In 2011, cross-border trade reached a value of around US$18.2trillion. Most of this activity—80 to 90 percent—was settled onopen account terms, meaning that the buyer received the shipmentbefore paying the seller. Open account trade has clear benefits forbuyers of goods, but it puts sellers at some risk that the buyermight not pay. This can be especially troublesome when a companyfirst begins selling to a new buyer in an unfamiliar region of theworld. The traditional method for mitigating counterparty risk insuch a situation is the letter of credit (L/C), a paper documentissued by a bank that assures payment once the bank receivesdocumentation that the shipment has fully met the contractterms.

|Now companies have access to a new instrument. The bank paymentobligation (BPO) functions like a traditional letter of creditinstrument that supports a commercial open account trade payment.It transfers buyer risk to an obligor bank in the same way that anL/C does, but it does so much more efficiently because fulfillmentof a BPO involves the digital exchange and matching of data in ISO20022 XML format.

|So far, around 50 banks have signed up to support BPOs, andthose banks cover approximately 75 percent of the trade flows thatpass through the global banking system. That number should continueto climb. In April, the International Chamber of Commerce (ICC)approved the Uniform Rules for Bank Payment Obligations (URBPO),the bank-to-bank rules governing use of the new instrument; therules went into effect at the beginning of July.

|The rules can be incorporated on a bilateral basis into anytransaction flow. But for now, SWIFT's Trade Services Utility (TSU) is the standard data matchingengine used for BPO transactions, largely because having a neutralthird party match the data helps build confidence in theinstrument.

|Although it will take many years for the BPO to become aswell-established and widely used as the L/C, companies arebeginning to test the waters. Early adopters include BP Chemicals,which has been using BPOs for more than a year, and Japanesedepartment store chain Ito-Yokado, which uses BPOs to supportimports from its Chinese suppliers. By mitigating key risks withintrading relationships, BPOs have the capacity to become animportant component in a company's supply chain managementstrategy.

|How Does a BPO Work?

|A BPO is born when the buyer in a transaction asks its bank tocreate an open account payment instrument with a bank paymentobligation. The buyer submits to its bank information about theorder, such as quantity, unit cost, port of departure, port ofarrival, payment terms, and International Commercial terms(Incoterms). The buyer's bank then uploads this information to theSWIFT TSU, which in turn passes the information to the seller'sbank for checking. When the seller's bank accepts the data, the“baseline” for the BPO is established, and the buyer's bankguarantees that it will pay the seller's bank as long as the sellerships the merchandise in accordance with the terms of theagreement.

|Once the seller has shipped the goods, its bank uploads theshipping and logistics data (e.g., bill of lading, airway bill) tothe TSU to be checked against the baseline. As long as the datamatches, the buyer's bank is required to settle the invoice withthe seller's bank on the due date.

|So if Company B orders 100 cartons of blueT-shirts and requests a BPO for the transaction, its bank willupload the transaction's purchase order information to the SWIFTTSU. Then the seller—say, Company S—will have its bank uploadinvoice data, which should describe the manufacture and shipping of100 cartons of blue T-shirts. The TSU will match the purchase orderdata with the invoice data. If the quantity, price, shipping terms,port of departure, etc. all match, then the bank for Company B isobligated to pay the bank for Company S. This is similar to thetransaction-data matching that happens regularly in enterpriseresource planning (ERP) and treasury management systems, but it'sperformed by an independent third party, and the BPO addsassurances of payment from the buyer's bank.

|The Value Proposition

|Bank payment obligations offer substantial benefits for bothsellers and buyers. For the seller, the BPO mitigates non-paymentrisk by substituting bank counterparty risk for buyer counterpartyrisk. Perhaps more importantly, a BPO effectively separates therisk of non-payment from the seller's ability to finance itsreceivables. Once the baseline for the BPO is established and thebuyer's bank is unconditionally obligated to pay, the seller may beable to obtain pre-shipment financing.

