These days, it's virtually impossible to become a bona fidemonopoly on Wall Street.

|But that's exactly what is happening in one vitalpart of the U.S. financial system, which has more than a fewtraders on edge.

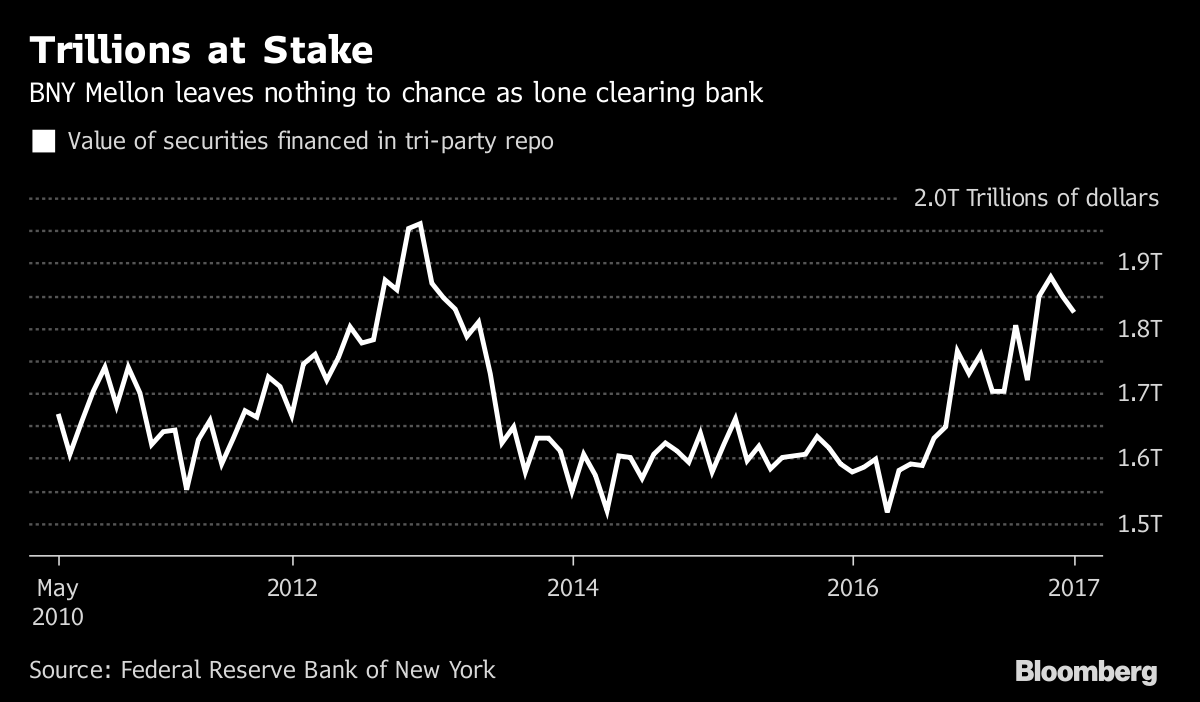

|Come mid-2018, just one entity—the Bank of New York MellonCorp.—will be responsible for ensuring almost two trilliondollars worth of securities financed by so-called repurchaseagreements are cleared and settled each and every day.With its lone longtime rival, JPMorgan Chase & Co., exiting thebusiness, BNY Mellon began the process of moving over clients thissummer.

|The problem isn't so much that BNY Mellon might abuse itsposition in what's become a highly regulated, utility-like part ofthe repo market. After all, JPMorgan threw in the towel after post-crisis rules made thebusiness costly and onerous. Instead, traders are worried thatrelying on a single bank for all clearing and settlement—whichinvolves checking every transaction is valid, transferring moneyfrom one account to another and safeguarding collateral backingeach contract—could mean big trouble if something goes wrong.

|And it's hard to overstate how important the repo market is tomodern American finance. The short-term loans, which dealersusually get by putting up U.S. government debt as collateral, servea crucial role in day-to-day trading on Wall Street. Not only dorepos support liquidity in the $14.1 trillion Treasury market, butthe financing they provide also helps grease the wheels of tradingin assets as varied as stocks, corporate bonds and currencies.

|“A single point of failure in the U.S. government-collateralizedrepo market, which is huge and is essentially the liquidity enginefor the country, is a little bit unnerving just in itself,” saidAdam Dean, managing director at Square 1 Asset Management. “It'snot an ideal situation.”

