|

Global pension plans continue to grow. Fund assets reachednew highs in 2014, with the United States leading the way.

Global pension plans continue to grow. Fund assets reachednew highs in 2014, with the United States leading the way.

That's the headline news from the TowersWatson “Global Pension Assets Study 2015.” The firm examinedchanges in pension plans' asset portfolios in 16 markets around theworld. At the end of 2014, the total value across all 16 marketswas US$36 trillion. The total value of U.S. pensions' assets was$22.1 trillion, which comes to 127 percent of U.S. GDP. Only in theNetherlands is the cumulative value of pension assets higherrelative to GDP.

|The study found that the enormous size of some pension plans isaffecting their asset allocation choices, according to Mark Ruloff,director of asset allocation with Towers Watson. “Some of thesefunds are so big that they could be referred to as a 'universalowner,'” Ruloff says. “They own a piece of virtually everything.When something bad happens in the world, or there's a catastropheof some sort that has a negative impact on the earth or on thefinancial system in general, then that will have a negative impacton these investors.”

|As a result, Ruloff reports, some pension asset managers areshifting from a “pure finance way of seeing pension investing”—anapproach that focuses only on short-term performance—to an approachthat emphasizes longer-term sustainable growth. “They do not wantto make investments that could potentially be deteriorating theplanet—for example, using water resources to excess,” he says.“They see that investing in a sustainable company is going to havea better impact on their portfolio over the long term.”

|Another trend that the Towers Watson study highlighted is theshift of assets from defined benefit to defined contribution plans.Among the seven largest pension markets, defined contributionassets represent almost half of all assets. In the United States,they represent more than half—58 percent, while 42 percent of allU.S. pension assets reside in defined benefit plans.

| At the same time, pension funds in the world's largestmarkets are shifting their portfolios from equities toward cash andalternative investments. In the United States, holdings of cashincreased from 0 percent in 2004 to 2 percent of all pension planassets at the end of last year. Holdings in “other assets,” whichcomprises investments such as real estate, hedge funds, privateequity, commodities, and even catastrophic bonds in the reinsurancearea, nearly doubled from 16 percent to 29 percent over the sameperiod. Meanwhile, U.S. pensions' equity holdings declined over thepast decade from 60 percent of the total portfolio to just 44percent.

At the same time, pension funds in the world's largestmarkets are shifting their portfolios from equities toward cash andalternative investments. In the United States, holdings of cashincreased from 0 percent in 2004 to 2 percent of all pension planassets at the end of last year. Holdings in “other assets,” whichcomprises investments such as real estate, hedge funds, privateequity, commodities, and even catastrophic bonds in the reinsurancearea, nearly doubled from 16 percent to 29 percent over the sameperiod. Meanwhile, U.S. pensions' equity holdings declined over thepast decade from 60 percent of the total portfolio to just 44percent.

“Pension funds are investing in all sorts of things outside thenorm of the typical equity/bond tradeoff,” Ruloff explains.“They're shifting from equities into these other types ofinvestments to get more diversification.” And that's not their onlychange in risk management strategy. “It's not just a matter of theasset class itself,” Ruloff says. “They're moving away from theequity risk premium toward other return drivers. For example, thinkof private equity. It definitely has an equity risk premium, but inprivate equity there's also an illiquidity premium, so pensions aretrying to get that illiquidity premium as well.”

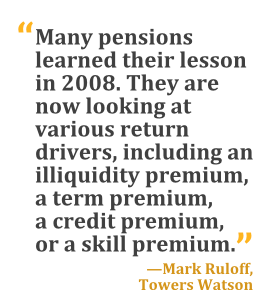

||These shifts reflect an improvement in pension risk management at U.S. entities, he adds. “Manypensions learned their lesson from the crisis in 2008. Before then,some may have thought they were diversified by being in large-capstocks, small-cap stocks, international equities, and emergingmarkets. But those were all equities, and they went down together.So they are now thinking, 'How can I diversify away from the equityrisk premium?' They're looking at various return drivers, includingan illiquidity premium, a term premium, a credit premium, or askill premium—for example, when you invest with a hedge fundmanager who is hopefully going to bring you some skill.”

| One nuance in this trend, which the survey didn't parseout, is how different types of pension plans might be reactingdifferently to current economic factors. Ruloff says Towers Watsonhas noticed recently that corporate pensions and government plansare taking significantly different approaches to asset management,particularly in their bond investments. Overall, U.S. pensions'bonds as a proportion of all assets rose very slightly over thepast decade, from 24 percent in 2004 to 25 percent at the end oflast year. But that's not the whole story.

One nuance in this trend, which the survey didn't parseout, is how different types of pension plans might be reactingdifferently to current economic factors. Ruloff says Towers Watsonhas noticed recently that corporate pensions and government plansare taking significantly different approaches to asset management,particularly in their bond investments. Overall, U.S. pensions'bonds as a proportion of all assets rose very slightly over thepast decade, from 24 percent in 2004 to 25 percent at the end oflast year. But that's not the whole story.

“Corporate pension plans have been more focused on hedging theirliabilities, and perhaps increasing their allocation to bonds, overthe past 10 years,” Ruloff says. “But public pension plans are morefocused on attempting to achieve their expected rate of return andtherefore have been moving away from bonds because of the low-yieldenvironment.”

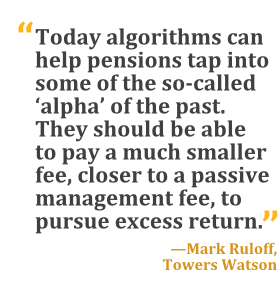

|What trends does Towers Watson expect to emerge on futureiterations of this survey? One prediction is that a more effective“value chain” will soon guide pension asset management decisions.“Today algorithms can help pensions tap into some of the so-called'alpha' of the past, the outperformance of the asset portfoliocompared with equity markets,” Ruloff says. “So plans shouldn't bepaying a lot for that. They should be able to pay a much smallerfee, closer to a passive management fee, for using an algorithm topursue the excess return.”

|For plan sponsors managing funds whose cumulative asset valuesexceed the annual domestic output of the U.S. economy, the prospectof lower fees is a bright spot on a horizon otherwise clouded withuncertainty.

|

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.