

|OTC derivatives usually serve corporate hedging needs betterthan exchanges because they enable the company to set tenors andnotionals with precision. (See OTC vs. Exchange-BasedTrading, below.) However, savvy corporate treasurers use thefutures market in two ways. The first way is through exchange-basedtrading; when a company's desired notionals and tenors match thesize and expiries of available instruments, trading on an exchangeoffers much lower counterparty risk and more pricingtransparency.

The Chicago Mercantile Exchange (CME) recently developed ahybrid facility that offers some of the benefits of exchange-basedtrading while preserving some of the flexibility of the OTC market.Essentially, the CME allows for a variety of OTC trades to besettled and cleared through the exchange. This eliminates bankcounterparty risk because the CME becomes the counterparty.Thirty-eight currency combinations are eligible for trading throughthis service, and maturities can be any valid business day betweenspot and two years. Both the bank and the corporate FX client haveto agree to use the CME service, of course.

|The second way in which exchanges can help corporate treasurersis by creating pricing transparency in the OTC market.Exchange-traded derivatives usually expire on the third Wednesdayof the month. The value of a future and a forward of the sameexpiry must converge, or else there would be an arbitrageopportunity. If a treasurer specifies that his OTC trades shouldexpire on the third Wednesday of the month, the OTC prices thatbanks quote should match the exchange pricing, thus creatingpricing transparency.

|

Controlling Counterparty Risk

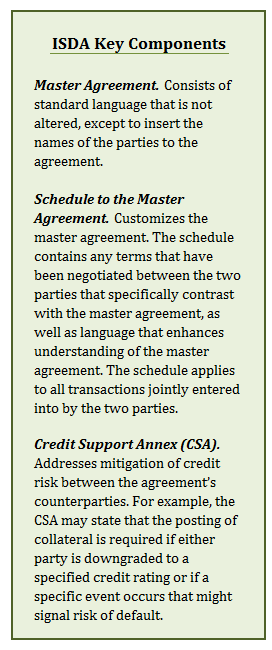

| An International Swaps and DerivativesAssociation (ISDA) MasterAgreement is the cornerstone of any transactional relationshipbetween two parties engaged in OTC financial transactions. (SeeISDA Key Components, at right.) It should come as nosurprise that ISDAs between corporations and banks havetraditionally been rather one-sided. If a company's credit ratingis downgraded beyond a certain level, its banking counterparty willnotify it that it has triggered the terms of its CSA and that itneeds to post additional collateral. But even if a bank actuallydefaults on a corporate customer, the company will likely have noopportunity to collect any collateral.

An International Swaps and DerivativesAssociation (ISDA) MasterAgreement is the cornerstone of any transactional relationshipbetween two parties engaged in OTC financial transactions. (SeeISDA Key Components, at right.) It should come as nosurprise that ISDAs between corporations and banks havetraditionally been rather one-sided. If a company's credit ratingis downgraded beyond a certain level, its banking counterparty willnotify it that it has triggered the terms of its CSA and that itneeds to post additional collateral. But even if a bank actuallydefaults on a corporate customer, the company will likely have noopportunity to collect any collateral.

For example, a typical CSA might call for the exchange ofcollateral if either party's credit rating is BBB or lower. Thecompany may be able to operate for quite some time with a BBBrating, or even at a below-investment-grade level. If the company'scredit rating were to drop to BBB, the bank would have ampleopportunity to obtain collateral under this CSA. However, if amajor bank's credit rating fell to BBB, that would likely be thestraw that broke the camel's back. The bank would no longer havesufficient capital to post collateral, and its cost of funds wouldhave already increased to a level that makes operating as a bankproblematic. The bank would be much more likely to default at thissame credit rating, so a CSA with these terms would provide a falsesense of security to the corporate counterparty.

|What can a corporate treasurer do to level the credit-riskplaying field? First, it's imperative to monitor counterpartyexposures on a timely basis and to set triggers for action. Thesetriggers should be based on real-time indicators of a bank's riskof default, such as its level of credit default swaps (CDS). As thebank approaches the limits you've set, reallocate your short-termtrades and/or cash deposits as much as possible.

