A crescendo built in thefinancial services industry late last year, as the effective dateapproached for sweeping new regulations. MiFID II, the European Union's version ofDodd-Frank, has capital markets professionals and their internalcompliance colleagues scrambling to position themselves on theright side of this far-reaching and comprehensive regulation.

A crescendo built in thefinancial services industry late last year, as the effective dateapproached for sweeping new regulations. MiFID II, the European Union's version ofDodd-Frank, has capital markets professionals and their internalcompliance colleagues scrambling to position themselves on theright side of this far-reaching and comprehensive regulation.

Why should a U.S.-based corporate finance officer or riskmanager care about a massive new regulatory framework across theAtlantic? The reason is simple: At the heart of the regulation is amandate for investment firms to adopt “best execution” practices.Investment firms are broadly defined as any legal entity whoseregular occupation or business is the provision of one or moreinvestment services to third parties and/or the performance of oneor more investment activities on a professional basis.

|Corporate treasurers who interact with European financialmarkets and securities may be directly impacted by the newregulations. Others may be indirectly affected. In the financialmarkets, fiduciary responsibility is fundamental, so the pursuit ofbest execution is logical. The pursuit of shareholder value in thecorporate world is not dissimilar from fiduciary responsibility.Therefore, it's not a stretch to imagine how the concept of bestexecution might apply to corporate treasurers and risk managers aswell.

|The good news is that MiFID II guidelines relating to increasedmarket transparency, best execution, and the identification ofexplicit transaction costs represent an opportunity for treasuryfunctions to improve the efficiency and execution of financialtransactions.

||

What Best Execution Is Not

The term “best execution” is widely misunderstood because almosteveryone is sure of exactly what it means. When the concept of bestexecution was first introduced in the 1980s, it referred to thepursuit of the best available price for the purchase or sale of asecurity in a burgeoning electronic marketplace. Over time, though,regulators in both the U.S. and the European Union realized thatthe concept of “best execution” is much more complicated thansimply trying to get the best possible price.

|Three decades ago, the technologies underpinning the capitalmarkets—such as lower latency trading solutions, individualaggregated liquidity venues, and new algorithmic order types—gaverise to issues that had the potential to undermine a singularbest-price objective. Speed and execution choice became prominentconcerns.

| In the early days of “bestexecution,” the focus was on equities, fixed income, andderivatives markets. Participants in the foreign exchange (FX)marketplace were largely left alone. After all, the FX market washuge, fragmented, and governed by a credit structure in which realmoney customers—corporations, pension funds, and assetmanagers—dealt directly with their banks on a one-to-one basis. Theemergence of electronic execution platforms (ECNs) some 20 yearsago did little to alter the FX trade execution experience of thecorporate trader.

In the early days of “bestexecution,” the focus was on equities, fixed income, andderivatives markets. Participants in the foreign exchange (FX)marketplace were largely left alone. After all, the FX market washuge, fragmented, and governed by a credit structure in which realmoney customers—corporations, pension funds, and assetmanagers—dealt directly with their banks on a one-to-one basis. Theemergence of electronic execution platforms (ECNs) some 20 yearsago did little to alter the FX trade execution experience of thecorporate trader.

That began to change about a decade ago. The global financialcrisis led to two market-changing pieces of regulation: Dodd-Frankin the United States and MiFID II in the European Union. Fundamental toboth was a demand that transparency be applied to allelements of capital-market activity. In 2009, the first large,public claims of pricing manipulation in the FX markets came tolight. The WMR FX benchmark crisis came next, followed by a steadystream of enforcement actions. All of a sudden, participants in theforeign exchange marketplace were confronting the “best execution”challenge for the first time.

||

MiFID II Definition of “Best Execution”

The essential definition of best execution, as outlined in thecurrent MiFID II guidelines and as applied to financial servicesfirms (both buy-side and sell-side), is actually pretty clear: Allsufficient effort must be taken to ensure that every trade isexecuted on terms most favorable to the client, and the tradingparty must be able to prove it. MiFID II provides an objective anda recordkeeping requirement.

|The regulation tells financial services firms what informationthey should consider and capture from their trading activity,including price, cost, speed, likelihood of execution andsettlement, etc. EU regulators even provide guidance on theevaluation procedures that financial services firms should utilizebefore and after a trade occurs. Beyond this guidance, however,MiFID II does not prescribe specific actions that a financialservices firm can take to ensure it has achieved “best execution,”largely because best execution is a process that has no realendpoint.

|When the SEC and FINRA tackled the definition of “bestexecution,” they made it clear that both broker-dealers and assetmanagers (fiduciaries) are obligated to consider and constantlyre-evaluate alternatives to the trading options they are currentlyusing, in light of the goal of achieving best execution for “theclient.” The regulators' intent was to signal that every tradingparticipant is responsible for:

- identifying its execution alternatives,

- trying out those alternatives,

- evaluating them in the context of other alternatives, and

- utilizing several of those options.

