As anyone who regularly deals with supply chain issuesknows, buyers and suppliers of goods and services usually haveconflicting interests. Supply chain managers at most companies areunder pressure to improve the company's cash efficiency, usually by extending paymentterms to their suppliers. But many suppliers lack the financialstrength or flexibility to adjust to longer payment terms. Forexample, if a supplier already has a highly leveraged balancesheet, increasing bank borrowing to finance short-term workingcapital may be prohibitively expensive. Extended payment terms mayalso expose suppliers to increased commodity or foreign exchangerisk.

As anyone who regularly deals with supply chain issuesknows, buyers and suppliers of goods and services usually haveconflicting interests. Supply chain managers at most companies areunder pressure to improve the company's cash efficiency, usually by extending paymentterms to their suppliers. But many suppliers lack the financialstrength or flexibility to adjust to longer payment terms. Forexample, if a supplier already has a highly leveraged balancesheet, increasing bank borrowing to finance short-term workingcapital may be prohibitively expensive. Extended payment terms mayalso expose suppliers to increased commodity or foreign exchangerisk.

When a large, well-capitalized company is buying goods orservices from a small or highly leveraged supplier, it may be in aposition to use its own balance sheet to support the supplier. A number ofstrategies have emerged in recent years to help buyers andsuppliers leverage the buyer's stronger financial position to helpthe supplier access lower-cost liquidity, often so that thesupplier can then offer the buyer extended payment terms. Most ofthese strategies involve monetization of the supplier's tradeaccounts receivable.

|The most common forms of trade receivables monetization includeopen-account–based supply chain finance andnegotiable-instrument–based supply chain finance. Together, thesetwo strategies are often referred to as “structured vendor-payablesfinance” or “reverse factoring.” A third, related strategy isnon-recourse receivables purchase, which is often incorrectlyreferred to as “factoring.”

|How Open-Account Supply Chain Finance Works

|An open-account structured vendor-payables program involves thesale of receivables owned by various suppliers and owed by oneparticular buyer. The suppliers sign up to negotiate and sell theirreceivables to investors via a bank or another company running anInternet-based platform. To maximize economies of scale, a buyerusually wants to have a number of suppliers taking part in itsopen-account program.

| Dependingon the size of the supplier base, the investors purchasing thereceivables generally consist of a single bank or a small group ofbanks, although receivables are sometimes sold on a blind tradingplatform, in which case they may be purchased by any number ofinvestors. The universe of possible investors is usually made up ofthe relationship banks of the buyer, but this is not always thecase. In recent years, a number of alternative investors such ashedge funds and insurance companies have also appeared in themarket.

Dependingon the size of the supplier base, the investors purchasing thereceivables generally consist of a single bank or a small group ofbanks, although receivables are sometimes sold on a blind tradingplatform, in which case they may be purchased by any number ofinvestors. The universe of possible investors is usually made up ofthe relationship banks of the buyer, but this is not always thecase. In recent years, a number of alternative investors such ashedge funds and insurance companies have also appeared in themarket.

The platforms on which receivables are submitted, approved, andsold tend to be similar across most open-account structuredvendor-payables programs. A supplier will sell goods or services tothe buyer, generating an invoice that it posts on the supply chainfinance platform for the buyer's confirmation. Once the buyerconfirms the invoice as valid, the related receivable becomeseligible for purchase by an investor. Only confirmed invoices areeligible for purchase, so a specific transaction can be sold onlyif both the supplier and the buyer agree to have it sold.

|In confirming the invoice, the original transaction's buyeragrees that it will pay the investor the full amount of the invoiceon its due date without any claim, abatement, deduction, reduction,or offset of any kind. This confirmation enables the investor tolook directly to the buyer for payment. The buyer may still requestdeductions and make similar claims against the supplier, with thoseoffsets potentially applying to future invoices, but the buyer willnot be permitted to challenge the amount owed on the receivablesold to the investor.

