In July, the Hackett Group released its annual “Working Capital Survey,” an analysis of trends in working capital management among large U.S. businesses. The Hackett Group examined the 2015 financial statements of the nation's 1,000 largest public companies outside the financial services sector and calculated each organization's days sales outstanding (DSO), days payables outstanding (DPO), and days inventory on hand (DIO).

In July, the Hackett Group released its annual “Working Capital Survey,” an analysis of trends in working capital management among large U.S. businesses. The Hackett Group examined the 2015 financial statements of the nation's 1,000 largest public companies outside the financial services sector and calculated each organization's days sales outstanding (DSO), days payables outstanding (DPO), and days inventory on hand (DIO).

This year's report suggests that many companies have been filling their cash coffers by taking advantage of the historically low cost of debt, rather than by launching initiatives designed to improve working capital performance. In fact, at the highest level, working capital performance among the companies included in the analysis is at its lowest point since the 2008 financial crisis.

Treasury & Risk sat down with Craig Bailey, a senior director with the Hackett Group, to get a better sense of what companies have been doing in their working capital management—and what they could and should be doing better.

T&R: At the 30,000-foot level, what are the key take-aways from the Hackett Group's “2016 US Working Capital Survey”?

Craig Bailey: Well, the performance of working capital among large U.S. companies deteriorated in 2015, for the first time in three years. However, a lot of that movement came from the energy sector, which has obviously been facing challenges over the past 12 months. If we strip out oil and gas, and look at all the other companies in this analysis, we see that working capital performance overall—at the level of the cash conversion cycle—stayed pretty static in 2015. But there have been shifts between inventory, receivables, and payables.

T&R: What does your analysis show at the level of DSO, DPO, and DIO?

CB: Receivables have generally stayed pretty flat for quite a while now. The improvement last year was less than 1 percent. That ties in with what we're seeing with our clients as well. Accounts receivable is usually one of the easier areas of working capital for a business to improve. So ever since the financial crisis, we've seen companies putting some effort into collections processes and other internal A/R processes. There was no real change there last year.

In payables, there's been a pretty steady improvement in performance since the financial crisis. And there was another increase in 2015, so no real change in that trend. We're seeing a lot of businesses moving to extend terms. Net-60 is becoming almost standard in the United States, and some companies are pushing that out to 90 or 120 days. I've even come across some organizations pushing terms out even further.

In payables, there's been a pretty steady improvement in performance since the financial crisis. And there was another increase in 2015, so no real change in that trend. We're seeing a lot of businesses moving to extend terms. Net-60 is becoming almost standard in the United States, and some companies are pushing that out to 90 or 120 days. I've even come across some organizations pushing terms out even further.

However, on the other side, we've seen that inventories deteriorated last year. Not massively; if we strip out oil and gas, inventories deteriorated by only 4 percent. But we're seeing this among some of our consulting clients as well. Lots of companies are looking at cost-cutting. Some that haven't done it yet are now looking at offshoring. Other businesses that have moved operations to low-cost countries are finding costs rising in popular offshoring destinations, so they're now looking at moving operations even farther afield. Which may reduce costs, but also extends lead times and extends the supply chain.

T&R: Where should a company start in improving inventory management?

CB: Typically the first step is for management to break down inventory into groupings. Maybe they'll break inventory down into raw materials, interim work, finished goods, and spare parts—whatever groupings make sense for their business. They should look at all of these individual groupings of inventory in isolation, both in terms of dollar value and days in inventory as well. We find that sometimes organizations are looking at the dollar value of a certain type of inventory; then when we go in, we find that another area has a very high number of days, which is where the company's focus should be. So that's the first thing: Break inventory out into meaningful groupings and look at both dollars and days of each grouping.

Then they should look at the drivers of each grouping of inventory, and which of those drivers they can actually influence. There may be a certain number of days that can be defined easily in terms of manufacturing lead times or customer staging requirements, and these are generally non-negotiable. But where are the other drivers coming from? To what extent are they within the organization's control? And which drivers—such as transportation lead times, potentially—are within the company's control, but with tradeoffs attached to them and some cost implications? From there, a company can look at each of these drivers and determine which it can, and should, tackle, and it can move forward with making those improvements.

Then they should look at the drivers of each grouping of inventory, and which of those drivers they can actually influence. There may be a certain number of days that can be defined easily in terms of manufacturing lead times or customer staging requirements, and these are generally non-negotiable. But where are the other drivers coming from? To what extent are they within the organization's control? And which drivers—such as transportation lead times, potentially—are within the company's control, but with tradeoffs attached to them and some cost implications? From there, a company can look at each of these drivers and determine which it can, and should, tackle, and it can move forward with making those improvements.

Success in improving inventory management revolves around taking that step approach, from a total inventory number to understanding the groupings of inventory; understanding the drivers of those groupings; understanding which drivers are most influenceable, what the tradeoffs and risks are; and then identifying action plans to tackle each of those drivers accordingly.

