Credit risk is a crucial financial consideration forcompanies of all shapes and sizes. Organizations aren't going tothrive if they can't rely on customers to pay what they owe, can'tdepend on their supply chain to move materials and components in atimely manner, or fear for the stability of their bankingpartners.

Credit risk is a crucial financial consideration forcompanies of all shapes and sizes. Organizations aren't going tothrive if they can't rely on customers to pay what they owe, can'tdepend on their supply chain to move materials and components in atimely manner, or fear for the stability of their bankingpartners.

It's a timeless topic, but with many new wrinkles, as today'stechnology tools make a world of information and powerful analyticscapabilities available to credit managers. To learn more about howcompanies today are managing the myriad credit risks they face—andto identify opportunities for improvement—Treasury &Risk undertook the “2016 Credit Risk Management Survey,”sponsored by Moody'sAnalytics.

|Conducted this summer, the survey received responses from 110professionals who work in treasury (43 percent), finance (40percent), risk management (10 percent), or line-of businessmanagement (6 percent). They hail from businesses of all sizes,across a wide swath of industries.

|What we found is that counterparty credit risk is, indeed,top-of-mind for treasury and finance teams. More survey respondentssaid they are very concerned about currency volatility orabout third-party payments fraud, but credit risk is not farbehind. Nearly two-thirds of respondents (63 percent) said they areeither concerned or very concerned about thecredit risk posed by their organization's trading partners and/orfinancial counterparties. That makes credit risk a more pressingconcern than interest rate risks (about which 38 percent areconcerned or very concerned), commodity pricevolatility (39 percent), or payments fraud perpetrated by employees(28 percent).

|Drivers of Credit-Risk Concerns

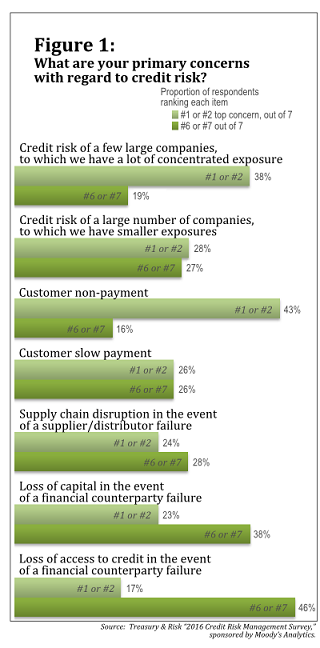

A major driver of corporate anxiety about credit risk is thatmany of the surveyed companies have large exposures to a fewspecific businesses. When asked to rank seven different sources ofcredit risk, in order, on the degree to which they're causingconcern, more than a quarter (26 percent) of respondents chosecredit risk of a few large companies, to which we have a lot ofconcentrated exposure as their number-one issue. Another 31percent rated this option second or third. Just 10 percent ofrespondents rated the alternative scenario, credit risk of alarge number of companies, to which we have smaller exposures,as their top concern. Most of those do business in eitherretail/distribution or the technology sector.

|Along the same lines, the survey shows that more treasury andfinance professionals are losing sleep over customers failing topay at all than over customers paying slowly. Forty-three percentof respondents—many in retail/distribution, telecommunications, andtransportation/logistics—rated customer non-payment amongtheir top two concerns, while only 26 percent gave the same ratingto customer slow payment. (See Figure 1.)

| Corporate treasury and finance professionals are afraidthat a single large customer will fail to pay. They worry thatproblems at a crucial supplier or distributor might wreak havocwith their supply chain. And they fret that if a financialcounterparty failed, they might lose capital or lose access tocredit. These concerns are justifiable. Any of these events couldhave significant ramifications for the bottom line of companies upand down the supply chain.

Corporate treasury and finance professionals are afraidthat a single large customer will fail to pay. They worry thatproblems at a crucial supplier or distributor might wreak havocwith their supply chain. And they fret that if a financialcounterparty failed, they might lose capital or lose access tocredit. These concerns are justifiable. Any of these events couldhave significant ramifications for the bottom line of companies upand down the supply chain.

