Last week, The Hackett Group released a report aptlytitled “Transformingthe Finance Organization: Ambition vs. Reality.” It combinesthe results of two Hackett research projects and reaches theconclusion that finance teams have been biting off more than theycan chew when it comes to transformational projects. However,Hackett also finds that finance executives' change agenda in 2013was considerably more modest than it was a couple yearsprior—suggesting that ambition in the finance function may bestarting to align more closely with reality.

Last week, The Hackett Group released a report aptlytitled “Transformingthe Finance Organization: Ambition vs. Reality.” It combinesthe results of two Hackett research projects and reaches theconclusion that finance teams have been biting off more than theycan chew when it comes to transformational projects. However,Hackett also finds that finance executives' change agenda in 2013was considerably more modest than it was a couple yearsprior—suggesting that ambition in the finance function may bestarting to align more closely with reality.

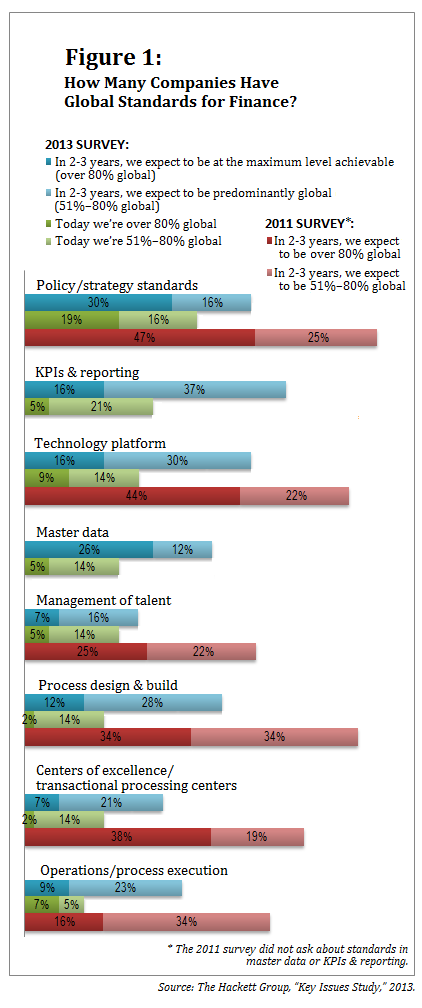

In its 2013 “Key Issues Study,” Hackett asked finance executivesin a wide range of companies whether their organization has globalstandards in eight areas: technology infrastructure, keyperformance indicators (KPIs) and reporting, talent management,master data, centers of excellence/transaction processing centers,setting policies and strategies, designing and building processes,and operations/process execution. See Figure 1, below.

|In each of these areas, respondents were asked to pick thecategory of global standardization that best describes theirorganization's current state and the category that they expect toreach in the next two to three years. Many respondents selected onecategory to describe their company's current state (e.g.,“predominantly global—51% to 80%”) and picked the next category upto describe where they expect to be in a few years (e.g., “maximumglobal level achievable—more than 80%”). The category with the mostrespondents reporting that their organization already has globalstandards was “policy/strategy standards”—19 percent said they'reat the maximum level achievable, and 16 percent said they'repredominantly global. These numbers are strong, yet 30 percent ofrespondents expect to reach the maximum level within three years,while 16 percent expect to be predominantly global at that time. Ifthese projects are successful, the proportion of companies at themaximum achievable level of globalization in policy/strategystandards would increase by more than 50 percent in just a fewyears.

|The question is: How likely are they to be successful? “Thereality is that over the past two years, the data from our annual'Key Issues Study' show no measurable increase in the level ofglobal standards across business services,” last week's Hackettreport states. Lynne Schneider, senior research director withHackett and one of the report's authors, puts it this way: “Acrossthe board, people are optimistic about how much change they canexecute in the next two to three years, relative to what they didin the past two to three years. I think the difference may beambition versus reality.”

|Comparing the data from Hackett's latest “Key Issues Study” withthe 2011 version of the same survey brings the challenge into starkfocus. Look at how respondents' 2011 projections of where theyexpect to be in two to three years (the red lines on Figure 1)compare with the 2013 reality (the green lines). For example,organizations may be more advanced in global policy/strategystandards than in other areas, but three years ago 47 percent ofcompanies expected to be at the maximum achievable level of globalstandardization by now, and only 19 percent have actually reachedthat goal.