Best execution is impossible to achieve if a trading participantcontinues using the same process blindly, to the exclusion ofalternatives. So the regulators said: “You can't just do the samething perpetually”; “You can't use only one or two alternatives”;and “You certainly can't be compliant if you do nothing.” Forexample, a fiduciary—and, by analogy, a corporate—that executes FXtransactions directly with a bank counterparty on a disclosed basisneeds to consider alternative execution strategies, such asexecuting anonymously on an ECN platform that sources liquidityfrom multiple market participants or employing execution algorithmsthat search for execution outcomes based on certain strategies.

|The word “best” suggests a singular, unparalleled process. Butthe actions demanded by the regulators require every tradingparticipant to utilize multiple alternatives so that it canconstantly evaluate them, replace those that are no longer workingoptimally, and continue to benchmark the alternatives against oneanother. This constant evaluation proves the fiduciary commitmentof the trading participant when representing its client'sinterests.

|While most corporations may not be directly regulated by MiFIDII, the company that pursues this type of “best execution” in itsFX transactions stands to reap significant benefits. In the FXmarketplace, achieving the best available price is a fleeting questaffected by factors like market impact and fill rates (how much ofa large order gets executed immediately at a particular price).It's impossible to know for certain whether the exchange rate atwhich a company's currency trade is executed is the best availableat the moment the trade is executed, which is why wise treasurersare continuously re-evaluating their trading alternatives.

||

Best Execution Is a Journey

The concept of best execution as a journey, not a destination,may be frustrating for FX market participants. Corporate financeofficers and risk managers are not speculators. Theirresponsibility is to execute FX trades that support the funding of,or payment for, activities their organization undertakes in othercountries. Corporate treasurers are largely passive risk managers,but they are still risk managers with a fiduciaryresponsibility.

|The regulations that have been introduced to rein in badbehavior and promote transparency in the financial markets havefundamentally interfered with everyone's status quo. The demands ofbest execution are forcing financial services firms to change theway they do business and are raising the bar globally for marketparticipants, including corporate treasurers and risk managers. Thejourney they must embark on requires their aggressive attention andengagement. Passive risk management activities must be transformedinto a process that is actually the destination. The result of thisjourney will drive greater efficiency, and the benefits of bestexecution will enable all market participants to reduce executionrisk and ultimately lower their cost of execution.

| The process diagram in Figure 1shows the journey corporate treasurers and other FX marketparticipants should follow to achieve best execution outcomes andadhere to the guidelines included in the FXGlobal Code (of conduct) issued earlier this year by the GlobalForeign Exchange Committee.

The process diagram in Figure 1shows the journey corporate treasurers and other FX marketparticipants should follow to achieve best execution outcomes andadhere to the guidelines included in the FXGlobal Code (of conduct) issued earlier this year by the GlobalForeign Exchange Committee.

The five elements in the journey to best execution are:

|1. Search

For some corporations and financial institutions, looking attrading alternatives comes naturally. For others, it's a whole newchallenge. The largest, most sophisticated corporations may alreadyuse multiple trading alternatives, have both ISDA and primebrokerage credit arrangements, and have embraced technology fully.However, a surprising number of companies still use voice orders, trade with a limited number ofcounterparties, and rely on the “request for quote” option whenthey do use technology.

|This part of the journey requires businesses to be open todifferent alternatives. For example, over the past several years,banks have built and begun offering real money customers, such ascorporates, algorithmic FX trading platforms that access a varietyof liquidity pools. These bank FX algorithmic platforms are anexample of the type of alternative that corporations mustconsider—among others—if they are going to comply with the bestexecution process.

|2. Selection

To follow the best execution roadmap in Figure 1, a treasurer orrisk manager must consider multiple trading alternatives. Relianceon just one or two alternatives does not provide enough variety toallow for an adequate evaluation when that part of the bestexecution journey occurs. An adequate selection process mustinclude an assortment of different trading choices to allow forfuture comparison.

