Rest in peace, VIX. You're no longer the fear gauge for globalmarkets.

|The Bank for International Settlements has found a betterbarometer to capture the nervousness that starts as a slightreduction in global banks' leverage, is magnified by Europeanlenders as a dollar squeeze in Asian supply chains, andreverberates around the world as a financial tightness felt byeveryone.

|Everyone, except the Chicago Board Options Exchange's VolatilityIndex.

|VIX used to be a reliable measure of pain in financial markets.But that was before the unprecedented monetary easing that followedthe 2008 credit crisis. Nowadays, trouble is more likely to brew asan angina at the heart of Wall Street broker-dealers than erupt asa paralyzing stroke in the price of options for S&P 500 stocks.VIX might still spike eventually. But investors wanting to rushtheir portfolios to the trauma center before it's too late shouldbe watching something else entirely.

|For a crude measure of breathlessness, look no further than thebroad U.S. dollar index. For a more sophisticated view, trycross-currency basis swap spreads.

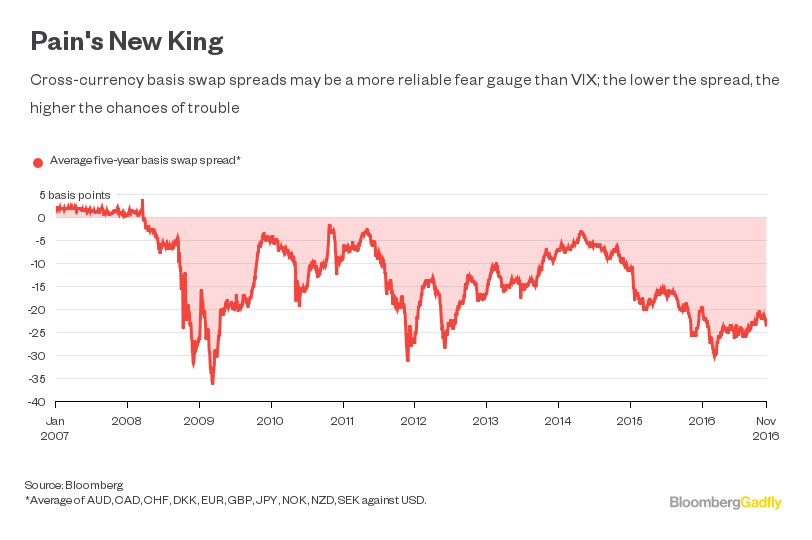

|Think of these spreads as a discount for not having the U.S.currency — and still wanting it. A negative spread on G-10currencies means that borrowing a unit of each of them and thenconverting the sum into dollars costs more than it would to borrowthe greenback outright.

|In theory, no gap should exist. Banks look for every opportunityto profit from any difference between the dollar interest rateimplied by foreign-exchange rates and the rate available in themoney market. Arbitrage would crush spreads.

|Sure enough, basis-swap spreads were negligible before 2008, butnow have turned deeply negative. To Hyun Song Shin, the Bank forInternational Settlements' head of research, they've gone frombeing “a rather esoteric corner of the foreign-exchangemarket” to “a relatively clean measure of the price ofbalance-sheet capacity of banks.” Lenders are walking away fromfree money because picking it up would require leverage, and that'sexpensive.

|If BIS researchers are right, this could explain why Asia won'tget much of an export kick by allowing local currencies to weakenagainst a resurgent dollar. Multicountry supply chains, greased bydollar loans, will grind slower as European banks pass on their owndifficulties in procuring dollars.

|

Since early 2014, the basis swap has moved in perfect lockstepwith the broad dollar: The higher the U.S. currency, the lower thespread. This gives rise to a disturbing scenario. If the 3.7% risein the trade-weighted dollar index since Donald Trump's electionvictory extends into 2017, the greenback shortage in the globalbanking system could start causing serious earnings misses,especially in Asia.

|Unless watered down or delayed, harsh Basel IV rules, expectedto be announced by early 2017, might lead to European lendersscrambling for a further 900 billion euro ($949 billion) incapital. That, too, could see them tone down corporate credit toAsia, where they're a bigger supplier of dollars than morecomfortably capitalized U.S. banks.

|Odds are that the VIX will remain a puppet on central banks'strings, and fail to give any advance warning. For investors, itmight be the time to bow to the new king of pain.

|Bloomberg News

|Copyright 2018 Bloomberg. All rightsreserved. This material may not be published, broadcast, rewritten,or redistributed.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.