High-profile court cases that pit participants indefined-contribution retirement plans against the plans' sponsorshave dominated news headlines lately. Participants in some planshave sued, claiming their plan's sponsor violated its fiduciaryduty by offering investment options that carry excessive fees. Ifyou sponsor a defined-contribution plan, the implications of caseslike Tibble v. Edison and Tussey v. ABB might have you feeling a bit ofpressure. You wouldn't be alone.

High-profile court cases that pit participants indefined-contribution retirement plans against the plans' sponsorshave dominated news headlines lately. Participants in some planshave sued, claiming their plan's sponsor violated its fiduciaryduty by offering investment options that carry excessive fees. Ifyou sponsor a defined-contribution plan, the implications of caseslike Tibble v. Edison and Tussey v. ABB might have you feeling a bit ofpressure. You wouldn't be alone.

Heightened scrutiny on defined-contribution plan fees has ledsome sponsors to decide to move their plan investments tolower-cost passive options. The rationale is that if courts havedecided high fees are bad, then funds with the lowest possibleoverall cost must be good. Unfortunately, things are not thatsimple.

|At the core of several court cases is ERISA Section 404(a)(1), known as the “prudent investorstandard.” It specifies that a plan fiduciary has a duty to actsolely in the interests of participants and beneficiaries, defrayreasonable expenses of administering the plan, and act in the samemanner that a prudent person would in the same circumstances. Theseprovisions do not suggest that the plan's fees must be the loweston an absolute basis, just that they must be reasonable.

|Further complicating the question of excessive fees, courts havefound that a fiduciary is failing to act solely in the bestinterests of plan participants and beneficiaries if the fiduciaryacts out of concern for its own liability. In Tatum v. RJR, the court found that the decision todivest the RJ Reynolds pension plan of Nabisco stock was for thepurpose of reducing the liability of the company and thus aviolation of ERISA.

|Picking an all-passive lineup in order to avoid lawsuits isclearly a decision that is not focused solely on what's in theparticipants' best interests. So, before making strategic changesto their defined-contribution plan menu, plan sponsors need to takeinto consideration the lessons offered by several recent courtdecisions.

|What Can You Learn from the Litigation?

In several recent cases, the courts have clarified thatfiduciaries don't have an obligation to simply select the cheapestoption.

|In Tibble v. Edison, the underlying question waswhether fiduciaries of the plan had chosen the proper share classfor certain mutual funds offered. The Supreme Court ruled in favorof plan participants who claimed Edison International violated itsfiduciary duty by offering participants mutual funds that were moreexpensive than other materially equivalent funds available on themarket. The main lesson to be learned from this ruling is that afiduciary has an obligation to monitor plan investments and fees onan ongoing basis, even after a fund is selected.

| InHeckerv. Deere, the court ruled that ERISA does notrequire fiduciaries to scour the market to find and offer thecheapest possible fund (which might create other problems). Whatplan sponsors must do is make sure the options they offer arereasonable. And the recently filed Bell v. Anthem andWhite v. Chevron cases show that even a sponsor whichprimarily uses index funds is not immune from getting sued over theissue of reasonable fees.

InHeckerv. Deere, the court ruled that ERISA does notrequire fiduciaries to scour the market to find and offer thecheapest possible fund (which might create other problems). Whatplan sponsors must do is make sure the options they offer arereasonable. And the recently filed Bell v. Anthem andWhite v. Chevron cases show that even a sponsor whichprimarily uses index funds is not immune from getting sued over theissue of reasonable fees.

These cases demonstrate that defined-contribution planfiduciaries have an obligation under the law to make prudent andreasoned decisions in the best interests of the plan's participantsbased on the evaluation and subsequent monitoring of funds. Thismeans that every plan sponsor needs a documented, deliberativeprocess both for selecting managers and administrators that theplan sponsor thinks are best for the plan, and for making sure allfees are reasonable for the level of service provided, includingfees paid separately and through revenue sharing.

||Some plan sponsors are addressing this fiduciary duty either byhiring consultants who can advise on the best investment options,or by outsourcing investment management functions to an ERISAsection 3(38) investment manager—one with the power to manage theselection, monitoring, and (if necessary) replacement of the plan'sfund managers.

|When a plan sponsor designates an outsourcer to carry outinvestment responsibilities, the outsourcer becomes liable forthose activities under ERISA. The sponsor retains liability for theprudent selection and ongoing monitoring of the outsourcer.

|Going Passive: Investment-Related Issues You Need toConsider

Some sponsors pick passive investments, which make investmentchoices based on an external index and generally seek to minimizeinvesting fees. Plan sponsors may believe that passive investmentsreduce their fiduciary risk and due diligence obligations. But thetruth is that “going passive” involves several active decisions,and meaningful due diligence requirements remain around each ofthese decisions.

|Sponsors need to have documented processes showing that theyhave reviewed and understand:

||

The index provider'sorganization. Who is providing index data forthe fund(s) you are offering to defined-contribution planparticipants? Participants invest with money managers (not indexproviders), but the plan sponsor still needs to make sure the indexprovider comes from a strong organization that has experience andexpertise in creating indexes.