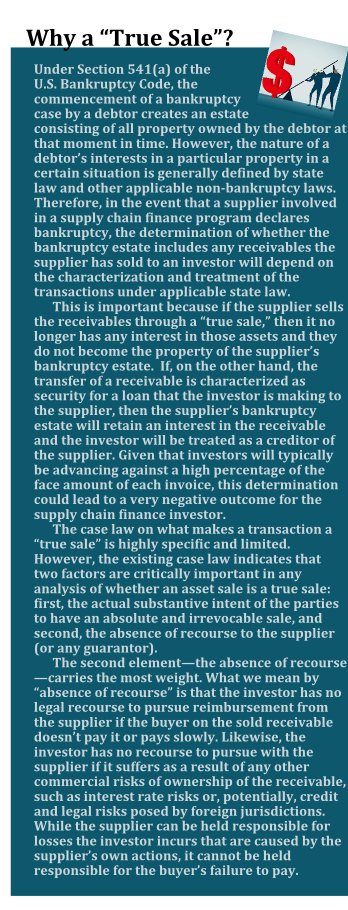

||The investor's agreement with the supplier sets out a formulafor determining the purchase price on all offered invoices.Typically the price is equal to the face value of the invoice minusa discount calculated based on the credit profile of the buyer—notthe supplier—as well as the number of days to maturity of thereceivable. If the supplier and investor elect to consummate thesale of a particular invoice, then the receivable represented bythe invoice is sold on a non-recourse basis to the investor in alegal “true sale.” (See the sidebar Why a “True Sale”?) Byutilizing a true sale, the investor can generally focus itsunderwriting on the underlying credit profile of the buyer andignore the credit of the supplier.

| When the sale of a receivable closes, the buyer will benotified. Then on the scheduled maturity date of the invoice, thebuyer will owe the investor the full face amount of the invoice.The difference between the buyer's payment to the investor and theinvestor's discounted payment to the supplier constitutes theinvestor's fee for participating in the transaction. This is oftenthe only fee that the investor charges; the buyer usually pays nofee on this type of transaction. Also, if the investor is thebuyer's cash management bank, the buyer may not have to modify itscash disbursement operations to pay the investor rather than thesupplier. In many cases, the investor simply debits a pre-agreedbank account for the amount of each sold receivable on the invoicematurity date.

When the sale of a receivable closes, the buyer will benotified. Then on the scheduled maturity date of the invoice, thebuyer will owe the investor the full face amount of the invoice.The difference between the buyer's payment to the investor and theinvestor's discounted payment to the supplier constitutes theinvestor's fee for participating in the transaction. This is oftenthe only fee that the investor charges; the buyer usually pays nofee on this type of transaction. Also, if the investor is thebuyer's cash management bank, the buyer may not have to modify itscash disbursement operations to pay the investor rather than thesupplier. In many cases, the investor simply debits a pre-agreedbank account for the amount of each sold receivable on the invoicematurity date.

Using Negotiable Instruments Instead ofReceivables

|An open-account vendor-payables program is not the ideal supplychain finance solution for every buyer. Open-account programs relyon the sale of accounts receivable under Article 9 of the UniformCommercial Code (UCC). The UCC provides an easy and predictable wayto finance or sell intangible assets like receivables in the UnitedStates. However, in some non-U.S. jurisdictions, sellingintangibles can be cumbersome and may expose the investor toadditional legal risks, such as risks associated with fraud andinsolvency.

|Even in the United States, an investor purchasing a receivableneeds to record that purchase under the UCC filing system in one ormore states. Depending on the supplier's existing creditarrangements, the investor may also need to obtain lien releasesfrom the supplier's lenders before the receivable can be sold.

|To bypass these challenges, buyers sometimes opt to implement analternative structure that utilizes negotiable instruments insteadof accounts receivable. A negotiable-instrument–based program issimilar in many respects to an open-account program. The suppliersubmits invoices, which the buyer approves. However, the supplieror buyer also creates a “draft,” a “bill of exchange,” a“negotiable promissory note,” or another form of negotiableinstrument. These instruments are governed by U.S. law.

