With interest rates poised to move higher in 2016, manytreasury professionals are hoping for a return to the good old daysof decent yields in safe investments for their corporate andinstitutional cash. However, the world they'll encounter when ratesfinally do rise will be very different from the higher-rateenvironment they left eight years ago.

With interest rates poised to move higher in 2016, manytreasury professionals are hoping for a return to the good old daysof decent yields in safe investments for their corporate andinstitutional cash. However, the world they'll encounter when ratesfinally do rise will be very different from the higher-rateenvironment they left eight years ago.

Since the financial crisis, the near-zero rates—combined with alengthy period of guarantees on demand deposits—helped create a“business as usual” mind-set among many treasury professionals. But2016 promises to be a pivotal year that will usher in a new era incash management, requiring new ways of thinking.

|Compared with a decade ago, today's cash investment landscape isshaped by higher risk awareness, more sensitivity to liquiditycosts, and stricter systemic regulation. Dodd-Frank and Basel IIIare already causing the biggest banks to limit uninsured deposits.And when money market reforms are instituted in October 2016,institutional money funds will have less stability, greater risk,and lower yield potential.

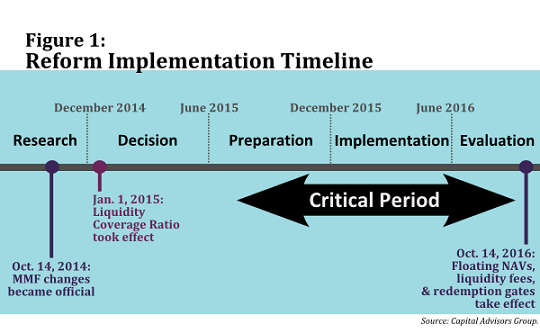

|Mindful of the timing and potential impact of these events (seeFigure 1, below), treasury professionals have already started toposition themselves for dramatic changes in the way they managetheir short-term cash. Many are changing their written investment policies to accommodate morealternatives to traditional deposits and money market funds. Atthe same time, many are also upgrading their research and riskmanagement capabilities to help safeguard principal and liquidityin a changing risk/return environment.

|As they plan for 2016, treasury professionals will confrontchallenges on at least three fronts:

- While prime money market funds will still be available for cashmanagement, their floating net asset values (NAVs) will change the utility theyoffer, and their new risk/reward equation will require closescrutiny.

- Supply of both traditional bank deposits and money marketinstruments may be constrained, requiring consideration ofalternatives.

- Cash managers may feel compelled to venture into less-familiarterritory with a new mix of traditional and non-traditional investments as they seek todeliver both liquidity and safety of principal.

By paying close attention to each of these challenges in thecritical transition period early next year, treasury professionalswill acquire tools to help maintain their desired mix of safety,liquidity, and yield throughout 2016 and beyond.

|Staying Afloat with Floating NAV MoneyFunds

|By the fall of 2016, when the dust has finally settled on moneymarket reform, institutional prime money market funds will haveadopted floating NAVs, and will have the option of imposingliquidity fees and redemption gates to limit investor withdrawalsin times of stress. These dramatic structural changes, asprescribed by the 2014 rule amendment by the Securities andExchange Commission (SEC), may fundamentally alter the desirabilityof money market funds as a cash management tool. But currently,little is known about what liquidity characteristics institutionalprime funds will have in October 2016. No one knows exactly howinstitutional shareholders will accept the reformed prime moneyfund products, how effective liquidity-monitoring tools will be, orwhether intraday liquidity will be possible.

|The prospect of liquidity fees and redemption gates, inparticular, are creating concern among corporate treasurers. If afund doesn't restrict daily redemptions, liquidity couldpotentially evaporate quickly. For example, Treasury debt andagency debt that matures within 60 days is not cash in a literalsense. In a rising-interest-rate environment, a money fund sellingthese instruments to raise cash might inadvertently create realizedlosses, which could potentially lead to NAV erosion. NAVdeterioration might encourage more redemption, exacerbating theliquidity shortage. Likewise, a few shareholders with a largeconcentration of shares might simultaneously decide to redeemshares from funds with low liquidity levels in periods of marketvolatility, resulting in a self-perpetuating liquidity drain.Shareholders in institutional funds that commingle pooled assetswill need a comprehensive understanding of these and otherliquidity risks in order to protect themselves.

|

Because of the liquidity risks, corporate cash managers willlikely start to balance their portfolios with multiple liquidityinstruments that complement one another. The portfolios willinclude the new institutional prime money funds with floating NAVs,but will not be limited to them. For example, a corporate portfoliomight also include a government money fund with a stable NAV anddirect purchases of government and other highly liquid securities.Government-fund shares may be used to accommodate unforeseenintraday liquidity needs, while institutional prime fund shares mayprovide extra yield potential and function as sources of next-dayliquidity. Then a laddered portfolio of government and othersecurities may be used to provide backup liquidity throughstaggered maturities or open-market sales in the unlikely eventthat liquidity becomes inaccessible in prime funds.