What, then, are survey respondents doing to mitigate the creditrisk they face?

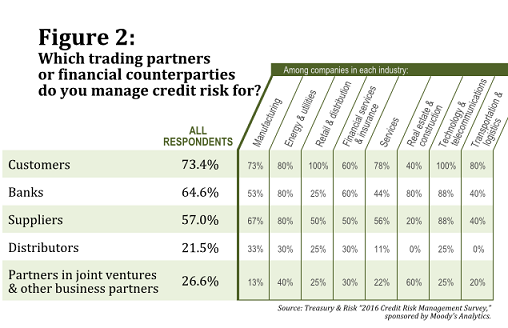

|To start, almost three-quarters of companies represented in thesurvey (73 percent) are managing the credit risk posed by theircustomers. This is good news, considering that 38 percentidentified either customer slow payment or customernon-payment as their single most important credit-riskconcern. Customer credit risk management is common across allindustry sectors, although businesses in financial services andreal estate/construction are somewhat less focused on mitigatingexposures to customer credit issues than are companies in otherindustries. (See Figure 2 on page 2.)

|Our survey also indicates that the vast majority of companies inthe energy, real estate/construction, technology, and telecomsectors proactively manage the credit risk posed by their banks.This makes sense, since respondents from these industries alsoshowed the most concern about the chance that one of theirfinancial counterparties might fail. Half of telecom companies, and40 percent of businesses in transportation/logistics, rankedloss of access to credit in the event of a financialcounterparty failure as either first or second on their listof primary concerns. In addition, almost a third (29 percent) oftech companies, and 20 percent of those in the energy industry,gave first or second billing to loss of capital in the event ofa financial counterparty failure.

||Companies in the manufacturing, energy, and tech sectors aremost likely to actively manage the credit risk of their suppliers.This gibes with the fact that 40 percent of respondents who work inmanufacturing, and 30 percent in the energy industry, ratedsupply chain disruption in the event of a supplier/distributorfailure as one of their top two concerns. Organizations in theretail sector are a bit more likely than the typical company tomanage credit risk for their distributors, but a bit less likelythan average to do so for their suppliers. Among companies that domanage distributors' credit risk, almost all (87 percent) alsoproactively manage suppliers' credit risk.

|Finally, a little over one-fourth of all respondents (27percent) said their organization manages the credit risk posed byits partners in joint ventures and other business partners. Thecompanies most likely to do so are those that are most concernedabout loss of capital in the event of a financial counterpartyfailure, as well as those most worried about customer slowpayment and about the credit risk of a large number ofcompanies, to which we have smaller exposures.

|Tools and Techniques for Credit RiskManagement

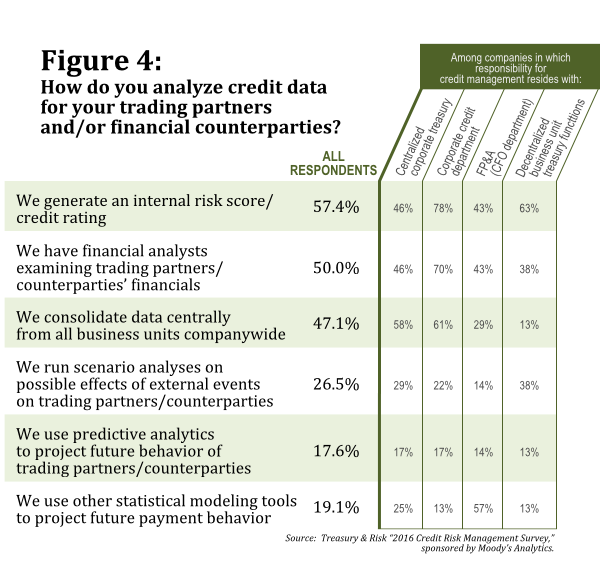

Participants in the Treasury & Risk survey use avariety of tools and techniques to analyze the credit risk of theirtrading partners and counterparties. Almost half consolidate datacentrally from all business units companywide. Exactly half havefinancial analysts examine trading partners' or counterparties'financials, and even more generate an internal risk score or creditrating. Many survey respondents also run scenario analyses on thepossible effects of external events on their trading partners orcounterparties; use predictive analytics to project the futurebehavior of trading partners or counterparties; and/or use otherstatistical modeling tools to project future payment behavior. (SeeFigure 4, on page 3.)

