A new Financial Accounting Standards Board (FASB)standard, ASU 2017-12, was released in August 2017. The goal was tosimplify hedge accounting rules and reporting.

A new Financial Accounting Standards Board (FASB)standard, ASU 2017-12, was released in August 2017. The goal was tosimplify hedge accounting rules and reporting.

The standard takes effect for public companies for fiscal yearsstarting after December 15, 2018, and for private companiesbeginning after December 15, 2019. However, the standard permitsearly adoption, spawning an interesting question: Is there abenefit to adopting prior to the beginning of 2018?

|The answer depends on whether the company has recorded losses orgains, or neither, from ineffectiveness in cash-flow hedgingrelationships.

|Many organizations are choosing to wait until 2018 to adopt ASU2017-12, but even a one-day difference in adoption—January 1, 2018,vs. December 31, 2017—could result in a very different outcome on acompany's financial statements. Finding the right answer for yourbusiness will require you to perform a quick analysis. Forsimplicity in presenting the approach, we will assume that the endof your current fiscal year is December 31, 2017, and that your newfiscal year begins January 1, 2018.

|To perform the analysis for your company, you will need toidentify all derivatives that are open and designated in acash-flow hedging relationship at year-end. For thesederivatives—and only these derivatives—quantify the cumulativebalances of the derivatives' gains or losses at the end of FY2017that are due to the hedges' ineffectiveness. Next, bifurcate thecumulative gains/losses associated with these derivatives intoamounts recognized during FY2017 and those recognized in prioryears.

||

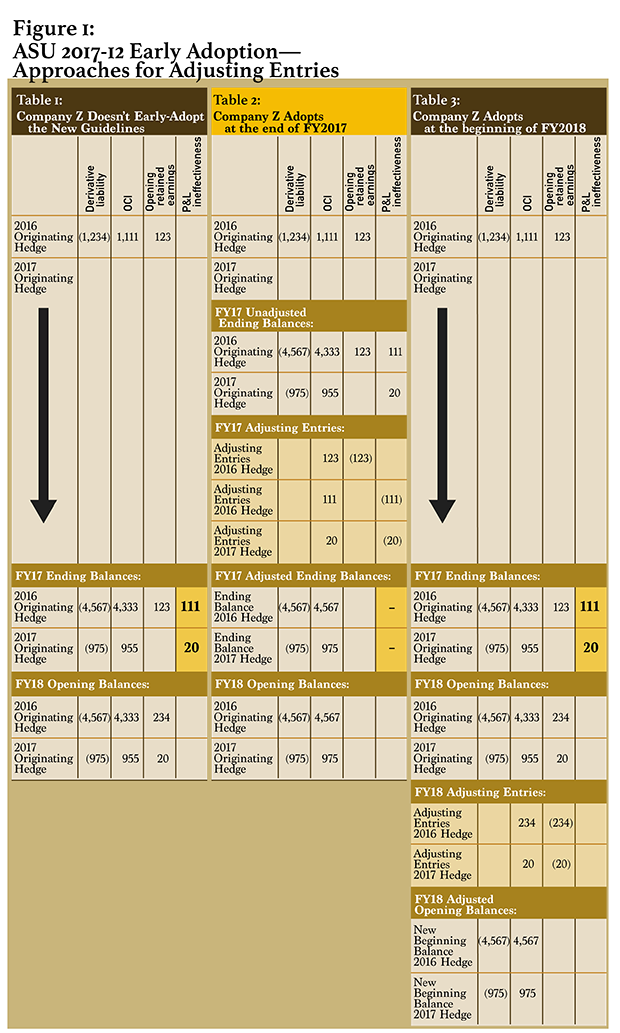

Company Z: An Example

To understand how these numbers are used, consider the exampleof Company Z, which has two open derivatives at year-end. The firstderivative, which we'll call “2016 Hedge,” was designated in 2016.The second, which we'll call “2017 Hedge,” was designated in 2017.Both remain designated in cash-flow hedge accounting relationshipsbeyond the end of 2017.

