Last month, Chatham Financial released a benchmarkingreport on the state of financial risk management amongU.S.-based businesses. Chatham studied the Securities and ExchangeCommission (SEC) filings of more than 1,000 public companies withannual revenues between $500 million and $20 billion, excludingfinancial services and insurance companies, to determine how manyof these organizations incur currency, commodity, and interest raterisks, and how they mitigate those risks.

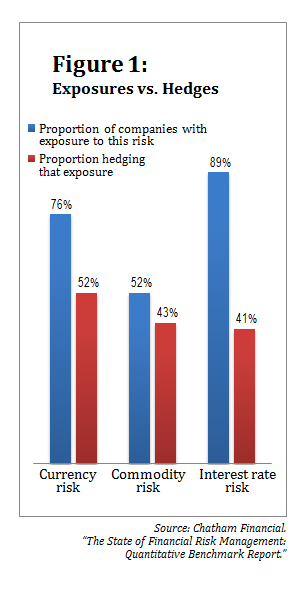

Many of these organizations have experienced a significantincrease in financial risks over the past decade, as they'veextended their operations abroad and as volatility has increased inglobal financial markets. Nevertheless, Chatham found that manycompanies with foreign exchange, interest rate, and/or commodityrisks on their financial statements are not using derivatives tohedge these risks (see Figure 1).

|About half of organizations that have currency risk are hedgingtheir exposure; the Chatham report notes that this is “asurprisingly low percentage given the extreme volatility around thecurrencies to which the companies have exposure.” The majority ofcompanies that are hedging foreign exchange (FX) risk are using both balance sheetand cash flow hedges.

|Among the companies that Chatham found to have commodity risk,even fewer are using derivatives to hedge it. Commodity hedging ismuch more prevalent in industries where commodity risk is core tothe business model—including natural resources and mining,transportation and utilities, and manufacturing. Larger companiesare also much more likely to hedge commodity risks. From thecombination of these factors, Chatham concludes: “Given thecomplexity of hedging commodities in the financial markets, itappears as though only sufficiently sophisticated corporations withcommodities as a core exposure have a tendency to hedge in thismanner.”

|Finally, interest rate risk—from credit agreements, asset-backedloans, bonds, etc.—is a concern for 89 percent of the companieswhose financial statements Chatham studied. However, only 41percent of those businesses hedge their interest rate risk usingderivatives. This is partly explained by companies' ability tomitigate some of the risk by issuing a combination of debt withfixed interest rates and debt with floating rates.

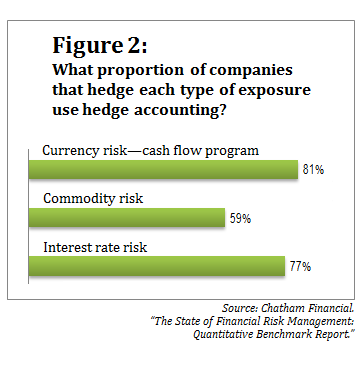

|Most companies that hedge risks in each financial-risk categoryuse hedge accounting under ASC 815 (formerly FAS 133), but hedgeaccounting is by no means universal. Figure 2 shows the breakdown,including for currency risk only cash flow hedging programs, asbalance sheet programs generally don't require the use of hedgeaccounting.

|

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.