| Although nearly two-thirds of respondents (63 percent)said their company uses an external model from a rating agency aspart of its credit-data analysis, a quarter (26 percent) use amarket-based external model, and 12 percent use aneconometrics-based external model. Just over half (51 percent) usean internal model driven by expert judgment, and 45 percent use aninternal quantitative model.

Although nearly two-thirds of respondents (63 percent)said their company uses an external model from a rating agency aspart of its credit-data analysis, a quarter (26 percent) use amarket-based external model, and 12 percent use aneconometrics-based external model. Just over half (51 percent) usean internal model driven by expert judgment, and 45 percent use aninternal quantitative model.

Businesses that use an internal model are more than twice aslikely to consolidate data centrally, and are nearly four times aslikely to generate internal credit ratings, as are companies thatuse either a market-based or econometric-based external model.Likewise, companies that use internal models are more likely to usescenario analysis, and nearly four times as likely to usepredictive analytics.

|The companies represented in our survey use data from fairlypredictable sources to populate these models. Three-quarters usecredit reports from credit bureaus. Seven in 10 use their tradingpartners' or financial counterparties' SEC filings and financialstatements. And nearly that many (69 percent) include in theircredit analyses their organization's internal data on transactionhistory, such as a customer's payment history with the companydoing the credit analysis.

|Sixty-one percent of survey respondents said their company usescredit risk scores developed by a third party to estimate theprobability of default. More than half (51 percent) of representedorganizations' credit-analysis processes incorporate bankreferences; 38 percent include industry or geographic data from athird party; and 32 percent use external data on the tradingpartner's or counterparty's transaction history. Severalrespondents also wrote in additional information sources that theirorganization uses, including insurance companies, industry creditassociations, and unaudited financials for the data underlyingcredit-related decisions.

|

Where Credit Management Authority Resides

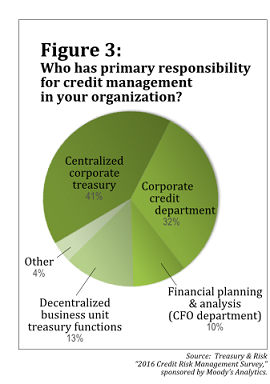

One of the largest determinants of the credit risk managementtools and techniques that a particular company uses is which groupwithin the organization has responsibility for corporate creditmanagement. The most common structure described in the Treasury& Risk survey gives credit management to a centralizedcorporate treasury function. That's how 41 percent of allorganizations are structured, including 53 percent of manufacturingcompanies and 50 percent of businesses in the retail/distributionsector. The companies that operate in the largest number ofcountries are also the most likely to use a centralized treasuryfunction for credit management—including 45 percent oforganizations doing business in 10 or more countries, and more thantwo-thirds of companies operating in five to nine countries.

| Overall, the second most popular location forcredit-management responsibility is within a separate corporatecredit department. About a third of survey respondents have acorporate credit function. This option has the most traction amongthe largest organizations, as well as in thetransportation/logistics sector (80 percent) and among financialservices firms (40 percent).

Overall, the second most popular location forcredit-management responsibility is within a separate corporatecredit department. About a third of survey respondents have acorporate credit function. This option has the most traction amongthe largest organizations, as well as in thetransportation/logistics sector (80 percent) and among financialservices firms (40 percent).

