It turns out that bond investors do occasionally put down theircollective foot and refuse to be cash registers for bigcompanies.

|Just such a moment came late Wednesday, when CharterCommunications Inc. withdrew a planned $1.5 billion bond sale,citing “market conditions.” The reality is the telecommunicationscompany wanted to borrow money at rock-bottom rates and use theproceeds to buy back shares but dropped its plan when bondbuyers pushed back the tiniest bit.

|To be fair, this week has been a bit weaker for lower-ratedcorporate debt, largely because of lower energy prices that havepressured leveraged oil and gas drillers. But money is stillrelatively cheap. Borrowing costs for risky companies outside ofthe energy sector rose by a mere 0.10 percentage point in thepast week, to 5.38%, compared with the decade-long average of 6.7%.Yields on Charter bonds are still near record lows.

|Charter's spokesman, Justin Venech, chalked up the bond sale'scancellation as a display of corporate responsibility. “We areprice-disciplined, and this was opportunistic,” he told BloombergNews.

|There are a few lessons in this. First, it suggeststhat Charter, like many companies, has been utterly spoiled byultra easy monetary conditions, which have suppressed yields nearrecord lows. If yields aren't perfect, borrowers can simply waitfor a better time, which is nearly inevitable.

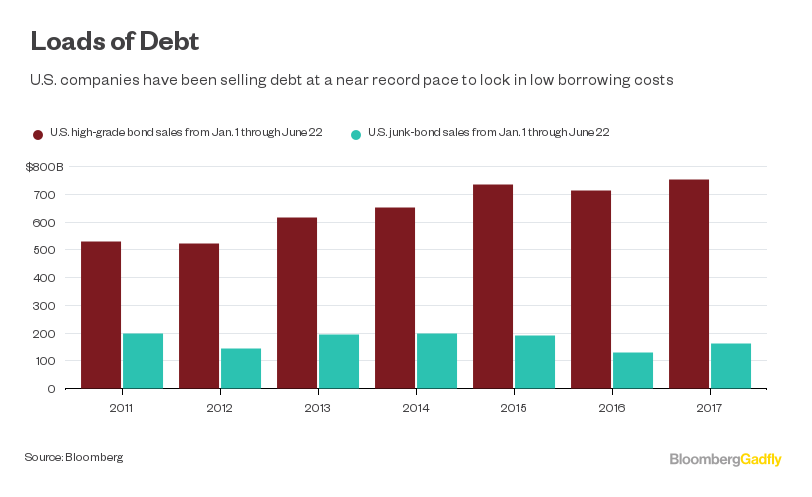

|Second, it highlights how corporations are borrowing cash theydon't need and will most likely be much more expensive to refinancein the future. U.S. corporate bond sales are near a record for thefirst half of the year. When (and if) borrowing costs do riseeventually, it will lead to pain for these companies that wouldhave been entirely avoidable.

|And third, it shows how companies have had the upper hand thisyear when dealing with bond investors. Many fundmanagers know they are getting a raw deal and go for itanyway. They don't expect to make a killing, but they have moneyand need to put it somewhere. They'll lose on an inflation-adjustedbasis if they park their cash in a money-market account, butthey're often insufficiently compensated for the risk they're oftenforced to take in the corporate credit market. This imbalance willmost likely continue for much longer than most investors wouldlike.

|While the Federal Reserve is slowly tightening the monetaryscrews, Japanese and European central bankers are still buyingassets and keeping short-term rates at record lows. No one seemsoverly worried about runaway inflation. Bonds have continued torally. Companies are fully aware of this dynamic. That's why aborrower like Charter is more than happy to wait out a rough patch.Even if bond investors balk on occasion, they'll probably return tobeing cash registers for corporate borrowers in short order.It's nice to see investors put up some resistance. In alllikelihood, such restraint won't last.

|

Bloomberg News

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.