|Suppose that at the end of FY2017, Company Z has recorded acumulative $234,000 loss for the 2016 Hedge and a cumulative$20,000 loss for the 2017 Hedge. The loss associated with the 2016Hedge needs to be further divided into the losses recognized inFY2017 (say, a $111,000 loss) and FY2016 or all prior periods (a$123,000 loss).

|Table 1 on Figure 1, below, shows the FY2017 opening and closingtrial balances and the FY2018 opening trial balance for Company Zif it decides not to adopt the new guidance at all.

|Early adoption. If, instead,Company Z chooses to adopt ASU 2017-12 at the end of 2017, thecompany will adjust FY2017's beginning (January 1, 2017) openingretained earnings with a credit equal to $123,000 and a debit toOther Comprehensive Income (OCI).

|Next, the current year-to-date ineffectiveness will be reversedby crediting earnings of $111,000 for the 2016 Hedge and creditingan additional $20,000 to earnings for the 2017 Hedge, thenoffsetting those changes with a $131,000 debit to OCI.

|After these entries, OCI will equal the fair value of the twoderivatives at year-end (assuming time value is not excluded fromthe hedging relationship) and at the start of the new fiscal year.Table 2 in Exhibit 1 shows the FY2017 opening and closing balancesand the FY2018 opening balance for Company Z if it adopts the newFASB guidance on the last day of FY2017.

|

Adoption at beginning of 2018. Ifthe same company were to wait until the start of 2018 to adopt thenew guidance, it would adjust its opening retained earnings for2018 with a credit of $234,000 for the 2016 Hedge plus $20,000 forthe 2017 Hedge, then offset those changes with a $254,000 debit toOCI.

After this adjustment, OCI would equal the fair value of thederivative at the beginning of the new year—again, assuming thattime value is not excluded from the hedging relationship. Table 3on Exhibit 1 shows the FY2017 opening and closing balances and theFY2018 opening balance for Company Z, if it adopts the new guidanceon the first day of FY2018.

||

Conclusions

A company should review the amounts and direction of cumulativeineffectiveness to determine whether adopting the new FASB guidanceprior to fiscal year-end is in its best interests, or whether itwill be better off waiting until the start of the new fiscal yearto adopt.

|If your company has registered ineffective losses, it should bemotivated to adopt the standard at the end of the year. Otherwise,it will end up running those ineffective losses through itsfinancial statements twice: Once during FY2017, as thealready-recorded ineffectiveness, and again in FY2018, as aneffective component—being made whole through an adjustment to theFY2018 opening retained earnings, which will likely be invisible tostakeholders. Please note: Should a company choose to adopt theFASB guidance in the current year, it will likely need to evaluatethe materiality of reversing ineffectiveness in previous quartersof the current year.

|Conversely, if your company has earned gains fromineffectiveness due to your existing hedge portfolio, you have theopportunity to keep the gains from ineffectiveness in the currentyear and re-record those gains in 2018 by waiting to adopt thestandard at the start of the year—again, the gain being reversed islikely to remain an unnoticed adjustment to the next year'sbeginning retained earnings.

|As this example demonstrates, there is an opportunity for somecompanies to unwind losses from ineffectiveness by adopting ASU2017-12 prior to year-end, and there is an opportunity forcompanies that have gains from ineffectiveness to re-book thosegains again the following year by waiting to adopt after year-end.There aren't any timing benefits for those entities fortunateenough to not have to record ineffectiveness in their cash-flowhedging relationships.

||

——————————–

| Helen Kane is arecognized leader in the application of ASC 815 (formerly FAS 133,“Accounting for Derivative Instruments and Hedging Activities”)within corporate environments. She founded Hedge Trackers in 2000 as a FAS 133consulting and outsourcing firm providing deeply technical yetpractical solutions to Fortune 1000 companies.

Helen Kane is arecognized leader in the application of ASC 815 (formerly FAS 133,“Accounting for Derivative Instruments and Hedging Activities”)within corporate environments. She founded Hedge Trackers in 2000 as a FAS 133consulting and outsourcing firm providing deeply technical yetpractical solutions to Fortune 1000 companies.

|

If your organization is still unsure about how the new ruleswould affect your financial outcomes, the Hedge Trackers team would be happyto help with modeling the impact and recommending an implementationplan to maximize the advantages.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.