Eight years after the beginning of the financial crisis,regulators and financiers are still searching for the optimalbalance between encouraging global growth and implementingregulations on trade finance instruments that are adequate,equitable, and risk-aligned.

Eight years after the beginning of the financial crisis,regulators and financiers are still searching for the optimalbalance between encouraging global growth and implementingregulations on trade finance instruments that are adequate,equitable, and risk-aligned.

This is a crucial discussion, especially for developing nationsand the companies looking to do business there. Trade financeassists buyers and sellers by filling in the trade cycle fundinggap and removing the payment risk and supply risk. It is thereforea key factor in emerging-market development, as governments andregulators around the world recognize.

|The International Chamber of Commerce's (ICC's) Trade Registerreport presents a global view of the credit risk profiles of tradeand export finance transactions, focusing on credit-related defaultand loss experience. This encompasses short-term products, whichtypically have a maturity of less than one year, such as issuedimport letters of credit (L/Cs), confirmed export L/Cs, import andexport loans, and performance guarantees and standby L/Cs. Thescope of medium- to long-term trade finance products is limited toproducts where an OECD Export Credit Agency (ECA) has provided astate-backed guarantee or insurance to the trade finance bank.

|Trade finance is critical to the expansion of trade. Without it,trade remains constrained, impacting economic development andincreasing instability across all sectors, countries, andpopulations. Yet global banks have been reducing their counterpartynetworks in the developing world, and thus reducing the amount oftrade finance available in this region.

|There are many reasons behind the withdrawal of global banksfrom the emerging markets. One is the high cost of compliance anddue diligence incurred when operating in this area. Another is theglobal regulatory climate, including the capital requirements imposed by Basel III, which reduce theamount of lending a bank can offer at each level of capitalreserves it has on hand. What's more, anti-money laundering (AML)and know-your-customer (KYC) requirements, although essential, haveweighed banks down with new investigative, tracking, and reportingresponsibilities.

|Bank de-leveraging and tighter global credit conditions—drivenin part by financial, regulatory, economic, and politicalconsiderations—pose a serious challenge to trade growth.

|

Growing Trade Finance Gap

Industry sources estimate that the average cost of maintaining abasic correspondent banking relationship has increased at leastfive times since the peak of the financial crisis. Indeed, in ICC's2015 Global Survey on Trade Finance report—which collates feedbackon the timing and calibration of reforms, and includes fullindustry representation and coverage—46 percent of banks reportedtermination of relationships, due at least in part to the addedcost or complexity of those relationships' maintenance.

| Thishas significant repercussions on emerging markets, which aredependent on trade finance as an engine for growth. Small tomidsize enterprises (SMEs), in particular, experience higher levelsof unmet demand for trade finance, for a variety of reasons rangingfrom risk profile to issues of bankability and the need forsignificant advisory support. The termination of correspondentbanking relationships denies emerging markets access to globalsupply chains and trade corridors, as well as access to liquiditythey need for growth and expansion. Considering that emergingmarkets continue to take on an increasingly larger share of globaltrade, and account for around 42 percent of global exports, a lackof trade financing clearly slows global growth rates.

Thishas significant repercussions on emerging markets, which aredependent on trade finance as an engine for growth. Small tomidsize enterprises (SMEs), in particular, experience higher levelsof unmet demand for trade finance, for a variety of reasons rangingfrom risk profile to issues of bankability and the need forsignificant advisory support. The termination of correspondentbanking relationships denies emerging markets access to globalsupply chains and trade corridors, as well as access to liquiditythey need for growth and expansion. Considering that emergingmarkets continue to take on an increasingly larger share of globaltrade, and account for around 42 percent of global exports, a lackof trade financing clearly slows global growth rates.

The ICC survey also suggests that the trade finance gap may beincreasing. Fifty-three percent of respondents perceive a shortfallbetween banking customers' demand for trade finance and theirability to satisfy that demand. Closing this gap requirescontinuing collaboration between trade banks and other privatesector sources, together with ECAs and multilateral developmentbanks—both groups critical to ensuring adequate availability oftrade financing. Additionally, industry stakeholders haverecognized the need to attract non-bank capital in support of tradefinance, and measures are being taken to better communicate toinvestment-pool managers about the nature of trade finance.

| Advocacyand collaboration on the regulatory side, based in part on the ICCTrade Register data, underpin ongoing efforts to find the rightbalance between the need for growth-driven trade (enabled by tradefinance) and the need for appropriate, risk-aligned capitaladequacy and compliance regulation. Ultimately, this has freed upbank balance sheet capacity to underwrite more trade financebusiness. As illustrated in the Trade Register report, there havebeen several substantive successes to date, though it is clear thatcontinuing engagement with the Basel Committee, along with regionaland national regulatory authorities, is necessary on this front.

Advocacyand collaboration on the regulatory side, based in part on the ICCTrade Register data, underpin ongoing efforts to find the rightbalance between the need for growth-driven trade (enabled by tradefinance) and the need for appropriate, risk-aligned capitaladequacy and compliance regulation. Ultimately, this has freed upbank balance sheet capacity to underwrite more trade financebusiness. As illustrated in the Trade Register report, there havebeen several substantive successes to date, though it is clear thatcontinuing engagement with the Basel Committee, along with regionaland national regulatory authorities, is necessary on this front.