|It is critical that the trading choices selected provide preciserecordkeeping/time stamping information for future analysis. Andthere is no point in selecting a trading alternative if that choicecannot provide the information necessary to track performance asmeasured against every metric, not just price. For example,corporates should have the ability to evaluate their FXtransactions against a reliable third-party benchmark, and theyshould have access to information that shows the available pricesand liquidity in a market before and after their trade execution,for analytical purposes. Thus, the selection process must bethoughtful and take into account all the elements of the bestexecution journey.

|3. Utilization

When a corporate treasurer has selected an appropriate set of FXtrading alternatives, he or she should be sure to allocate tradingvolume in a manner that facilitates the evaluation process that isfundamental to best execution. Large orders should not simply bechanneled to a particular trading option based on legacy practice,nor should small orders. The use of different order types andalgorithms should also be utilized to create a data set for futureevaluation.

|The regulators do not prescribe how long an organization shouldtake to reach a decision regarding the attractiveness of any FXalternative. The point here is that a corporation must use multipletrading alternatives to position itself to meet best executionstandards, and use them over a long enough time to allow for properevaluation.

|Once the best execution journey begins, two things becomeabundantly clear: First, this journey is not in a self-driving car.The FX market participant is completely responsible for its ownjourney. Getting around the process cycle takes commitment, energy,and constant engagement. And second, the journey never ends—thejourney is the destination.

|4. Evaluation

Regulators in the financial markets have provided clear guidancefor the evaluation process in the best execution journey, and avariety of commercial third-party tools have sprung up to performthe pre-trade and post-trade elements of a proper evaluation.

|Post-trade transaction cost analysis (TCA) was their initialfocus. A niche industry sprung up to evaluate trades executed byreal money customers. Not surprisingly, some TCA products arebetter than others, but at this stage it is not clear that the TCAprocess is much more than a “check the box” for many corporationsand financial firms. The providers of high-quality TCA tools offerreal value in the evaluation of alternative trading venues, whileless-sophisticated solutions can actually have the oppositeeffect.

|As corporate treasurers conduct evaluations of their tradingchoices, they must also measure their own ability to perform aneffective evaluation. Does the company have enough information? Aredecision-makers able to interpret the information they receive fromthird parties? The regulatory message is crystal clear: Thecorporation or financial firm is solely responsible for theevaluation; it cannot pass off responsibility to a third-partyprovider of TCA.

|The MiFID II regulation requires investment firms to perform apre-trade market check before each trade they execute. Thisexercise must be systematic and embedded in the firm's tradingpolicies and practices. Looking at a quote on a subscription screendoes not meet the regulator's requirement. On the buy-side, theFX Global Code guides trade execution, suggesting thatprotecting the client's trading intention and identity is a bestpractice. Then, once a trade is completed, MiFID II requires ananalysis of the adequacy of the trading outcome. TCA tools can do agood job of supporting these post-trade analyses.

|Evaluation is an area in which it makes sense for corporatetreasurers to follow the roadmap that the financial servicesindustry has developed for best execution. This end-to-end tradeevaluation process depends on access to relevant data and theanalytics to decipher that information. A corollary to this accessis robust recordkeeping that can be referenced at any time in thefuture. Given the challenging requirements of the evaluationportion of the best execution journey, it is imperative that acompany chooses trading alternatives that help meet the fulsomedemands of the best execution standards. Perhaps this is obvious,but an adequate evaluation can be performed only if tradingalternatives provide the data and analytics to allow thatevaluation to take place.

|5. Reflection

Best execution guidelines do not, in an absolute sense, dictatethe outcome of the evaluation process. The new MiFID II regulationdoes not judge; it places that burden squarely on the shoulders ofthe financial services firms. The regulators merely demand thatsuch judgments be made soundly and consistently. By analogy, if acorporate treasurer determines that a combination ofalgorithm-based execution platforms and single-dealer executionsdelivers the best trading outcome, then he or she merely needs todocument the results to answer the question “How so?”

|That said, the best execution journey requires a commitment toongoing review. The reflection portion of the journey may be thequickest, since it requires a look backward to study the outputsfrom the evaluation process: What factors were considered regardinganonymous vs. disclosed executions? Were pre-trade analyticsemployed systemically? And how well did the market participantexecute as analyzed by robust TCA?

|Coming out of this judgment phase, the FX market participant isobligated to begin its best execution journey anew. What newtrading alternatives have appeared recently or in the past year?What has the organization learned through the evaluation processthat encourages it to seek out other trading venues orapproaches?