From the buyer's point of view, a BPO offers the opportunity tonegotiate better contract terms because the supplier has betteraccess to financing. A buyer that is larger than its suppliers, orthat has a better credit rating, can use BPOs to leverage its lowercost of capital upstream for strategic suppliers. In return, thebuyer may request extended payment terms or a reduction in the costof goods. BPOs can also be helpful when a particular buyer exceedsthe internal credit limit that it has been granted by the seller.The seller can use a BPO to diversify its exposure away from thatbuyer in favor of the buyer's bank.

|For both parties, the BPO removes many of the time-consumingactivities involved in matching paper invoices and the paymentdelays associated with document discrepancies. Moreover, becausedata from both buyer and seller is available in the standardizedISO 20022 format, the parties can upload it to their treasury orERP systems and mine it for insights into their overall financialsupply chain activities.

||BPOs in Context

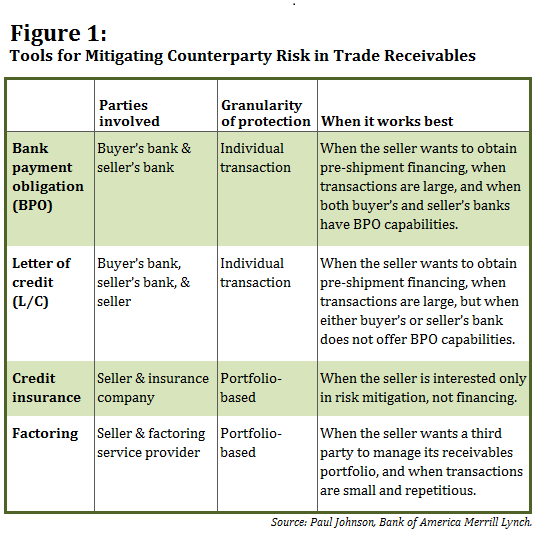

|How does the BPO compare with existing tools and techniques? Interms of their risk mitigation benefits, BPOs are most comparableto letters of credit. In both cases, the buyer's bank guaranteespayment as long as certain conditions are met and documented.However, the BPO is not simply an electronic L/C. For one thing,the BPO is a straightforward bank-to-bank arrangement in which theseller's bank—and not the seller itself—is the beneficiary. Assuch, the two-party BPO is simpler and more insulated from theunderlying transaction than a traditional L/C, in which the issuingbank, the advising bank, and the beneficiary are allparties.

In addition, because the trigger to payment with a BPO is thepresentation of XML data, rather than the exchange of paper-baseddocumentation such as invoices and bills of lading, there is farless friction in the process. This means that although the BPOprovides many of the same features as an L/C, it costs less andbehaves quite differently. Cycle times are much faster and muchmore predictable, so a buyer can issue a BPO much closer to theshipment date—say, two days before shipment instead of 30 to 60days out. The seller still gets the risk protection it wants beforeshipping the order, but the buyer doesn't have to tie up its linesof credit for months to account for the inefficiencies of the100-year-old L/C process. Ultimately, a BPO enables both parties tomanage working capital much more precisely than does a letter ofcredit.

|Although the BPO may be used as an L/C substitute, it wasdesigned to be an alternative to other open account risk mitigationand financing tools, such as credit insurance and factoring. Onekey difference from either of these options is that a BPO istransactional, meaning it can be used on a shipment-by-shipmentbasis, while credit insurance and factoring are portfolio-based andtypically do not offer sellers the ability to select particulartransactions for protection.

|Another important differentiator between BPOs and creditinsurance is that the latter does not help with liquidity or supplychain financing. Credit insurance may be a good solution for purerisk mitigation, but even then, it is a secondary source ofrepayment for the company selling the goods. The seller first hasto seek payment from the buyer and then, if the buyer doesn't pay,the seller has to go through the claims process, which can becumbersome and time-consuming.