|Perhaps because so many companies failed to achieve their goalsfrom a few years ago, comparing finance's 2011 expectations (thered lines) with the expectations for two to three years from now(the blue lines) reveals a serious reduction in ambition. A quarterof 2011 respondents expected their talent management to be at themaximum possible level of globalization by now. Yet only 5 percentof companies actually reached that goal—and only 7 percent nowthink they'll be there by 2016.

|“I think that finance people have realized that getting to thislevel of global standard is more difficult than they initiallythought,” Schneider says. “The benefit of hindsight is that theycan see that they set goals that were unreachable with theresources that they had, and now they are trying to do a better jobof setting goals for standardization that are more readilyachievable. The difference between where they are today and wherethey want to be in a few years is still significant, but they areprobably being more realistic about the amount of improvement theywill be able to make.”

|

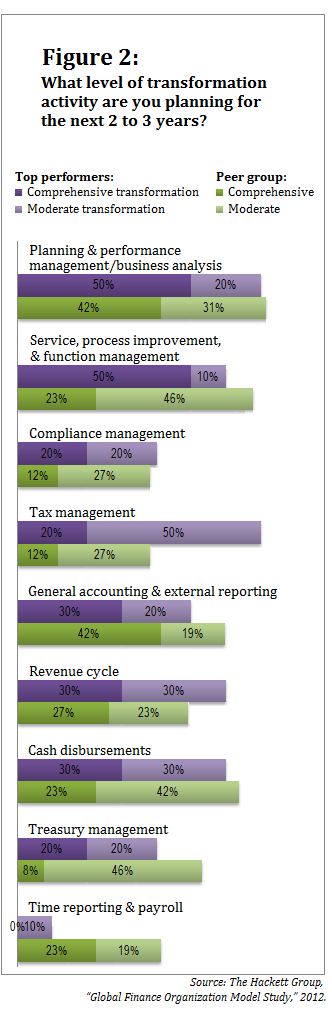

The report released last week also considersresults of a separate Hackett study, conducted in 2012, thatexplored which finance processes companies have been working totransform, and which they expect to tackle in the near future. Inthat survey, Hackett divided respondents into two performancecategories based on the cost of their finance function, its degreeof standardization, and indicators of the quality of its outputs.Top performers accounted for around 20 to 25 percent of theparticipants, and Hackett grouped the rest of the organizationsinto a “peer group.”

|Half of all top performers reported that they hadcomprehensively transformed their compliance management practicesfrom 2010 to 2012, while 40 percent had engaged in comprehensivetransformation of their planning and performance managementprocesses, and the same proportion had transformed “service,process improvement, and function management.” In contrast, only 19percent of the peer group had completed comprehensivetransformations of compliance management or of service, processimprovement, and function management—and only 12 percent hadtransformed planning and performance management.

|The areas in which the most peer-group companies had achievedcomprehensive transformation were cash disbursements (27 percent)and tax management (23 percent). More than half (58 percent) of thepeer group had achieved either moderate or comprehensivetransformation of their general accounting and external reportingprocesses.

Looking forward, companies in both performance categories saidthey expect to do a better job of transforming their financeprocesses over the next two to three years. Half of all topperformers, and 42 percent of the peer group, plan to complete acomprehensive transformation of planning and performancemanagement/business analysis. (See Figure 2.) Those proportions aremuch higher than the 40 percent of top performers and 12 percent ofthe peer group that had achieved comprehensive transformation inthat area in the recent past.

|Although history suggests that companies tend to be overlyoptimistic about their ability to transform critical processes andachieve global standardization, many now seem to be making internalchanges that improve their chances of succeeding with theirtransformational goals over the next few years. Schneider saysshe's seeing an increasing number of companies dedicating resourcesto transformational projects. “We have seen a renewed focus oninternal transformation groups. It's our hope that these groupsdon't get their attention subdivided into 15 differenthigh-priority projects that all must be done right now,” shesays.

|“More and more companies are making investments to put in placethe right infrastructure to carry out these projects,” adds TomWillman, an associate principal and global practice leader, financeexecutive advisory program, for Hackett and Schneider's co-authoron the report. “Are companies going to be more successful than theyhave been in the past? I think the key is: Are they going toadequately prioritize the things they want to accomplish anddedicate the appropriate resources to those activities? If yes,then they are positioned to make some meaningful progress. You haveto prioritize what is most important from a strategic standpointand what is most important from a financial standpoint, thenallocate resources and set expectations appropriately against thosepriorities.”

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.