In 10 percent of all companies—including 20 percent of thosedoing business in only one country—credit management resides in acorporate financial planning and analysis (FP&A) function thatfalls under the purview of the corporate CFO. In contrast, 13percent of survey respondents said their organization gives creditmanagement responsibility to decentralized treasury functionswithin the business units. Additionally, several survey respondentsreported that their companies use other solutions, includingoutsourcing credit management and placing credit management in anenterprise risk management (ERM) function.

|The companies that have a corporate credit department are themost likely to generate an internal risk/credit score (78 percent,vs. 50 percent of other businesses) and to have financial analystsexamining the financials of organizations they do business with (70percent, vs. 43 percent of other companies). Corporate creditfunctions are also most likely to consolidate all credit data fromacross the organization (61 percent), followed closely by companiesin which a centralized treasury team handles credit management (58percent). Just 22 percent of other companies consolidate creditdata from all their business units. (See Figure 4, below.)

|Interestingly, the companies that are most likely to usescenario analysis to project the effects of external events ontheir credit counterparties are those in which credit management ishandled by decentralized business units, followed by companies inwhich corporate treasury handles credit management. Organizationsin which credit management resides with FP&A are not any morelikely to engage in predictive analytics—and are actually lesslikely to run scenario analyses—than are other businesses. However,FP&A functions are more than twice as likely to use otherstatistical modeling tools to project future payment behavior.

|While not statistically valid, it's worth noting that the oneorganization represented in our survey that outsources creditmanagement uses all of these techniques.

|

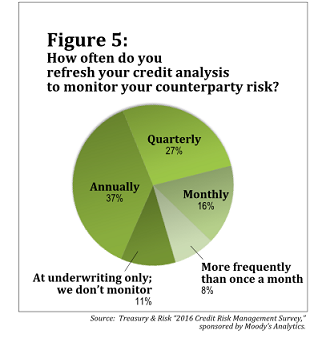

Credit Risk Analysis Refresh Cycle

Across all companies represented in the Treasury &Risk survey, 16 percent refresh their counterparty creditanalysis once a month, and 8 percent refresh even more frequently.Businesses that consolidate all their data centrally, and thosethat generate an internal risk rating, are most likely to refreshmore than once a month. Two in five companies that use predictiveanalytics (42 percent) refresh their analyses monthly, comparedwith 13 percent of companies that don't use predictive analytics.In contrast, 37 percent of all survey participants said theircompany refreshes credit analyses only once a year, and 11 percentperform a credit analysis only once for each organization; they donot monitor on an ongoing basis at all.

Across all companies represented in the Treasury &Risk survey, 16 percent refresh their counterparty creditanalysis once a month, and 8 percent refresh even more frequently.Businesses that consolidate all their data centrally, and thosethat generate an internal risk rating, are most likely to refreshmore than once a month. Two in five companies that use predictiveanalytics (42 percent) refresh their analyses monthly, comparedwith 13 percent of companies that don't use predictive analytics.In contrast, 37 percent of all survey participants said theircompany refreshes credit analyses only once a year, and 11 percentperform a credit analysis only once for each organization; they donot monitor on an ongoing basis at all.

The majority of companies that have a corporate credit function(57 percent) update credit analyses on an annual basis; only 17percent of these organizations refresh monthly or more frequently.Annually is also the most common refresh cycle for organizations inwhich decentralized business unit treasury teams handle creditmanagement (33 percent of these companies).

|But in companies where centralized treasury has responsibilityfor them, credit analyses are most likely to be refreshed quarterly(35 percent), monthly (14 percent), or more frequently (10percent). And in companies where FP&A manages counterpartycredit, 72 percent update their credit analyses quarterly or moreoften.

|What Is Limiting Credit ManagementEffectiveness?