|Once created, the instrument is then sold by the supplier to aninvestor using a process similar to that of open-accountreceivables sales, but it usually involves a physical embodiment ofthe negotiable instrument. The investor takes physical possessionof the instrument upon purchase, then presents the instrument tothe buyer for payment on the invoice maturity date. In some cases,the creation, acceptance, assignment, and presentment of theinstrument are handled entirely by the investor, with no need forthe supplier and buyer to exchange a physical document.

||Because these instruments are governed by U.S. law and owed by aU.S. buyer, they are free of most foreign-law constraints, even ifthe supplier is a non-U.S. company. Thus, negotiable instrumentsallow an investor working with a U.S.-based buyer to purchasereceivables from a wider universe of suppliers than it could underan open-account program.

| Theother key advantage of an instrument-based program is what's knownas the “holder in due course” doctrine. Section 3-302 of the UCCdefines a “holder in due course” as one who takes an instrument forvalue in good faith, absent any notice that it is overdue, has beendishonored, or is subject to any defense against it or claim to itby any other person. If the purchaser of a negotiable instrument isa holder in due course, the purchaser may not be subject to many ofthe defenses available to creditors under Article 9 of the UCC.This means that, unlike with open-account programs, invoices soldas negotiable instruments will give the investor priority againstclaims of the supplier's other creditors, including in a bankruptcyproceeding. Investors should take note, however, that while theseprograms are built on solid legal foundations, there is little orno case law on the issue of whether an investor in this type ofsupply chain program would qualify as a holder in due course. Inaddition, investors often do not need to deal with the UCCrecording system when purchasing negotiable instruments.

Theother key advantage of an instrument-based program is what's knownas the “holder in due course” doctrine. Section 3-302 of the UCCdefines a “holder in due course” as one who takes an instrument forvalue in good faith, absent any notice that it is overdue, has beendishonored, or is subject to any defense against it or claim to itby any other person. If the purchaser of a negotiable instrument isa holder in due course, the purchaser may not be subject to many ofthe defenses available to creditors under Article 9 of the UCC.This means that, unlike with open-account programs, invoices soldas negotiable instruments will give the investor priority againstclaims of the supplier's other creditors, including in a bankruptcyproceeding. Investors should take note, however, that while theseprograms are built on solid legal foundations, there is little orno case law on the issue of whether an investor in this type ofsupply chain program would qualify as a holder in due course. Inaddition, investors often do not need to deal with the UCCrecording system when purchasing negotiable instruments.

On the other hand, this type of program is more cumbersome thanan open-account program and may be unfamiliar to many U.S.suppliers.

|Key Considerations in Structured Vendor-PayablesPrograms

|Buyers considering implementing a structured vendor-payablesprogram will want to consider a few key issues. The first, andperhaps the most obvious, is that these programs require closecoordination among the buyer's treasury, legal, and purchasingfunctions. The initial negotiation with prospective investors isusually led by a company's treasury and legal teams, but thepurchasing function is generally responsible for on-boardingsuppliers and maintaining the program. A lack of coordination amongthese departments can easily lead to implementation of a suboptimalprogram and underutilization of the program by the company'ssuppliers.

|The second key issue concerns the accounting treatment of astructured vendor-payables program. For the buyer, the chiefaccounting priority is usually to avoid having to reclassify theaffected payables as short-term indebtedness on its balance sheet.Such reclassification is usually unfavorable because it increasesthe company's balance sheet leverage, which may affect financialcovenants and ratios contained in loan agreements, indentures, andemployee compensation agreements, among other contracts.

|Unfortunately, no specific U.S. GAAP guidance addresses theaccounting for structured vendor-payables arrangements. In 2003 and2004, Securities and Exchange Commission (SEC) staff madeconference presentations outlining general guidance for companiesthat report to the SEC1. They noted that inspecific situations, certain characteristics of structuredvendor-payables arrangements may cause supplier payables to bereclassified on the balance sheet of the buyer as short-termindebtedness. Lacking specific GAAP guidance, most auditors usethese comments as a guide in making determinations regardingbalance sheet treatment.

|Auditors are more likely to require indebtedness treatment whena structured vendor-payables arrangement has any of the followingcharacteristics:

- The economic terms and character of the obligations owed to theinvestor are different from the obligations the buyer previouslyowed to the supplier.