|Alternatives to Bank Deposits and Prime MoneyFunds

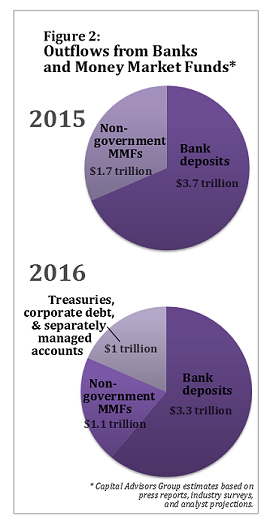

|In 2016, regulations and market forces may reduce theavailability and yields, and increase uncertainty about risk andliquidity, for both bank deposits and the new iteration ofinstitutional money market funds. The net effect may be significantoutflows from deposits and non-government prime money market funds.Capital Advisors Group estimates that more than $1 trillion incorporate cash which is currently held in bank deposits and moneyfunds may migrate into new or different accounts in the comingyear. Specifically:

|

- Reforms that strengthen banks' balance sheet liquidity havemade traditional deposits more expensive and less available,leading large banks to reduce their proportion of uninsureddeposits of corporate cash. Capital Advisors Group estimates thatas much as $450 billion of the $3.7 trillion* held inovernight deposits at the top six global systemically importantbanks might move into safe but low-yield government securities andother vehicles.

- At the same time, with SEC-mandated changes in prime moneyfunds increasing potential risk and reducing potential liquidityand yields, we estimate that as much as $615 billion of the$1.7 trillion in corporate cash held in institutional money fundswill move into low-yield government funds and other vehicles (seeFigure 2).

Most cash investment policies subscribe to the objectives ofprincipal stability, liquidity, and income potential. Untilrecently, prime money market funds achieved all three objectivesreasonably well, and bank deposits may have accomplished the firsttwo. But if the hands-off liquidity management practice of leavingall cash balances in a few bank accounts or money market fundsbecomes less attractive from a risk-reward perspective, what arethe alternatives?

|An obvious destination for cash migrating from deposits andprime money funds is to government-only money market funds, whichare not subject to floating NAVs, liquidity fees, or redemptiongates. However, the influx of cash into this safe haven with alimited supply can be expected to depress yields. Evidence of thistrend came in October 2015 with the first-ever sale of three-monthTreasuries with a yield of zero.

|Therefore, many corporate and institutional cash managers areconsidering supplemental alternatives to government securities,including direct purchases of short-term commercial paper andestablishment of separately managed accounts. Direct purchasesrequire hands-on investment and accounting expertise, liquiditymanagement, and risk and credit monitoring. However, investing inresearch and counterparty risk management capabilities, and/oropting to employ separately managed liquidity accounts maintainedby an advisory firm with appropriate expertise, can effectivelyaddress those issues.

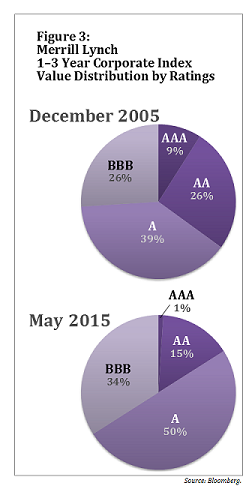

||Corporate treasurers wanting to change their cash-investment mixtruly have a universe of options, each of which requires carefulconsideration. One of the largest factors impacting alternativeinvestment strategies has been the contraction in supplyof high-grade securities rated AA or higher (see Figure 3,below). Gone are the days when a treasurer could easily construct acash portfolio solely with non-government AA and A-1+ credits.Today many investors are considering putting their cash to work ininstruments with lower investment-grade ratings.

|Those treasurers who can buy corporate bonds, either directly orthrough custom-tailored separate accounts, may benefit from awidening of spreads and increasing supply. Over the pastdecade, the dollar value of corporate bonds with an A rating astracked in the Merrill Lynch 1-to-3-Year Corporate Index hasincreased almost fourfold, and supply of investment-grade BBBsecurities in the index has increased even more.

| Corporate bonds with BBB ratings have the positiveattributes of broader supply, improved risk diversification,moderate default and ratings migration risk, and attractive yieldpotential. Of course, these attributes need to be viewed in thecontext of a treasury organization's investment policies for itsgeneral fixed-income portfolio, which tend to emphasize principalpreservation and liquidity more than income.

Corporate bonds with BBB ratings have the positiveattributes of broader supply, improved risk diversification,moderate default and ratings migration risk, and attractive yieldpotential. Of course, these attributes need to be viewed in thecontext of a treasury organization's investment policies for itsgeneral fixed-income portfolio, which tend to emphasize principalpreservation and liquidity more than income.

Investors should expect lower market liquidity from BBB debt,and would be well-advised to use these investments only as part ofa conservatively constructed core portfolio. But if one starts witha core base of high-quality liquid investments in a portfolio, BBBdebt may be layered in as an attractive risk diversifier and yieldenhancer.

|In essence, as the short-term government securities continue tobe haunted by supply constraints and stressed by demand, treasurersconsidering individual corporate securities or separately managedaccounts should have adequate options.

|The Right Investment Mix for Safety, Liquidity, andYield

|A key objective for many managers of institutional cash is toreduce unnecessary balances in overnight bank deposits and moneymarket funds and to deploy cash in a diversified portfolio ofhigh-quality instruments. Achieving the right balance of safety,liquidity, and yield becomes more challenging as the portfoliogrows in complexity.