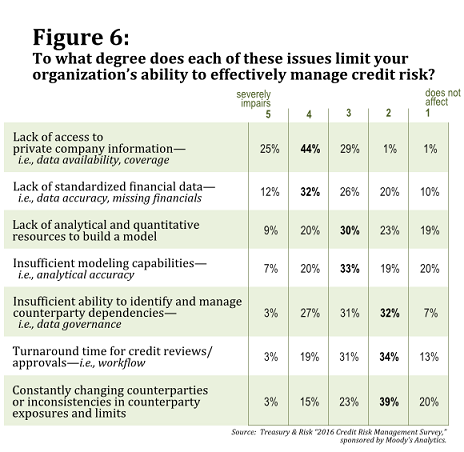

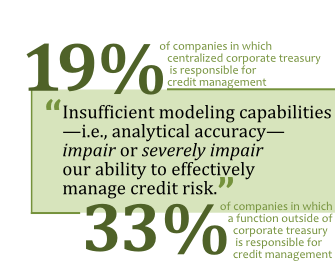

The survey also asked respondents to rank the degree to whichdifferent issues limit their organization's ability to effectivelymanage credit risk. On a scale of 1 to 5, where 1 means“does not affect” and 5 means “severely impairs,” close toa third of respondents (28 percent) rated insufficient modelingcapabilities—i.e., analytical accuracy either 4 or5. These problems with analytical accuracy areegalitarian. More than any of the other challenges we identified,insufficient modeling capabilities cuts evenly across allindustries and all degrees of complexity in organizationalstructure (see Figure 6, below).

|That isn't to say all companies struggle equally with allaspects of data analysis. Twenty-nine percent of respondents ratedlack of analytical and quantitative resources to build amodel as either 4 or 5 on the scale oflimiting risk management effectiveness. But analytical andquantitative resources are especially problematic for organizationsthat proactively manage the credit risk they face from their banks(31 percent of these respondents rated lack of analytical andquantitative resources to build a model either 4 or5) and/or business partners (33 percent). And amongorganizations that are gravely concerned about losing access tocredit in the event of a financial counterparty failure, 55 percentgave either a 4 or 5 to lack of analyticaland quantitative resources to build a model.

|Even more challenging for the organizations represented in thesurvey is a lack of standardized financial data—i.e., dataaccuracy, missing financials. Among all respondents, 44percent assigned this issue a score of 4 or 5. Asmight be expected, standardization of data is most problematic forcompanies that consolidate data centrally from all business unitscompanywide; 74 percent of these organizations gave high-impactratings to lack of standardized financial data, comparedwith only 44 percent of companies that do not consolidate datacentrally. This challenge also becomes more problematic the morecomplex the organization becomes. Sixty percent of respondentswhose company operates in 10 or more countries cited lack ofstandardized financial data as severely impairing theirability to effectively manage credit risk.

|

Another data issue, insufficient ability to identify andmanage counterparty dependencies—i.e., data governance,received a score of 4 or 5 on thelimiting-effectiveness scale from 29 percent of respondents,although very few (3 percent) rated it “5 = severely impairs.” Datagovernance is most problematic for companies that use statisticalmodeling tools to project future payment behavior, and forcompanies that refresh their credit analyses on a monthly basis; 40percent and 45 percent of these businesses, respectively, ratedinsufficient ability to identify and manage counterpartydependencies at 4 or 5.

|The issue that is problematic for the largest proportion ofsurvey respondents is lack of access to private companyinformation—i.e., data availability, coverage. A quarter ofrespondents rated this problem a 5, and more thantwo-thirds (68 percent) gave it either a 4 or 5.Meanwhile, less than 3 percent rated it 1 or 2.Private company information is most problematic for manufacturing(79 percent rate it 4 or 5) andtransportation/logistics companies (75 percent). It's aparticularly notable challenge for all organizations in whichcustomer slow payment is a leading concern; 80 percent ofthese respondents ranked lack of access to private companyinformation either 4 or 5.

| The final two issues pose the least challenge, althougheach was given a score of 5 by 3 percent of surveyrespondents. Turnaround time for credit reviews/approvals—i.e.,workflow is considered a serious barrier to efficiency (rated4 or 5) by 22 percent of all respondents. Itsimpact is especially acute in the financial services and energyindustries, while it has almost no impact on respondents in theservices and manufacturing sectors.

The final two issues pose the least challenge, althougheach was given a score of 5 by 3 percent of surveyrespondents. Turnaround time for credit reviews/approvals—i.e.,workflow is considered a serious barrier to efficiency (rated4 or 5) by 22 percent of all respondents. Itsimpact is especially acute in the financial services and energyindustries, while it has almost no impact on respondents in theservices and manufacturing sectors.