|Plan sponsors can start by asking fund managers about theirinvestment rationale for the index provider, including how theprovider compares with others in terms of fees and exposures. It isalso important to understand the research capabilities, technologyinfrastructure, and history of the index provider. If the fundmanager does not provide satisfactory answers, plan sponsors cantake their questions directly to the index provider.

|

The index provider's methodology. For passive options, the investment experience is driven,almost completely, by the index provider's methodology. Therefore,it is crucial for the defined-contribution plan sponsor selectingan index fund to understand the index's underlying methodology.This includes verifying that the index exposures match the plansponsor's desired exposures.

|There are several different methodologies across indexproviders, which can lead to different types of exposures. Forexample, the calendar-year returns of the S&P 500 Index differfrom those of the FTSE Russell 1000 Index, despite both being goodproxies for U.S. large-cap equity. Between 1998 and 2014, thedifferential return was almost 300 basis points in some calendaryears. In fixed income, the Barclays U.S. Aggregate Bond Index hasincreased its allocation to low-yielding government securities overthe last five years. If interest rates increase, this exposurecould leave participants unguarded.

|

Quality of implementation by the passive-fundmanager. More goes into managing a passive fundthan you might think. There are rules about sampling (or not),rebalancing, pricing, and market timing. The way these rules aredesigned and implemented can change how closely the fund tracks anindex. That is why tracking “error,” in addition to cost andperformance history, is a key indicator for evaluating passiveinvestments.

|One source of tracking error may be the index manager'sreplication method. Funds do not necessarily purchase everysecurity in an index. They may choose a sample designed torepresent the whole instead. Other areas that can affect trackingand performance are the sophistication of the quantitative toolsthe fund uses, its trading practices, and the amount and timing ofcross-trading.

|As with the management of any investment option, plan sponsorsalso need to be comfortable with the team responsible for managingimplementation at the index fund.

||

The feasibility and costs of replicating theindex. Some indexes can be replicated easily;these are typically indexes that track asset classes which arehighly liquid and publicly traded. But some less-liquid markets,such as high-yield bonds, may present substantial management andimplementation costs. They may also present a high likelihood oftracking error because a fund manager is unlikely to be able toperfectly match the fund's investments to the index portfolio. Andsome markets, such as private real estate, can't be replicated inan index at all.

Plan sponsors that opt for an all-passive fund lineup should beaware that they may be preventing plan participants from accessingcertain asset classes within the plan, because those asset classeslack quality index funds. Returning to the decision in Heckerv. Deere, the lesson for plan sponsors is tofocus on the value of fund options, not just fees. Asset classesthat are more efficient, with higher analyst coverage, may makegood candidates for passive management. Less-efficient classes withlower analyst coverage, such as small cap equities, emergingmarkets equities, and real assets, can be attractive for activemanagement.

|Whatever the final decision on passive and active options, plansponsors need to base their choice on a belief about what is bestfor their participants and document the process and rationale forarriving at their decision.

|

The fees charged by the passive-fundprovider. Several passive-fund managers providevery similar products yet have different fee structures. A keyelement of the defined-contribution plan sponsor's fiduciary dutyis to ensure that plan participants are paying the lowest feespossible, given the size of assets in the plan. This was raised inthe recent White v. Chevron lawsuit.

|Two important questions to ask are the following: Does the fundyou selected for participants have the cheapest share classavailable to your plan? How do mutual funds compare with collectiveinvestment trusts?

|A plan sponsor is responsible for the ongoing review of fees andcosts, and while the courts have not defined exactly what “ongoing”means, it makes sense to review a plan at least annually.

|

Might active-management opportunities be moreprudent? While passive management is a goodstarting point, a prudent plan sponsor should also consider activemanagement—especially in situations involving asset classes thatare difficult to passively manage in a cost-effective manner.Asking questions like this in an annual review can help demonstratea “conscientious and diligent process” for reaching prudentinvesting decisions.

|Keep in mind that low fees don't necessarily translate intobetter outcomes for participants. For example, in aninstitutionally run target-date fund that mixes active and passiveinvestments, it would be reasonable to expect an extra 50 basispoints per year in performance, net of fees, compared with passivecounterparts. Russell Investments' analysis finds that thisdifference could generate up to seven years of additional spendingin retirement for a participant who saved and invested over a40-year working career.

