To gain a better understanding of the complexities andinefficiencies inherent in modern “treasury onboarding,” TreasuryStrategies recently undertook a survey, commissioned by WAUSAUFinancial Systems, a vendor of solutions for payments andreceivables processing. The survey gauged the opinions of bothbanks and corporate users of banking services about the processthrough which banks sell and then implement new services forcorporate clients. Corporate treasurers may not be surprised tolearn that the businesses outside the financial services sector seemore problems with the process than do their banks.

|Treasury Strategies asked the corporate respondents howfrequently they face issues such as a lack of visibility into theimplementation process, unnecessarily long or inefficientimplementations, and poor communication with the bank. “All ofthose problems were rated above a 3 out of 5, with 5 meaning 'veryoften,'” says Chris Zegal, vice president of marketing at WAUSAU.“An issue rated 3 probably occurs fairly often.” The averagefrequency rating that large companies assigned to the problem oflacking a clear view into the implementation's status was 3.8, andthese organizations experience communication problems at afrequency of 3.5 (see Figure 1). “Since all of these are ratedabove a 3, the companies probably have some sort of challenge inevery implementation. It seems like problems are the norm ratherthan the exception,” Zegal adds.

|Survey respondents who work for banks gave these issuesconsiderably lower frequency ratings than did the corporaterespondents. For example, large banks scored “customer isdissatisfied with communication” at 2.5, compared with the 3.5 thatcompanies gave “poor communication with bank.” As Zegal interpretsthis result: “The banks know they have these challenges, but theydon't think they happen as frequently as the corporations thinkthey do.”

|

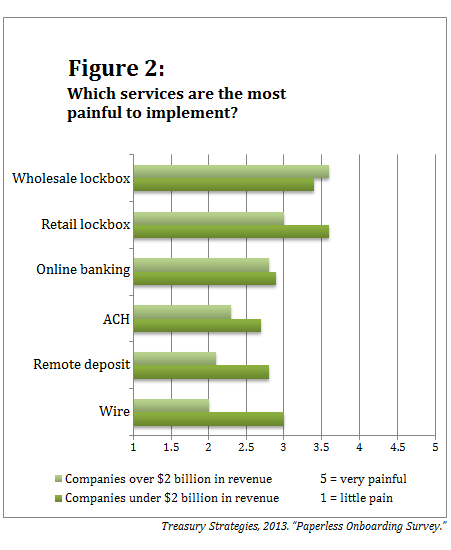

The survey also asked companies which banking services are mostpainful to implement. Lockbox services ranked first, but manyrespondents indicated that their organization has also struggled toget up to speed with online banking, Automated Clearing House (ACH)transactions, remote deposit, and wire transfers (see Figure 2).All except wholesale lockbox services are less painful for largercompanies than for smaller businesses—presumably because largerorganizations have more resources to devote to implementation.

|“Companies want to go live with these services quickly andeasily,” says Joe Pitzo, vice president, paperless enterprisesolutions, for WAUSAU. “It should be painless. And what we see inthis survey is that that isn't always the case.”

|

“The expectations of companies today are much like those ofconsumers,” Pitzo adds. “They want to be kept up to date throughoutthe entire process, from sales through delivery and training on newservices. They get that type of notification on UPS and FedExdeliveries. Even with food deliveries you're kept up to date. Andtreasurers expect a similar response from their financialinstitutions when they're signing up for services.”

|Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.