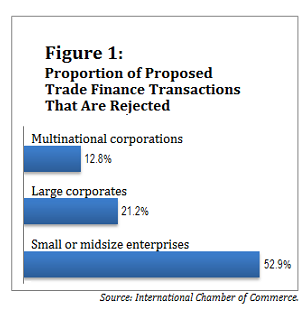

SMEs in riskier markets bear the brunt of the trade finance gap.These businesses account for 46 percent of proposed trade financetransactions, but only 47 percent of these transactions areaccepted; more than half are rejected. By comparison, 79 percent oftrade finance transactions for larger corporates are accepted. (SeeFigure 1.) This gap has a significant impact on global development;the Asian Development Bank estimates that unmet demand for tradefinance around the world, among companies of all sizes, amounts toUS$1.1 trillion.

|Trade Finance Is Low-Risk

Although the trade finance gap clearly persists, there is reasonfor optimism. In the ICC Global Survey on Trade Finance, 61 percentof respondent banks reported increases in their capacity to meettrade finance demand. A key reason behind this positive trend isthat banks are becoming increasingly aware of the importance, andvery effective mitigation, of the risks inherent in tradefinance.

|Indeed, in the latest edition of ICC's Trade Register,traditional trade finance products fare particularly well, both atthe customer and transactional level, and when weighted byexposure. For example, the transaction default rate for short-termexport L/Cs was 0.01 percent between 2008 and 2014, whichcorresponds to a Moody's rating between Aaa and Aa. Figures formedium- to long-term trade finance products are also positive, withan annual loss rate from 2007 to 2014 that is lower than the lossrate reported by Moody's for Aa-rated bonds. In fact, the corporatedefault rate of 0.88 percent for medium- to long-term trade financeproducts, across all asset classes, compares very favorably withthe Moody's default rate of 1.9 percent for all ratedcorporates.

|And even in the event of default, trade finance instrumentsrecord high rates of eventual asset recovery. The median result forall short-term trade finance products is close to 100 percentrecovery. Even with prudent assumptions, the average expected lossfor short-term trade finance is lower for all products than that oftypical corporate exposures.

|

Open and Constructive Dialogue Around TradeFinance

The results of the 2015 Trade Register analysis remain broadlyconsistent with findings over the last seven years, since theinception of the Trade Register, and continue to provide a soundand objective basis for constructive, substantive dialogue andadvocacy with the Basel Committee and other regulatory authorities.Even as we all recognize the need for regulatory oversight aimed atassuring a robust global financial system, it is clear that tradefinance products should be treated as low-risk creditinstruments.

|Of course, opportunities to further balance regulatoryobjectives with trade finance value creation remain, and extend tocompliance and regulatory issues beyond the capital adequacydiscussion. For instance, trade-based money laundering, whichdrives certain types of financial-sector regulation, must befurther explored, considering that only a small portion of suchactivity actually occurs in the context of trade financetransactions.

| Inparticular, there is room for greater communication andunderstanding among bankers, trade financiers, and otherstakeholders so that all parties strive to reach informed decisionsabout the best way forward. As such, the improved tone, approach,and substance of dialogue are all to the good, and mustcontinue.

Inparticular, there is room for greater communication andunderstanding among bankers, trade financiers, and otherstakeholders so that all parties strive to reach informed decisionsabout the best way forward. As such, the improved tone, approach,and substance of dialogue are all to the good, and mustcontinue.

The next phase of the dialogue and advocacy work can veryusefully extend to involving representatives from the clientcommunity of users of trade financing—from treasury and financeexecutives in large multinationals, to entrepreneurs leadingeconomically critical small businesses. The matter of availabilityof trade finance and appropriately risk-aligned regulation of thisbusiness are not fundamentally “bank problems,” but issues ofimportance to trade flows and real economic activity.

|Companies of all sizes can engage in this dialogue and advocacyeffort through various channels, from industry associations tochambers of commerce, to numerous international and multilateralinstitutions active in the financing of international trade andrelated advocacy efforts—which today extend from the ICC to theBasel Committee, the World Trade Organization, the B-20/G-20 annualprocesses, the United Nations system, the World Economic Forum, andnumerous other organizations.

|A concrete first step may be for treasurers to reach out totheir trade financers or to organizations like the ICC BankingCommission, BAFT in Washington, and others to share their views andexperiences, and ultimately to contribute to shaping policy in thisarea.

|The importance of engaging companies and private-sector endclients in this process increases as we shift our attention fromtraditional trade finance mechanisms and instruments to theincreasingly crucial and fast-growing area of supply chain finance, which takes a holistic, ecosystem-levelview of trading relationships and involves multiple commercialrelationships—sometimes supplier communities numberingthousands—touching multinationals as well as micro-enterprises andSMEs, often located in developing economies.

|——————————————————

| Alexander R. Malaket, CITP, is thedeputy head of the executive committee for the InternationalChamber of Commerce (ICC) Banking Commission and president of OPUSAdvisory Services. He has over 25 years of professional experiencein trade, trade finance, investment, financial services, andsenior-level consulting.

Alexander R. Malaket, CITP, is thedeputy head of the executive committee for the InternationalChamber of Commerce (ICC) Banking Commission and president of OPUSAdvisory Services. He has over 25 years of professional experiencein trade, trade finance, investment, financial services, andsenior-level consulting.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.