European debt markets have suddenly become more appealing tosome big American corporations again, spurred in part by monetarypolicy changes.

|Several American household names have recently crossed the pondto issue debt in Europe. Companies such as Altria Group Inc.,Coca-Cola Co., Ford Motor Credit Co., and International BusinessMachines Corp., among others, together have sold almost 18 billioneuros (US$20.2 billion) in so-called reverse Yankee bonds thisyear.

|“We have shifted from what was a buyers' market, to the extentthat there was buying back in December and November, to very muchan issuers' market now,” says Morgan Stanley strategist SrikanthSankaran. He points out that investors who had moved to thesidelines have now re-entered the market, allowing for“surprisingly strong” liquidity in European credit markets.

|The debt sales have been well received. Colgate Palmolive Co.,for example, was seven times oversubscribed, allowing for a 25basis point (bps) spread tightening from initial price thoughts,considered a floor for pricing.

|

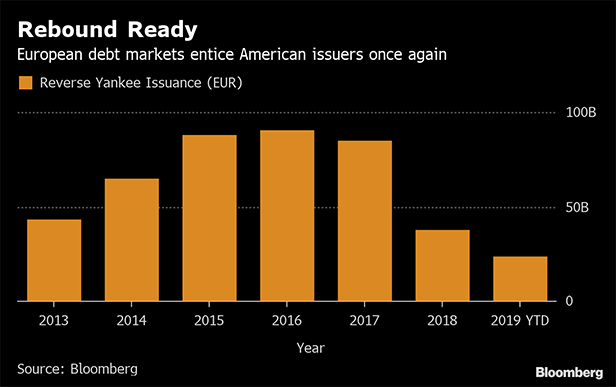

The recent spike in reverse Yankee issuance is nothing out ofthe ordinary, according to Hans Mikkelsen, Bank of America's headof U.S. high-grade credit strategy, who says, “We are reboundingfrom levels of last year to levels that are more natural.” Hepoints to the lower borrowing costs in Europe and issuers' desireto create a balance between assets and liabilities abroad ascatalysts.

|Since 2012, 10-year German bunds have yielded less than 10-yearU.S. Treasuries, contributing to a cheaper credit environment whencompared with the United States. Partly as a result, euro issuancein the five years that followed also jumped. That being said, 2018saw a drop-off in reverse Yankee issuance, begging the question ofwhy.

|Europe had a more volatile funding environment compared with theU.S. last year, amid political risks and the slowing ofquantitative easing. The European Central Bank (ECB) announced thismorning that it will keep rates at record lows for longer, to helpstimulate economic growth. Its recent patient stance has helpedtighten spreads and decrease yields in the Eurozone.

|With the ECB's prior bond buying program, supply ineuro-denominated debt left for private investors dropped, creatingmore demand for new issues. The reverse Yankee issuers that dochoose to access euro debt markets are mainly investment-grade,multinational companies that are feeding the appetite to ownhigh-quality corporate debt. This is especially the case as U.S.growth, although slowing, is still a bright spot compared withother regions of the world.

||

What Comes Next?

As some American companies turn abroad for funding, foreignissuance in U.S. dollars is also declining. So far, 2019 hasseen only 5 percent of debt in the U.S. investment-grademarket (excluding financials) come from Yankee issuers, comparedwith an average of 13 percent last year.

|The opportunity that the Eurozone offers for issuers to borrowat lower rates while diversifying their investor base may continue.“I think we're going to see quite active reverse Yankee deals atleast for the time being,” says Mikkelsen.

|High cash balances in investor portfolios and patient centralbanks are keeping corporate bond yields low, says Sankaran, whoalso expects some degree of reverse Yankee issuance to continue inthe near term.

|American issuers also have the option of exchanging proceedsback into dollars. The five-year cost to convert payments fromeuros into dollars using cross-currency basis swaps has cheapened,providing an additional incentive to issue abroad.

|Gennadiy Goldberg, a strategist at TD Securities based in NewYork, says the key driver for the divergence between the euro andU.S. dollar has been tightening in the cross-currency basis swapsat the end of 2018.

|“The widening in cross-currency basis we saw over the early partof the year has certainly slowed, so for the moment, I would expectto see ample euro issuance to continue. However, if thecross-currency basis continues to widen, as it did earlier in theyear, then dollar supply could become more attractive relative tothe euro,” Goldberg said in an interview.

||

Copyright 2019 Bloomberg. All rightsreserved. This material may not be published, broadcast, rewritten,or redistributed.

Complete your profile to continue reading and get FREE access to Treasury & Risk, part of your ALM digital membership.

Your access to unlimited Treasury & Risk content isn’t changing.

Once you are an ALM digital member, you’ll receive:

- Critical Treasury & Risk information including in-depth analysis of treasury and finance best practices, case studies with corporate innovators, informative newsletters, educational webcasts and videos, and resources from industry leaders.

- Exclusive discounts on ALM and Treasury & Risk events.

- Access to other award-winning ALM websites including PropertyCasualty360.com and Law.com.

*May exclude premium content

Already have an account? Sign In

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.