In 2011, cross-border trade reached a value of around US$18.2 trillion. Most of this activity—80 to 90 percent—was settled on open account terms, meaning that the buyer received the shipment before paying the seller. Open account trade has clear benefits for buyers of goods, but it puts sellers at some risk that the buyer might not pay. This can be especially troublesome when a company first begins selling to a new buyer in an unfamiliar region of the world. The traditional method for mitigating counterparty risk in such a situation is the letter of credit (L/C), a paper document issued by a bank that assures payment once the bank receives documentation that the shipment has fully met the contract terms.

Now companies have access to a new instrument. The bank payment obligation (BPO) functions like a traditional letter of credit instrument that supports a commercial open account trade payment. It transfers buyer risk to an obligor bank in the same way that an L/C does, but it does so much more efficiently because fulfillment of a BPO involves the digital exchange and matching of data in ISO 20022 XML format.

So far, around 50 banks have signed up to support BPOs, and those banks cover approximately 75 percent of the trade flows that pass through the global banking system. That number should continue to climb. In April, the International Chamber of Commerce (ICC) approved the Uniform Rules for Bank Payment Obligations (URBPO), the bank-to-bank rules governing use of the new instrument; the rules went into effect at the beginning of July.

The rules can be incorporated on a bilateral basis into any transaction flow. But for now, SWIFT's Trade Services Utility (TSU) is the standard data matching engine used for BPO transactions, largely because having a neutral third party match the data helps build confidence in the instrument.

Although it will take many years for the BPO to become as well-established and widely used as the L/C, companies are beginning to test the waters. Early adopters include BP Chemicals, which has been using BPOs for more than a year, and Japanese department store chain Ito-Yokado, which uses BPOs to support imports from its Chinese suppliers. By mitigating key risks within trading relationships, BPOs have the capacity to become an important component in a company's supply chain management strategy.

How Does a BPO Work?

A BPO is born when the buyer in a transaction asks its bank to create an open account payment instrument with a bank payment obligation. The buyer submits to its bank information about the order, such as quantity, unit cost, port of departure, port of arrival, payment terms, and International Commercial terms (Incoterms). The buyer's bank then uploads this information to the SWIFT TSU, which in turn passes the information to the seller's bank for checking. When the seller's bank accepts the data, the “baseline” for the BPO is established, and the buyer's bank guarantees that it will pay the seller's bank as long as the seller ships the merchandise in accordance with the terms of the agreement.

Once the seller has shipped the goods, its bank uploads the shipping and logistics data (e.g., bill of lading, airway bill) to the TSU to be checked against the baseline. As long as the data matches, the buyer's bank is required to settle the invoice with the seller's bank on the due date.

So if Company B orders 100 cartons of blue T-shirts and requests a BPO for the transaction, its bank will upload the transaction's purchase order information to the SWIFT TSU. Then the seller—say, Company S—will have its bank upload invoice data, which should describe the manufacture and shipping of 100 cartons of blue T-shirts. The TSU will match the purchase order data with the invoice data. If the quantity, price, shipping terms, port of departure, etc. all match, then the bank for Company B is obligated to pay the bank for Company S. This is similar to the transaction-data matching that happens regularly in enterprise resource planning (ERP) and treasury management systems, but it's performed by an independent third party, and the BPO adds assurances of payment from the buyer's bank.

The Value Proposition

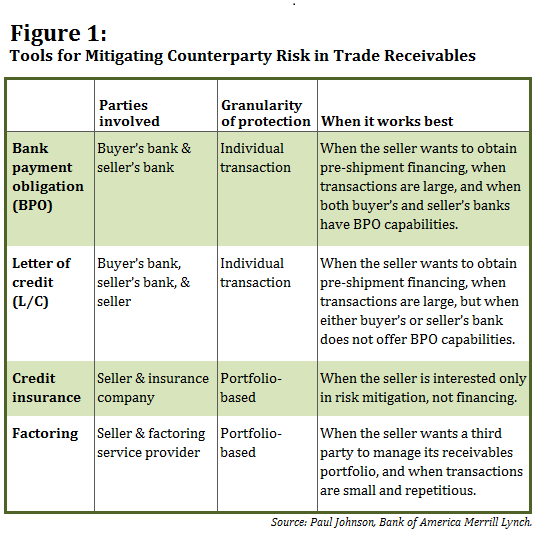

Bank payment obligations offer substantial benefits for both sellers and buyers. For the seller, the BPO mitigates non-payment risk by substituting bank counterparty risk for buyer counterparty risk. Perhaps more importantly, a BPO effectively separates the risk of non-payment from the seller's ability to finance its receivables. Once the baseline for the BPO is established and the buyer's bank is unconditionally obligated to pay, the seller may be able to obtain pre-shipment financing.

From the buyer's point of view, a BPO offers the opportunity to negotiate better contract terms because the supplier has better access to financing. A buyer that is larger than its suppliers, or that has a better credit rating, can use BPOs to leverage its lower cost of capital upstream for strategic suppliers. In return, the buyer may request extended payment terms or a reduction in the cost of goods. BPOs can also be helpful when a particular buyer exceeds the internal credit limit that it has been granted by the seller. The seller can use a BPO to diversify its exposure away from that buyer in favor of the buyer's bank.

For both parties, the BPO removes many of the time-consuming activities involved in matching paper invoices and the payment delays associated with document discrepancies. Moreover, because data from both buyer and seller is available in the standardized ISO 20022 format, the parties can upload it to their treasury or ERP systems and mine it for insights into their overall financial supply chain activities.