||

When Best Execution Processes Make for Better TradeOutcomes

On October 17, 2017, the senior representatives of the UnitedStates, Canada, and Mexico who are leading NAFTA renegotiations held a press conferencefollowing the completion of their fourth week-long session. Thenews conference lasted approximately 20 minutes and includedstatements from each country's official. In the course of thesestatements, eagerly awaited by many in the FX trading community,the participants revealed that numerous “unconventional challenges”had arisen during this fourth session that would require creativesolutions and extended intercessions. Minister Freeland from Canadawarned that any result which would roll back 23 years of tradeprogress would cause fundamental harm to North American industries,particularly the automotive industry. The take-away from this newsconference was that the parties still had a long way to go in theireffort to “modernize” NAFTA.

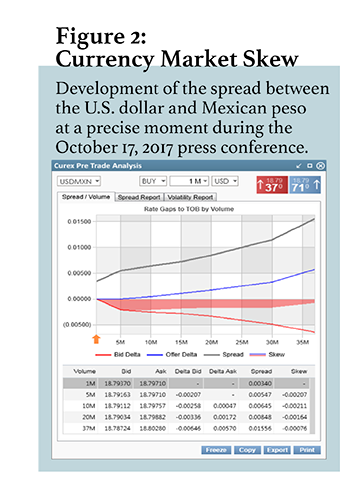

| As the press conferenceprogressed, the currency relationships between U.S. dollar (USD),Canadian dollar (CAD), and Mexican peso (MXN) became more volatile.For any corporate treasurer needing to transact in thosecurrencies, real-time knowledge of the market's movement would havebeen extremely valuable. One pre-trade analytical tool revealed themarket skew shown in Figure 2.

As the press conferenceprogressed, the currency relationships between U.S. dollar (USD),Canadian dollar (CAD), and Mexican peso (MXN) became more volatile.For any corporate treasurer needing to transact in thosecurrencies, real-time knowledge of the market's movement would havebeen extremely valuable. One pre-trade analytical tool revealed themarket skew shown in Figure 2.

As Figure 2 illustrates, prices skewed significantly in favor ofthe offered side of the market reflecting increased interest inselling USD against MXN. A company needing to sell USD against MXNwould want to do so as aggressively as possible, to sell theirinterest in front of an increasingly weak USD market. If thecompany's treasurer followed best execution principles, his or herpre-trade market check would have revealed the information inFigure 2. Having direct access to this data—without calling a bankand disclosing trading interest—would have been critical for acorporate treasurer interested in achieving a best executionoutcome.

|While this illustration relates to a singular event, the processof best execution, if followed consistently, will always allow thecorporate treasurer to have pre-trade market intelligence, as wellas a post-trade perspective to better understand the quality ofevery trade completed and to inform them of how to improve theirexecutions going forward.

||

It's Time to Start the Best ExecutionJourney

Following the process that is the best execution journey willabsolutely deliver benefits to every corporate treasurer and riskmanager. By following the five-phase process, an FX marketparticipant will achieve greater efficiency through access tobetter intelligence, and that will result in lower total costs inFX executions.

|This point about total costs is important. FX marketparticipants are too often unaware of the market impact of theirtrading choices. Market impact—price changes caused by executionperformance—is a real economic cost of execution. This hidden butreal cost can occur because of information leakage and evenfront-running. And the information leakage may be the direct resultof the execution choice made by the FX market participant. Is thecompany executing by voice, creating execution delay? Is it usingrequests for quotes (RFQs), which reveal its trade intention andsize? Is it trading anonymously? Is it executing on a venue inwhich its trade can be rejected? A corporate treasurer who followsthe best execution processes described in this article will take asignificant step to avoid those costs.

|Adopting the best execution process delivers outcomes that willbuild confidence whenever an FX execution is required. Taking asystematic approach supports a reliable, sustainable, andtransparent protocol that alleviates performance pressure andsupports better risk management. Best execution in FX, and in everyasset class, is a journey that requires commitment and attention.The regulations coming out of the financial marketplace haveprovided a map that every market participant should follow.Corporate treasurers and risk managers should embrace thisjourney.

|

James L. Singleton isthe chairman and CEO of Cürex Group, a New YorkCity-based institutional foreign exchange executionservices and data analytics company.

James L. Singleton isthe chairman and CEO of Cürex Group, a New YorkCity-based institutional foreign exchange executionservices and data analytics company.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.