Additional Review for Passive Target-DateFunds

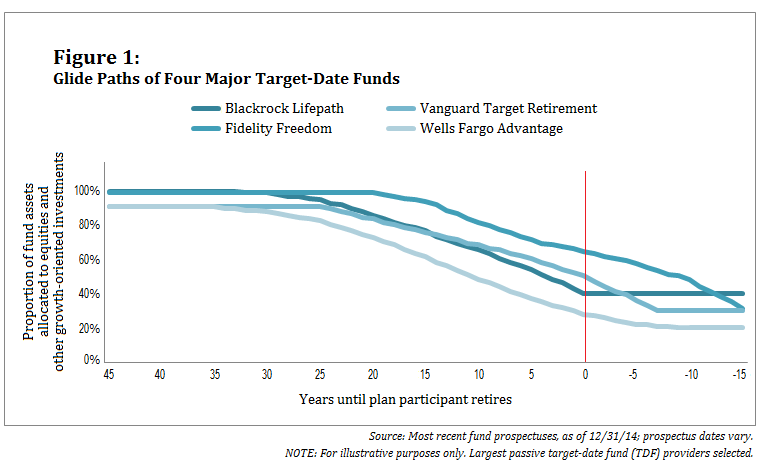

Glide path methodology. Themanagers of a target-date fund (TDF) decide when and where toinvest the fund's assets. These decisions are active, even if theychoose all passive investments that individually track relevantindexes, such as the S&P 500 Index and Barclays U.S. AggregateBond Index.

|A TDF's “glide path” shows how it changes the mix ofgrowth-oriented and income-oriented investments as the fundapproaches the target retirement date. The glide paths of fourmajor “passive” target-date providers show clearly that severalactive decisions are embedded in the design of each TDF (see Figure1, below). These include when the glide path starts to slope—i.e.,when the fund starts to allocate less of the portfolio togrowth-oriented investments—as well as the steepness of the slope,how much risk the plan participant is taking at retirement, andwhether the glide path remains flat in retirement. All of thesedecisions influence participants' potential outcomes andexperiences.

|

Asset allocation. It's importantto understand which asset classes the TDF managers choose and whenthey make changes to these allocations. If a passive TDF manageromits certain asset classes that cannot be cost-effectively managedpassively, that exclusion is an active decision that may increasevolatility or reduce return expectations.

| Theplan sponsor also needs to consider how the TDF manager makesallocations across the asset classes. For example, how much of theequity allocation is in U.S. securities? Geographic diversificationis particularly important for TDFs because they are designed tomanage all of a plan participant's assets. A concentratedallocation to any particular asset class or region could lead tohigher portfolio volatility, while a more globally focusedallocation could potentially lead to a smoother ride, which isimportant to many participants saving for retirement.

Theplan sponsor also needs to consider how the TDF manager makesallocations across the asset classes. For example, how much of theequity allocation is in U.S. securities? Geographic diversificationis particularly important for TDFs because they are designed tomanage all of a plan participant's assets. A concentratedallocation to any particular asset class or region could lead tohigher portfolio volatility, while a more globally focusedallocation could potentially lead to a smoother ride, which isimportant to many participants saving for retirement.

Sponsors might consider a TDF series that uses actively managedfunds for asset classes with the greatest potential for addingvalue going forward, but also uses passively managed funds forefficient asset classes like large-cap U.S. equities. This approachenables the plan sponsor to control overall fund costs whilebringing participants a diversified combination of potential returnsources—including some asset classes (e.g., real assets) that aretypically more expensive.

|Making the Best-Informed Decisions for PlanParticipants

Defined-contribution plan sponsors have a big responsibility.They should make decisions based exclusively on which investmentchoices they think are best for their plan's participants, whileensuring compliance with legal and regulatory requirements. Inparticular, I encourage plan sponsors to:

- focus on each fund's value, not just the level of fees;

- avoid taking what seems to be the path of leastresistance—i.e., going all-passive in the belief that doing soprovides some fiduciary protection;

- document the rationale behind each decision; and

- get expert advice and/or outsource to a trusted provider ifyour organization doesn't have the right investment expertisein-house.

Ultimately, making decisions that help plan participants reachtheir retirement-income goals is in the best interests of both theparticipants and the plan sponsor. Doing so may also help keep yourorganization's name out of the headlines.

|————————————

| Josh Cohen is managing director for definedcontribution with Russell Investments, responsible for theleadership, strategic direction, and growth of the U.S. definedcontribution business. He is an executive committee member andchair of the retirement research board of the DefinedContribution Institutional Investment Association (DCIIA), a memberof the Board of Trustees of the Employee Benefit Research Institute(EBRI), and recently served on the Department of Labor's ERISAAdvisory Council.

Josh Cohen is managing director for definedcontribution with Russell Investments, responsible for theleadership, strategic direction, and growth of the U.S. definedcontribution business. He is an executive committee member andchair of the retirement research board of the DefinedContribution Institutional Investment Association (DCIIA), a memberof the Board of Trustees of the Employee Benefit Research Institute(EBRI), and recently served on the Department of Labor's ERISAAdvisory Council.

|

The opinions expressed in this material are notnecessarily those held by Russell Investments, its affiliates orsubsidiaries. While all material is deemed to be reliable, accuracyand completeness cannot be guaranteed. The information, analysis,and opinions expressed herein are for general information only andare not intended to provide specific advice or recommendations forany individual or entity.

|AI-24295

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

")