|Factoring, or selling an accounts receivable portfolio, ispopular with exporters, and it can make sense when a company has aportfolio of transactions that are small and repetitious. However,factoring businesses often want to take over servicing the seller'saccounts receivable ledger, which an exporter may find intrusive,while BPO servicing is done by the exporter. Companies with morebig-ticket, episodic receivables may find BPOs to be a morecost-effective and efficient solution than factoring.

|

Building a Business Case for 21st-Century TradeSettlement

|It takes two to tango in any kind of trade transaction, andlocal banks in emerging markets may have never heard of a bankpayment obligation. Nevertheless, for companies that engage inlarge transactions in far-flung regions of the world, now is a goodtime to look into this option.

| Before an organization can encouragetrading partners to adopt BPOs, however, it needs to build internalconsensus around the idea. This is not an insignificant challenge.People in the company's procurement, treasury, finance, andlogistics departments will all have different perspectives on whatis important when it comes to trade instruments. For example,procurement and logistics usually focus on getting the right goodsto the right place at the right time, whereas treasury's prioritymay be to avoid the ballooning of the balance sheet by offeringbuyers generous terms to close deals. To overcome varying andsometimes contradictory priorities, everyone in the organizationhas to recognize BPOs' benefits for their particular function.

Before an organization can encouragetrading partners to adopt BPOs, however, it needs to build internalconsensus around the idea. This is not an insignificant challenge.People in the company's procurement, treasury, finance, andlogistics departments will all have different perspectives on whatis important when it comes to trade instruments. For example,procurement and logistics usually focus on getting the right goodsto the right place at the right time, whereas treasury's prioritymay be to avoid the ballooning of the balance sheet by offeringbuyers generous terms to close deals. To overcome varying andsometimes contradictory priorities, everyone in the organizationhas to recognize BPOs' benefits for their particular function.

At the same time, companies looking to use BPOs may facetactical hurdles in areas such as obtaining IT support in creatingand deploying the XML message schemas for exchanging data withbanks. Many companies overcome this type of challenge by engaging aC-level executive in the process, someone who is capable of makingsupply chain decisions (both operational and financial) through anenterprise lens, rather than at the line-of-business or functionallevel. Quite often, this executive reports to the CEO, reflectingthe fact that supply chain optimization is seen as a major sourceof competitive advantage.

|Finally, companies wanting to move forward with BPOs need tomake sure that their bank not only has the necessary capabilitiesnow, but also has made a long-term commitment to supporting thisnew instrument. The bank needs to have a global network and deepexpertise in trade finance.

|As companies build a business case for using BPOs, they need toclearly articulate the overall benefits they hope to achieve. Goalsmay relate to risk mitigation, financing, and visibility. Companiescan measure BPOs' success by evaluating changes in their usage oflines of credit—in other words, whether they're using less creditor turning it over faster. They can look at working capital metrics such as days payables outstanding(DPO), days inventory outstanding (DIO), and days sales outstanding(DSO). And they can evaluate the degree to which administrativecosts fall and cycle times accelerate.

|The BPO has much to offer counterparties currently trading onopen account terms. Although the tool is just starting to gainmomentum, early adopters are already reaping the benefits.Incorporating a bank guarantee into existing open account trade maybe well worth the disruption to established business practices.Because it draws on database technologies and global standards,this new instrument has the potential to benefit all parties in atrade transaction—and to bring trade settlement into the 21stcentury.

|—————————————-

| Paul Johnson is thesenior product manager, global trade and supply chain, withBank of America Merrill Lynch. His primaryresponsibilities include development and rollout of new trade andsupply chain programs, product management and globalsales/marketing support, structuring unique trade transactions,training, and working with risk management and compliance.

Paul Johnson is thesenior product manager, global trade and supply chain, withBank of America Merrill Lynch. His primaryresponsibilities include development and rollout of new trade andsupply chain programs, product management and globalsales/marketing support, structuring unique trade transactions,training, and working with risk management and compliance.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.