President Donald Trump's pledges to overhaul taxes, trade,infrastructure and health care may thrill some corporate leaders,but it's causing many to delay expansions. That's bad forbanks.

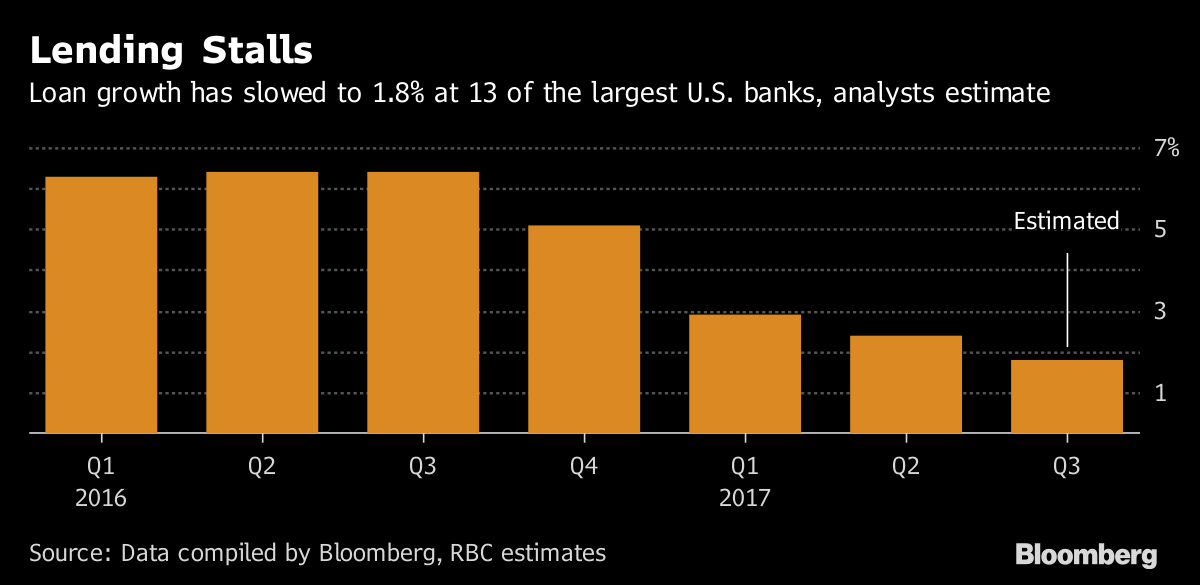

|Lending growth probably decelerated for a fourth straightquarter in the three months ended Sept. 30 across more than a dozenof the biggest U.S. banks, according to Royal Bank of Canadaanalysts and Bloomberg calculations. Their total loans may haveticked up just 1.8%, the smallest increase in more than two years,as commercial and industrial customers held off on buying equipmentand building plants.

|Executives are “hesitant to borrow in the face of uncertainty,”said Jason Goldberg, an analyst at Barclays. “Whether it'spotential tax reform, health-care uncertainties, or they're unclearwhat infrastructure spending is going to look like, you'vedefinitely seen corporates take a pause.”

|Washington's inaction has been frustrating bankers for months, asentiment that may surface anew when they start posting quarterlyresults this week. During the last round in July, JPMorgan ChaseCEO Jamie Dimon lashed out, saying, “There would be much strongergrowth if there were more intelligent decisions and less gridlock.”In June, Bank of America chief operating officer Thomas Montagsaid corporate clients need clarity to make big investmentdecisions.

|Trump and his top economic adviser, Gary Cohn, have said theyexpect the financial industry to help fund growth. But instead, adearth of progress on big legislation has stymied thatbusiness.

|Congressional Republicans spent much of September trying toresurrect a failed health-care bill. Then Trump told lawmakers his$1 trillion infrastructure plan may not rely on public-privatepartnerships, potentially throwing a wrench into a key priority.The president also released a tax plan that many analysts considerunlikely to win support until designers can prove it won't balloonthe federal deficit.

|For banks, the uncertainties are compounding challenges inlending, which also is being constrained by tighter regulation andslower-than-expected interest-rate hikes — factors that havecrimped trading revenue too. Low yields have encouraged firms toissue bonds and use the proceeds to repay bank loans, said AlisonWilliams, an analyst at Bloomberg Intelligence. U.S. Bancorp CEOAndrew Cecere addressed the challenges at an investor conferencelast month.

|“With the low yield curve, there was a lot of debt issuance, andthat debt issuance was used to pay down some bank lending,” hesaid. In addition, “there was some more uncertainty that enteredthe market because of some of the slowdown in the perceived timingof tax policy and trade policy and regulation,” slowing companies'capital expenditures.

'Mental Signal'

Corporate executives' outlook for the next six to 12 monthsdeteriorated in July and August, with some respondents citingheightened policy uncertainty, the Federal Reserve Bank of Chicagosaid last month. The number of workers on U.S. payrolls declined inSeptember for the first time since 2010, reflecting majordisruptions from hurricanes Harvey and Irma.

|For now, bank investors are willing to look beyond that. The24-company KBW Bank Index surged more than 30% from the Novemberelection to early March on optimism that Trump's administrationwill eventually ease bank regulation, reignite inflation and driveup interest rates. The rally resumed in September as attentionshifted to taxes.

|“People were underweight financials for a long time,” said ChrisWhalen, an independent analyst and consultant. “When Trump gotelected that was a mental signal for these guys that we shouldincrease our allocation.”

|Investors continue to see reasons for optimism. Trump's plan tocut corporate tax rates would be particularly beneficial for banks,whose burdens are often elevated by a lack of deductions. The sixlargest U.S. banks could see net income rise $6.4 billion under theadministration's proposal. And lenders still produce big profits.JPMorgan generated $26.5 billion in the 12 months through June, arecord for any U.S. bank.

|Yet expectations for the third quarter are measured. JPMorgan,the nation's largest bank, may say Thursday that adjusted profitrose 2% to $5.89 billion, according to analysts surveyed byBloomberg. At Citigroup Inc., set to report the same day, profitprobably slipped 1% to $3.57 billion.

|Wells Fargo & Co. and Bank of America report the followingday and Goldman Sachs and Morgan Stanley release earnings nextweek.

|There are other reasons for concern. While consumers are stillborrowing more, there's mounting evidence they're becoming lessreliable, potentially ending a period in which losses were low.Credit cards face heightened competition, while an overheated automarket has led some lenders like Wells Fargo to pull back.

|And for mortgage lending, a big driver for banks in the run-upto the 2008 financial crisis, new rules have made it more difficultto make money. Survivors have been buying loans from smaller“correspondent” lenders, a strategy that's started to run out ofroom.

|“You will see some pain this quarter,” Whalen said. “JPMorganand Wells Fargo have been bidding aggressively.”

Trading Declines

Trading also is expected to be down, in part because the lack ofcongressional action has left clients with few reasons to buy orsell. Executives from JPMorgan, Citigroup and Bank of America toldinvestors last month to expect declines ranging from 15% to 20% inthe third quarter from the same period a year ago.

|That may leave investors and analysts looking past thisquarter's results to the end of the year, when lawmakers may havemore progress to show on tax policy and other priorities.

|“Banks tend to be more optimistic looking out than they are inthe current quarter, so we'll see,” Barclays's Goldberg said.“Pipelines are good. At the end of the day though, loan growth is areflection of the economy and economic growth has been a little bitmore subdued than desired.”

|

From: Bloomberg News

|Copyright 2018 Bloomberg. All rightsreserved. This material may not be published, broadcast, rewritten,or redistributed.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.