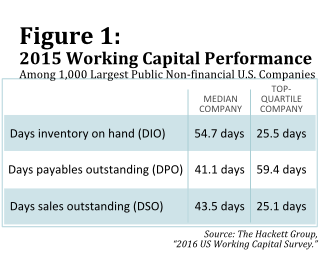

T&R: Clearly some companies are getting it right. Your 2016 Working Capital Survey divides respondents into quartiles based on their performance in DSO, DPO, and DIO. And the difference between the top-quartile companies and the median company is pretty remarkable, for each of those metrics. In terms of inventory management, the median company keeps inventory on hand for almost twice as long as the top-quartile company. [See Figure 1, below.]

CB: Yes, the top quartile of organizations are doing a lot better than the median company in each area of working capital performance. Although even among companies that are currently focused on improving working capital, many struggle with sustainability. A lot of organizations run these projects as one-off initiatives, and they lose momentum over time. Among companies that have improved their cash conversion cycle in recent years, only 10 percent have seen improvements every year for the past three years. Only 2 percent have improved every year for the past five years. And fewer than 1 percent of the companies we looked at have improved working capital every year for the past seven years.

Companies really struggle to make their quick wins sustainable by embedding working capital performance improvement practices so that they become normal ways of working for employees.

T&R: So, what should an organization do to make a working capital management project sustainable?

CB: The company needs to look at how to actually change normal ways of working. Often we'll see organizations put in a quarter-end or year-end initiative to try to improve collections, cut back inventories, or extend payment terms. But the project will be very short-term.

Two of the common things we look at in trying to make these types of projects more sustainable are: First, what are the targets; what are we measuring in the business? And second, who is accountable—not in terms of apportioning blame, but in terms of who is responsible for performing the root-cause analysis to understand trends and then find corrective actions? That's a key thing we see in projects that aren't sustainable—a lack of accountability.

Two of the common things we look at in trying to make these types of projects more sustainable are: First, what are the targets; what are we measuring in the business? And second, who is accountable—not in terms of apportioning blame, but in terms of who is responsible for performing the root-cause analysis to understand trends and then find corrective actions? That's a key thing we see in projects that aren't sustainable—a lack of accountability.

So my key recommendation is to move away from quarter-end or year-end targets, to ongoing rolling targets with very clear owners and very clear reporting.

T&R: Another challenge I see with sustainability of a working capital initiative is that one company's payable is another company's receivable. So improvement in one company probably corresponds to deterioration in the other. You found that, in the largest U.S. companies, receivables performance has stayed pretty flat, while payables performance has improved. Does this mean they're squeezing smaller companies, or where else in the supply chain does that improvement in payables show up?

CB: I think it's a couple of things. You're right, there might be an element of squeezing smaller companies. I also think supply chain financing could be having an effect there, and we are certainly seeing an increase in supply chain financing. There are more and more providers coming into the market, and it's something our clients are increasingly asking about.

T&R: That makes sense. What about debt? The debt load for companies in your study increased by almost 10 percent last year, and has more than doubled since 2008. Do you see a connection between increasing corporate debt and a lack of improvement in working capital management?

CB: We do. Among the 1,000 companies we looked at, 432 have increased their debt levels by more than 100 percent since 2008. Over the same period, these companies' cash conversion cycle also increased—by 332 percent on average. In contrast, among companies that paid down their debt, the cash conversion cycle fell by an average of 40 percent.

CB: We do. Among the 1,000 companies we looked at, 432 have increased their debt levels by more than 100 percent since 2008. Over the same period, these companies' cash conversion cycle also increased—by 332 percent on average. In contrast, among companies that paid down their debt, the cash conversion cycle fell by an average of 40 percent.

T&R: Those are pretty striking numbers. With interest rates so low and debt so cheap, though, how can a treasury or finance manager convince senior management that a working capital performance initiative is worth the effort?

CB: The first step is to explore any opportunities that could come from improving working capital. How much capital could you free up, and what could that capital be used for? It's easy to say, 'The cost of cash is cheap, so why worry?' But when executives start to see hundreds of millions of dollars of opportunity, they get ideas of what that could be used for. So the first step is to get a feel for the size of the opportunity and the advantage it offers the business.

The next step would be to look at what other benefits could come from the project. Often, working capital management initiatives are not exclusively about working capital. Companies can achieve additional process improvements, and possibly also cost savings, depending on which initiatives they're putting in place.

T&R: Do you anticipate that working capital management will become more front-and-center for companies once interest rates are rising?

CB: We do. We are anticipating that as interest rates go up, there will be more of a discussion internally around ways to improve operations and to release cash from operations before looking for funding elsewhere. As the cost of cash increases, companies will become a little less complacent and will look for those opportunities internally.

CB: We do. We are anticipating that as interest rates go up, there will be more of a discussion internally around ways to improve operations and to release cash from operations before looking for funding elsewhere. As the cost of cash increases, companies will become a little less complacent and will look for those opportunities internally.

Many companies have become very, very reliant on debt, and in the long term that is not sustainable. Now is the time for companies to be getting ahead in terms of their working capital management practices. They should be getting ahead of it now, anticipating changes in the future and looking to improve their working capital position while they still have time to do it proactively rather than reactively.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.