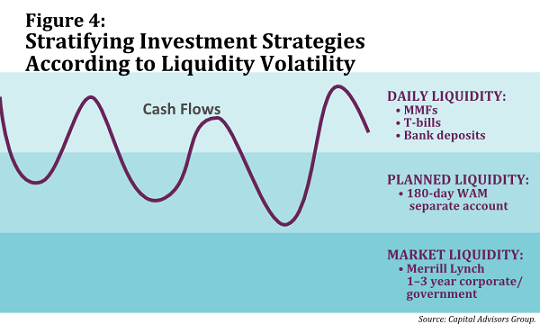

|Cash investors constructing portfolios with a mix of deposits,money market funds, and direct investments often find that astratified investment strategy works well. Dividing cash balancesinto specific categories and adopting different strategies for eachhelps treasurers achieve their liquidity and safety goals withappropriate returns. Many divide liquid balances into threesegments according to liquidity volatility: daily, planned, andmarket (see Figure 4, below).

||

Daily liquidity. Maintaining sufficient balances for dailycash use and reserves for unanticipated fluctuations is necessaryto ensure that the company can meet its daily liquidityrequirements. Appropriate vehicles for holding this cash mayinclude transactional bank deposits, stable-NAV money market fundsand other pooled investments, and overnight repos.

|

Planned liquidity. For seasonal cash needs and plannedexpenditures, a liability-driven strategy with targeted maturitiesmay provide higher income opportunity without sacrificingliquidity. Accounting rules may vary, but many such portfoliosoffer principal stability with “held to maturity” treatment.Appropriate instruments may include term deposit accounts, Treasuryand agency securities, and high-quality corporate and financialcredits.

|Market liquidity. Sometimes referred to as “core cash” or“strategic balances,” market liquidity balances represent excesscash that isn't governed by near-term liquidity constraints. Lessneed for liquidity enables cash managers to employ more flexible strategies with the goal ofmaximizing return potential. In addition to proceeds that flowin as securities mature, liquidity may come from the secondarymarket. With a moderately longer time horizon, portfolio strategiesmay also include high-quality asset-backed and mortgage-backedsecurities.

|Stratifying cash balances into several categories, and applyingtargeted strategies to each category, helps to delineate the threeobjectives of cash management: safety of principal, stability, andincome potential. As it becomes increasingly difficult to deliveron all three objectives with deposits and money funds alone, astratified approach may allow cash managers to pick the beststrategies suited for each need, utilizing a combination ofdeposits, money market funds, and direct purchases in acomprehensive approach.

|Managing Credit and Risk in the New Era

|Managing risk through the upcoming period of market change willdemand new levels of attention and caution from all stakeholders.Therefore, as cash investors in 2016 try to understand the newlyconstituted money market funds and examine a new mix of investmentalternatives beyond bank deposits and money funds, they must alsoinvest time and energy in comprehensive credit and risk managementcapabilities.

| Credit approval for a cash portfolio is different from theprocess used for other fixed-income investments. Cash investorshave unique credit requirements, including liquidity needs, lowthresholds for principal loss, a tendency to hold securities tomaturity, and a conservative bias placing a higher priority onpreservation of principal than on income. Another consideration isthe available supply of suitable short-term investments.

Credit approval for a cash portfolio is different from theprocess used for other fixed-income investments. Cash investorshave unique credit requirements, including liquidity needs, lowthresholds for principal loss, a tendency to hold securities tomaturity, and a conservative bias placing a higher priority onpreservation of principal than on income. Another consideration isthe available supply of suitable short-term investments.

Treasury professionals are advised to follow a rigorous protocolin selecting appropriate securities and then managing andmonitoring the credit status of those securities. A comprehensivecredit management program—including initial screening, macroscreening, establishment of internal ratings, and ongoingmonitoring and surveillance of the portfolio—is a start. Theprocess should also entail mitigation of risk through developmentof plans for an effective response to, and management of, anycredit event.

|The stakes have never been higher for corporate treasuryprofessionals, who will confront more dramatic changes in corporatecash management in 2016 than they have in years. The good news isthat with the right preparations, including a renewed focus oncredit and risk management and consideration of alternativeinvestments, they will have the tools they need to succeed.

|—————————————

| Ben Campbell is founder and CEO of CapitalAdvisors Group, Inc., an independent investment advisor based inNewton, Massachusetts, that specializes in institutional cashinvestments, risk management, and debt financing. In June2011, Treasury & Risk named Ben one of the “100 MostInfluential People in Finance.”

Ben Campbell is founder and CEO of CapitalAdvisors Group, Inc., an independent investment advisor based inNewton, Massachusetts, that specializes in institutional cashinvestments, risk management, and debt financing. In June2011, Treasury & Risk named Ben one of the “100 MostInfluential People in Finance.”

Lance Pan, CFA, is the director of investmentresearch and strategy for Capital Advisors Group.

Lance Pan, CFA, is the director of investmentresearch and strategy for Capital Advisors Group.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.