- The buyer agrees to cover the supplier's financing costs orother obligations to the investor.

- Supplier participation in the program is mandatory.

- The buyer has excessive control in the negotiation ofdocumentation between the supplier and the investor.

Most legal documentation used by sophisticated investors instructured vendor-payables programs is designed to address theseconcerns. However, buyers should be sure to discuss theimplementation of any supply chain finance solution with theirinternal and external auditors well before they start rolling out aprogram.

|1. SEC Staff Speeches: 2003 and 2004 AICPA NationalConference on Current SEC and PCAOB Developments. Robert Comerford:“Classification and disclosure of certain trade accounts payabletransactions involving an intermediary.”

|An Alternative: Non-Recourse ReceivablesPurchase

|A close relative of structured vendor-payables programs is anon-recourse receivables-purchase solution. This is often describedas a “factoring” arrangement, but that's a misleading designationbecause these facilities have little in common with the small-scalefinancing mechanism traditionally provided by factoring companiesin the United States.

|Much like an open-account payables transaction, areceivables-purchase facility entails a supplier selling one ormore investors its rights to certain accounts receivable owed by aparticular buyer. A big difference is that the buyer's involvementis minimal beyond introducing the investor to its supplier base.The buyer does not have to confirm each invoice before thereceivable can be sold. In fact, an investor might provide thesetypes of facilities to suppliers without the buyer even knowingabout it. Another benefit for the buyer is that areceivables-purchase facility generally does not have anyaccounting complications for the buyer.

|For suppliers, these facilities can provide much higher advancerates and lower overall costs compared with more traditionalasset-based loan facilities. They can also assist suppliers inmonetizing excess customer concentrations that would be excluded bythe borrowing-base funding formulas found in most asset-based loan(ABL) agreements or accounts receivable securitizations.Traditional ABL and securitization facilities will often containstrict concentration limits on the percentage of receivables of aparticular obligor which may be used to generate fundingavailability. These limits can often be as low as a few percentagepoints. For many suppliers to industries with a small number ofdominant buyers (e.g., retail, auto) these limitations can resultin the supplier being unable to monetize a large percentage of itsoutstanding receivables.

|Finally, unlike a structured vendor-payables program, which willusually require a great deal of work at the buyer to implement androll out among its supplier base, these types of transactions canbe executed quickly and sometimes even on a one-off basis.

|The downside of these facilities for the investor is that thereis no direct confirmation from the buyer that it will pay theinvestor. Thus, investors in these facilities are very keen to makesure that what they are acquiring from the supplier is a valid andenforceable claim against the buyer. The investor usually conductssignificantly more due diligence on suppliers before entering thesetransactions, and it pays close attention to making sure that thesupplier is transferring the receivables via a legal true sale.(See the sidebar Why a “True Sale”?)

|The Future of Trade ReceivablesMonetization

|All three of these types of arrangements help suppliers accessimproved liquidity, whether or not their buyer is looking forextended payment terms. Most of these strategies can be implementedwith few, if any, direct expenses to the buyer.

|Trade receivables monetization is particularly popular in theconsumer retail, automotive and other manufacturing, chemical, andpharmaceutical sectors. Buyers in these industries tend to haveextensive supply chains that are global in scope, and generally thebuyers are larger, with a more favorable credit profile, than mostof their suppliers. However, the benefits of monetizing tradereceivables aren't limited to a few business sectors. Thesestrategies may be utilized by any buyer with a solid credit ratingand a diverse supplier base, or by any supplier whose buyers havehigh credit quality.

|A lot is happening in supply chain finance, and it seems likelythat the recent growth in popularity of these programs willcontinue well into the future. Based on our own pipeline ofprojects at Mayer Brown, we expect to be talking about structuredtrade receivables solutions for a long time. Stay tuned.

|————————————————

| Massimo Capretta is counsel in Mayer Brown'sChicago office and a member of the firm's banking and financepractice.

Massimo Capretta is counsel in Mayer Brown'sChicago office and a member of the firm's banking and financepractice.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.