|For longer-term exposures, such as cross-currency interest rateswaps or long-dated forwards, consider posting margin utilizing the services of a third-partycollateral manager. Collateral managers accept and remit collateralbased on the mark-to-market status of the outstanding trades toeach financial counterparty. Companies and their banks need tospell out in their CSAs both the role of the collateral manager andthe objective measures of risk that will be used to set collateralrequirements for both parties.

||Limiting Banks' Re-hypothecation Rights

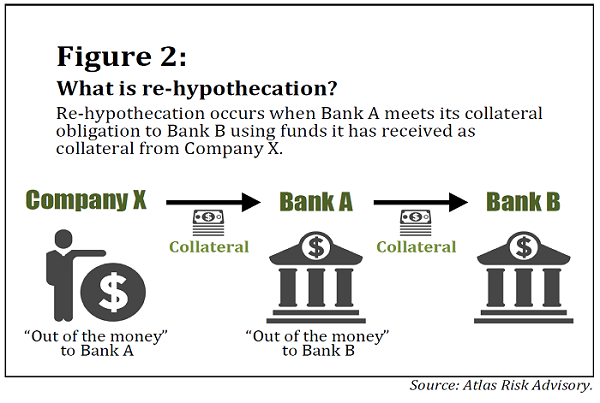

|One other approach to reducing the counterparty risks posed bybanks is to limit their re-hypothecation rights. Figure 2, below, demonstrates howre-hypothecation works. In the illustration, Company X is requiredto post collateral because it is out of the money on a series oftrades with Bank A, its counterparty bank. Bank A, in turn, is outof the money with respect to some transactions it's engaged in withBank B. So at the end of the day, Bank A must post collateral toBank B. Rather than coming up with its own funds to use ascollateral, Bank A prefers to cover its agreement with Bank B by“re-hypothecating” the collateral it receives from Company X.

|For Company X, this arrangement can be highly problematic ifBank A is at risk of default. If the trades happen to move back inCompany X's favor, Bank A may no longer have the funds to returnCompany X's collateral. Rules have been very loose in governing howbanks can re-hypothecate collateral, under the argument that itfrees up capital and makes lending cheaper. Unfortunately, this hasresulted in some circumstances where multiple counterparties haveclaims on the same collateral. In the bankruptcy of MF Global, forexample, untangling the complex trail of commingled assets andcollateral claims took years.

|Whether or not to grant your banking counterpartiesre-hypothecation rights on the collateral you might end up sendingthem is an item for negotiation. If you do not grantre-hypothecation rights, the bank will likely add to the trade afunding charge, which may be significant. One Fortune 100 treasurymanager, with whom we recently discussed this issue, noted that thefunding charge his company faced during negotiations would havebeen prohibitively expensive, so although the company consideredits options, in the end it granted re-hypothecation rights to itscounterparty.

|

Adopting a Defensive Posture

|Because it is largely unregulated, the over-the-counter marketfor FX derivatives is full of hidden and costly traps that threatento catch up unsuspecting corporate treasurers. Tactics companiesmight encounter from their banking counterparties include outrightprice misquotes, skewed bid-ask spreads, front-running of largetrades, asymmetric ISDAs and CSAs, and re-hypothecation.

|Fortunately, multinational corporations have a number of optionsfor leveling the playing field. All treasurers engaging inderivatives trades should obtain accurate and unbiased marketinformation, and should bid out large transactions. Once they knowwhere the market is, treasurers can consider splitting trades amongmultiple counterparties or trading anonymously to preventfront-running. They can time their OTC trades to coincide with CMEmaturity dates and the WM/Reuters fixing schedule. They cannegotiate CSAs that are more fair. They should monitor their banks'credit ratings along with their exposure to the banks, and theyshould consider utilizing third-party collateral managers. Acorporate treasury team that uses these tactics in its FXderivatives trading dramatically reduces its risk of beingovercharged or caught flat-footed by credit issues among itsbanking counterparties.

|—————————————————

| Paul Stafford is thedirector of marketing for Atlas Risk Advisory, a firm that providesFX risk management software and consulting services tomultinational corporations.

Paul Stafford is thedirector of marketing for Atlas Risk Advisory, a firm that providesFX risk management software and consulting services tomultinational corporations.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.