When the Federal Reserve raised benchmark interest rates lastmonth, it took North Carolina lender BB&T Corp. less than anhour to announce it was passing that cost along to borrowers.Depositors, however, have yet to see the benefit.

|For many investors, such discipline means U.S. banks are aboutto feast on rising interest rates — profiting froma fatter margin between what they charge for loans and the rewardsthey offer depositors who provide the funds. Now, a small butgrowing chorus of senior executives and analysts is signaling thatresolve may fray and that shareholder optimism is too high.

|Banks are under unprecedented pressure to break ranks andcompete for deposits. Compared with past cycles, more savers areweb-savvy — able to comparison shop and transfermoney online to firms offering better deals. Money-market fundsthat suffered for years with near-zero rates are eager to lure backcustomers. And new liquidity rules encourage banks to draw morefunding from consumer deposits, pushing lenders to fight for thoseclients.

|“We've never really seen this movie before,” JPMorgan Chase& Co. chief financial officer Marianne Lake warned investors inFebruary. Lenders are “coming off of zero-bound rates in a worldwhere liquidity requirements and technology advancements willincrease the competition to get deposits and where customers aremore rate aware.”

|In a raft of recent research notes, analysts said they willlisten carefully for U.S. bank leaders to project deposit rateswhen their companies start reporting first-quarter results April13. Net income at the nation's six biggest banks —JPMorgan, Citigroup Inc., Bank of America Corp., Wells Fargo &Co., Goldman Sachs Group Inc. and Morgan Stanley —will probably climb 15% to $21.3 billion in the period, helped byimprovement in net interest margins, according to estimatescompiled by Bloomberg.

|But many analysts are underestimating the speed at which banksmay need to increase their so-called deposit beta, the share of Fedrate hikes that banks say will get passed along to depositors,according to U.S. Bancorp chief operating officer Andy Cecere, whowill become CEO of the nation's largest regional lender nextTuesday.

|Cecere, 56, laid out this argument in an interview: For years,with interest rates near zero, money market funds whittled costsand waived fees to keep clients. After the Fed raised rates inMarch by a quarter point for the third time since the financialcrisis, fees are back. That means funds can share future Fed hikesmore liberally with customers. And that changes the game forbanks.

|“Competition against waivers meant banks were holding depositbetas,” Cecere said. “Now, the competition for those consumerdeposits will increase rates.”

|Wall Street trading will also drive bank earnings in the firstquarter, with analysts estimating dealings in fixed-income,currencies and commodities probably increased at Morgan Stanley,Goldman Sachs and JPMorgan, offset by declines in revenue fromequities.

|But interest rates have been a major theme for shareholders inrecent months. Financial stocks soared after Donald Trump'sNovember election on speculation he will ease rules and pursuepolicies that spur inflation and lift long-term rates, helpingbanks earn more from lending.

|A key question for that equation is whether deposits are stillas “sticky” as they have been for decades, or whether customers,freed from going to branches to deal with tellers, will demandhigher returns to stick around. Small deviations in beta can helpor hurt banks' bottom lines.

|JPMorgan's Lake told investors in February that the bank modeleda scenario in which the Fed raises rates by a quarter point twice ayear through 2018, and once in 2019. If the lender passes alongmore than half of that increase to depositors — abeta of more than 50% — it would reap $11 billionmore revenue from interest, she said.

|While that bodes well for profits, one assumption is notable. In2004, the beta was roughly 45%, she said.

|In the first quarter, analysts project the six biggest U.S.banks increased net interest income 8.5% to $49.1 billion, the mostsince 2010.

|Marty Mosby, an analyst at Vining-Sparks IBG, said banks havebeen slow to increase deposit rates because they're still workingto cover the expense of maintaining accounts. He expects to seemore movement after the Fed raises rates by another 25 basispoints.

|“We will be watching for indications of an uptick in depositbetas in the wake of Fed rate hikes in December and March,” JeffHarte, an analyst at Sandler O'Neill & Partners, said Monday ina note to clients.

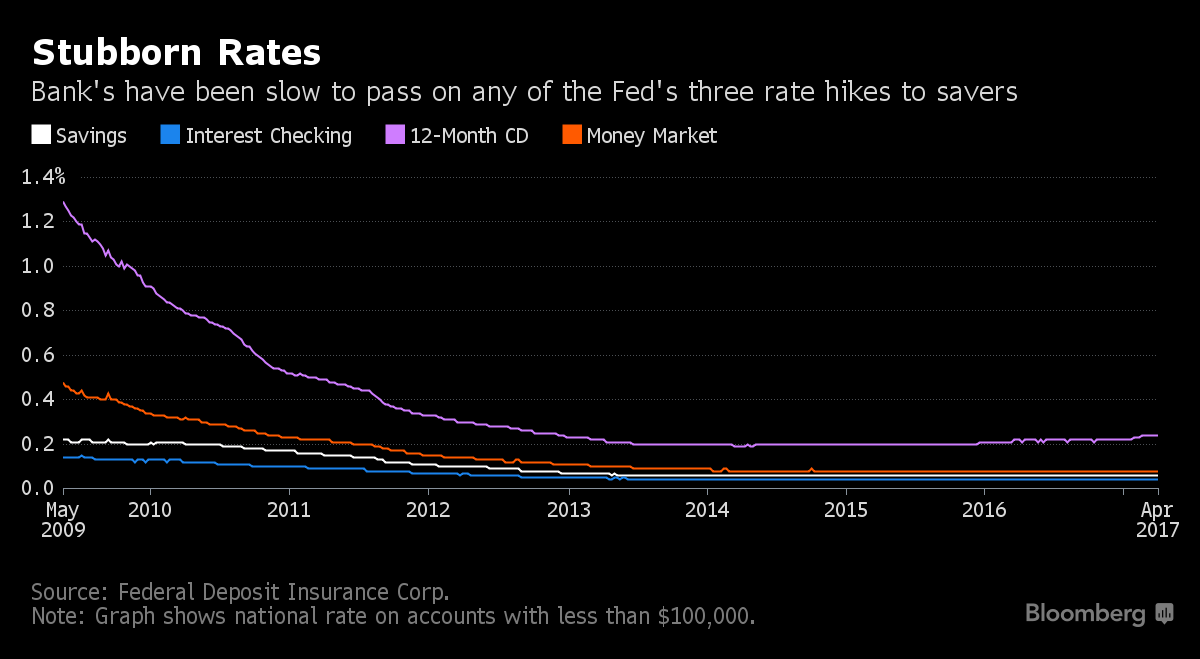

|At BB&T, customers with an eSavings account earned a 0.03%interest rate as of Friday — even less than inearly December 2015, just before the Fed began its hikes.

|'More Hype'

Banks, meanwhile, realize that consumers' patience won't lasttoo long, said Ray Montague, director of deposit product researchat Informa Research Services. His clients include bank executiveswho set rates to remain competitive. Some who used to request hisresearch monthly now ask for it once a week, he said. Those who gotit weekly are now asking for it twice a week or even daily. Thefear is that consumer behavior might change fast.

|“As there's more pressure, more hype, more news about increasedrates I think there's going to be more sense that 'I need toactually start shopping around looking for the best rate,'”Montague said. “That's what's going to rattle the banks.”

|

Bloomberg News

|Copyright 2018 Bloomberg. All rightsreserved. This material may not be published, broadcast, rewritten,or redistributed.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.