|Recall that it was widespread panic in the repo market thathelped lead to the collapse of Lehman Brothers Holdings Inc. and imperiled the financialsystem a decade ago. While the Federal Reserve has spearheadedefforts that have greatly reduced systemic risks in tri-partyrepo, having just one clearing bank has the potential to leave U.S.markets more vulnerable to everything from natural disasters andcomputer glitches to terrorism and cyberattacks.

|Brian Ruane, who oversees BNY Mellon's securities clearance andtri-party collateral business, says the firm is leaving nothing tochance.

|The bank, which had over 80% of the market even before JPMorgandecided to exit the business, has spent $100 million in recentyears beefing up its technology, which included upgrades to enablethree-way trade confirmations and the automatic substitution ofcollateral within repo agreements, to meet the Fed's tougherrequirements.

'Important Role'

That sum doesn't include the “very sizable” investment the bankmade to replace its three-decade-old clearing and settlementplatform. And since JPMorgan's announcement last year, Ruane saysBNY Mellon has spent even more on improvements, without saying howmuch.

|“We understand the important role we play in the marketplace andare preparing ourselves to take on this greater capacity,” Ruane, a22-year veteran at the bank, said in an interview from BNY Mellon'soffice in downtown Manhattan. “A key focus is on buildingresiliency, by investing more in back-up, capacity, technology,processes and people.”

|There's also plenty at stake for BNY Mellon itself. Fees fromclearing accounted for 12% of revenue last year, according to thebank.

|For years, regulators have prodded players in the industry tocome up with ways to prevent potential troubles in repos (which still play an important rolein the shadow banking system) from turning into a contagion thatthreatens broader financial markets, as they did in 2008.

|Clearing banks ended the practice of extending intraday credit,which regularly exceeded a trillion dollars. Repo dealers now haveto set aside more capital to protect themselves against potentiallosses. More contracts are now backed by government debt ratherthan mortgages or other risk assets.

Fire Sales

Nevertheless, the Fed says work still needs to be done toeliminate fire sales, which was a key risk during the financial crisis.Dealers and investors are still vulnerable to the kind of rapid,wholesale dumping of assets that sank Lehman, and the repo industryhas yet to implement a solution.

|Now, JPMorgan's impending exit is once again calling attentionto the stability of the repo market.

|“In this day and age when we are looking for risk mitigationacross a wide range of institutions, it's much healthier for themarketplace to have numerous clearers involved,” said ChristianRasmussen, the global co-head of repo trading at UBS Group. “Itmitigates any concentration risk.”

|For its part, BNY Mellon recently set up a unit called BNYMellon Government Securities Corp. to oversee its repo business andbolster governance. It will have a separate board that includes anumber of independent directors.

|“We recognize the systemic importance of this market and welcomethe steps that Bank of New York Mellon has taken,” Fed GovernorJerome Powell said last month. The Fed “will continue to haveheightened expectations for Bank of New York Mellon as it becomesthe sole provider of settlement services.”

Better Off?

The process hasn't been easy. Because of the legal and technicalcomplexities, Ruane says the bank has taken its time getting newclients up and running to ensure that everything runs smoothly. Asof late July, BNY Mellon had moved just four of JPMorgan's clientsonto its platform. And for the time being, JPMorgan will stillsafeguard their collateral, though both banks expect a majority tomake the switch to BNY Mellon in the future.

|Nobody is suggesting that the current state of affairs isbulletproof. In the event where one clearing bank goes down, itcould still take weeks for the other to pick up all the slack.

|“It's not like a firm can just flick a switch and move from oneto the other,” said Jeff Kidwell, the director of funding anddirect repo at AVM, a broker-dealer in Boca Raton, Fla.

|Darrell Duffie, a Stanford University finance professor who haswritten extensively on the repo market, says that because of issueslike its high fixed costs, clearing is one business that just mightbe better off as a monopoly. Having a single player do all theback-office work could increase efficiency and liquidity. Thatwould be a positive in the Treasury market, which critics say hassuffered as post-crisis rules have made it tougher to trade.

|“Fewer pipes required in the plumbing of the repo market shouldmake things cheaper,” he said.

|However, Duffie added one small, but important caveat. That'sall “assuming it doesn't cause clearing fees to go up,” hesaid.

|

Bloomberg News

|Copyright 2018 Bloomberg. All rightsreserved. This material may not be published, broadcast, rewritten,or redistributed.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.