BPOs in Context

How does the BPO compare with existing tools and techniques? In terms of their risk mitigation benefits, BPOs are most comparable to letters of credit. In both cases, the buyer's bank guarantees payment as long as certain conditions are met and documented. However, the BPO is not simply an electronic L/C. For one thing, the BPO is a straightforward bank-to-bank arrangement in which the seller's bank—and not the seller itself—is the beneficiary. As such, the two-party BPO is simpler and more insulated from the underlying transaction than a traditional L/C, in which the issuing bank, the advising bank, and the beneficiary are all parties.

In addition, because the trigger to payment with a BPO is the presentation of XML data, rather than the exchange of paper-based documentation such as invoices and bills of lading, there is far less friction in the process. This means that although the BPO provides many of the same features as an L/C, it costs less and behaves quite differently. Cycle times are much faster and much more predictable, so a buyer can issue a BPO much closer to the shipment date—say, two days before shipment instead of 30 to 60 days out. The seller still gets the risk protection it wants before shipping the order, but the buyer doesn't have to tie up its lines of credit for months to account for the inefficiencies of the 100-year-old L/C process. Ultimately, a BPO enables both parties to manage working capital much more precisely than does a letter of credit.

Although the BPO may be used as an L/C substitute, it was designed to be an alternative to other open account risk mitigation and financing tools, such as credit insurance and factoring. One key difference from either of these options is that a BPO is transactional, meaning it can be used on a shipment-by-shipment basis, while credit insurance and factoring are portfolio-based and typically do not offer sellers the ability to select particular transactions for protection.

Another important differentiator between BPOs and credit insurance is that the latter does not help with liquidity or supply chain financing. Credit insurance may be a good solution for pure risk mitigation, but even then, it is a secondary source of repayment for the company selling the goods. The seller first has to seek payment from the buyer and then, if the buyer doesn't pay, the seller has to go through the claims process, which can be cumbersome and time-consuming.

Factoring, or selling an accounts receivable portfolio, is popular with exporters, and it can make sense when a company has a portfolio of transactions that are small and repetitious. However, factoring businesses often want to take over servicing the seller's accounts receivable ledger, which an exporter may find intrusive, while BPO servicing is done by the exporter. Companies with more big-ticket, episodic receivables may find BPOs to be a more cost-effective and efficient solution than factoring.

Building a Business Case for 21st-Century Trade Settlement

It takes two to tango in any kind of trade transaction, and local banks in emerging markets may have never heard of a bank payment obligation. Nevertheless, for companies that engage in large transactions in far-flung regions of the world, now is a good time to look into this option.

Before an organization can encourage trading partners to adopt BPOs, however, it needs to build internal consensus around the idea. This is not an insignificant challenge. People in the company's procurement, treasury, finance, and logistics departments will all have different perspectives on what is important when it comes to trade instruments. For example, procurement and logistics usually focus on getting the right goods to the right place at the right time, whereas treasury's priority may be to avoid the ballooning of the balance sheet by offering buyers generous terms to close deals. To overcome varying and sometimes contradictory priorities, everyone in the organization has to recognize BPOs' benefits for their particular function.

Before an organization can encourage trading partners to adopt BPOs, however, it needs to build internal consensus around the idea. This is not an insignificant challenge. People in the company's procurement, treasury, finance, and logistics departments will all have different perspectives on what is important when it comes to trade instruments. For example, procurement and logistics usually focus on getting the right goods to the right place at the right time, whereas treasury's priority may be to avoid the ballooning of the balance sheet by offering buyers generous terms to close deals. To overcome varying and sometimes contradictory priorities, everyone in the organization has to recognize BPOs' benefits for their particular function.

At the same time, companies looking to use BPOs may face tactical hurdles in areas such as obtaining IT support in creating and deploying the XML message schemas for exchanging data with banks. Many companies overcome this type of challenge by engaging a C-level executive in the process, someone who is capable of making supply chain decisions (both operational and financial) through an enterprise lens, rather than at the line-of-business or functional level. Quite often, this executive reports to the CEO, reflecting the fact that supply chain optimization is seen as a major source of competitive advantage.

Finally, companies wanting to move forward with BPOs need to make sure that their bank not only has the necessary capabilities now, but also has made a long-term commitment to supporting this new instrument. The bank needs to have a global network and deep expertise in trade finance.

As companies build a business case for using BPOs, they need to clearly articulate the overall benefits they hope to achieve. Goals may relate to risk mitigation, financing, and visibility. Companies can measure BPOs' success by evaluating changes in their usage of lines of credit—in other words, whether they're using less credit or turning it over faster. They can look at working capital metrics such as days payables outstanding (DPO), days inventory outstanding (DIO), and days sales outstanding (DSO). And they can evaluate the degree to which administrative costs fall and cycle times accelerate.

The BPO has much to offer counterparties currently trading on open account terms. Although the tool is just starting to gain momentum, early adopters are already reaping the benefits. Incorporating a bank guarantee into existing open account trade may be well worth the disruption to established business practices. Because it draws on database technologies and global standards, this new instrument has the potential to benefit all parties in a trade transaction—and to bring trade settlement into the 21st century.

—————————————-

Paul Johnson is the senior product manager, global trade and supply chain, with Bank of America Merrill Lynch. His primary responsibilities include development and rollout of new trade and supply chain programs, product management and global sales/marketing support, structuring unique trade transactions, training, and working with risk management and compliance.

Paul Johnson is the senior product manager, global trade and supply chain, with Bank of America Merrill Lynch. His primary responsibilities include development and rollout of new trade and supply chain programs, product management and global sales/marketing support, structuring unique trade transactions, training, and working with risk management and compliance.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.