Constantly changing counterparties or inconsistencies incounterparty exposures and limits received a score of4 or 5 from 17 percent of respondents overall.Among companies that do not consolidate data centrally, 22 percentgave changing/inconsistent counterparty information top billing,compared with only 13 percent of companies that do centralizecredit information. Not surprisingly, changing counterpartyinformation is a top issue among 33 percent of companies thatperform credit analyses only at underwriting, without continuing tomonitor on an ongoing basis.

|Credit Risk Management Best Practices

What can companies learn from this research about how to improvetheir credit risk management processes? An obvious place to startis by reconsidering the model their data analysts use. Surveyrespondents from companies that rely on a market-based externalmodel were more likely to select “severely impairs” to describe theimpact on their credit risk management of every single challengethey were asked about. In contrast, companies that use internalmodels are less likely to be impacted by the challenges identifiedin the survey.

|In addition, companies should look hard at consolidatingcorporate credit information in a central location. Althoughrespondents who said their company consolidate[s] datacentrally from all business units companywide are much morelikely to consider lack of standardized financial data aserious problem, they are less likely to face the other challengesidentified in the survey—in many cases by a differential of morethan 10 percentage points. For example, a lack of analyticaland quantitative resources to build a model inhibits creditmanagement success (rating of 4 or 5) in 34percent of companies that do not consolidate credit data centrally,compared with 19 percent of companies that do. Similarly,respondents whose companies fail to centralize credit data are morelikely to feel their ability to identify and managecounterparty dependencies [is] insufficient (33 percent, vs.25 percent of companies that do centralize data). They are alsomore likely to feel that constantly changing counterparties orinconsistencies in counterparty exposures and limits have aserious impact on their credit risk management capabilities (22percent, vs. 13 percent of companies that centralize data).

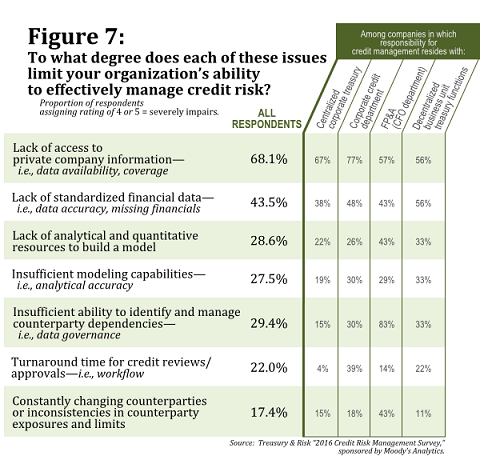

||As they consider consolidating credit data, companies looking toimprove their credit management should also think aboutcentralizing those responsibilities within the corporate treasuryfunction. Across almost every issue addressed in the Treasury& Risk survey, respondents in companies where credit riskis managed outside of corporate treasury were more likely toidentify the problem as severely impairing their ability to managecredit risk. (See Figure 7.)

|This discrepancy is particularly acute in terms of workflow anddata governance. In companies where corporate treasury handlescredit management, 15 percent gave insufficient ability toidentify and manage counterparty dependencies a rating of4 or 5—so problems managing counterpartydependencies either impair or severely impair credit riskmanagement among 15 percent of these companies—compared with 38percent of companies in which a different function manages creditrisk.

|

Finally, companies that want to bulk up their ability tomitigate the various credit risks they face should reconsider thefrequency with which they refresh their analyses. Among surveyrespondents whose businesses update credit analyses only annually,33 percent believe their modeling capabilities—and so theiranalytical accuracy—is insufficient. That number drops to 22percent among those that refresh credit analyses quarterly, and tojust 9 percent among those who refresh monthly.

|There is no silver bullet for credit risk management, nosolution that optimally fits every diverse business's management ofthe risks presented by each of its counterparties. But our researchindicates strong correlations between organizations' ability tominimize the impact of specific problems on credit managementeffectiveness, their consolidation of companywide credit data, andtheir centralization of credit management activities withincorporate treasury. Organizations looking to make better creditdecisions should give these correlations careful consideration.

|——————-

|Meg Waters is the editor in chief ofTreasury & Risk.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Meg Waters

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.