.

.

In the evolving and volatile environment in which every business is operating today, re-evaluating the corporate liquidity forecasting process makes sense. Last week, we outlined a method treasury teams can use to design a "best fit" framework for their cash forecasting. But that's not the end of forecasting planning. Before they can implement their new framework, treasury should also review the supporting infrastructure they have in place.

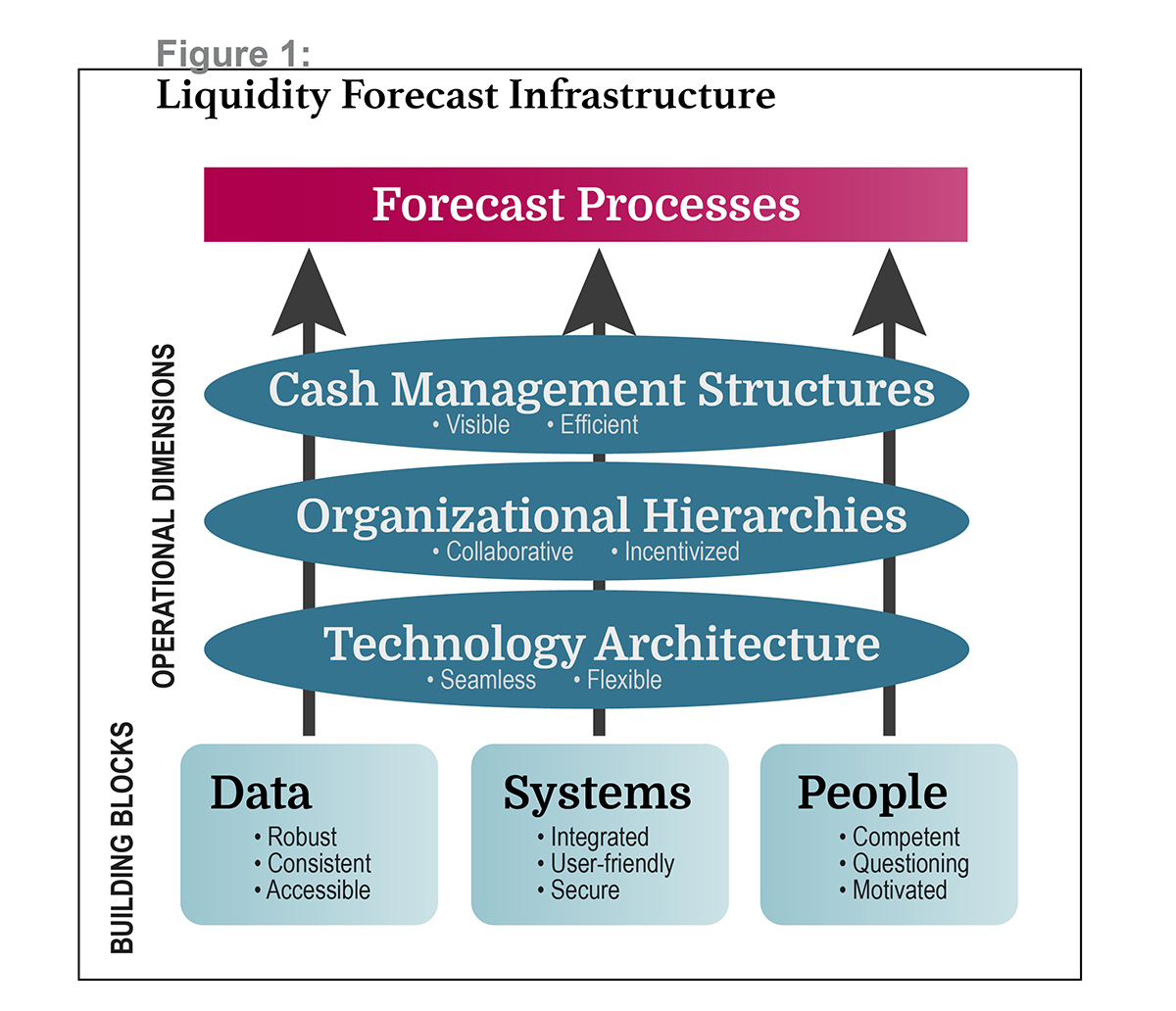

That's because we do not live in a perfect world. While a treasury group's new framework will establish the desired outputs of the liquidity forecasting process, the ability to actually produce those outputs will depend on the supporting infrastructure. This comprises everything that underlies the processes for producing the forecasts and measuring key performance indicators (KPIs). The core building blocks are data, systems, and people, but a treasury team also needs to factor in the business's operational dimensions: its technology architecture, organizational hierarchies, and cash management structures (see Figure 1).

1. Data: Is the required data reliable, complete, and easily accessible? Data points are the building blocks supporting the forecast, and the most common challenges revolve around availability and reliability. Typically, data sources for cash forecasting include processed payment and direct debit runs (for immediate liquidity); A/R and A/P ledgers (near-term); sales and purchase order books; scheduled contract items; and other regularly recurring costs, such as payroll.

Depending on the complexity of the cash management structure and the reporting capabilities of online banking applications, data inputs may also include actual bank balances, advance notifications of receipts and payments, and maturing trade finance items. Data that resides in accessible systems can enhance efficiency through automation, in addition to reducing the effort required to create intra-period forecast refreshes.

The further in the future an event is expected to happen, the less reliable data on that event is likely to be. For example, treasury may be able to total the value of outstanding customer invoices, but may not be able to pin down the timing with any certainty. Additionally, as the forecast horizon extends, available data will be only partially complete, requiring the blending of known data with projected estimates. Within larger organizations that use disparate technologies, different groups may rely on different data definitions, leading to inconsistent results. And partial or inaccurate data will obviously hamper the effectiveness of forecast processes, since estimates or modeling will have to fill the gaps. Depending on the technology environment, such a situation may result in manual workarounds, which reduce forecasting efficiency.

The availability of historical data in the right format to support variance analysis can present another specific challenge: Legacy finance systems may not support this. However, treasury may be able to create proxy historical data by separating out discrete items (e.g., payroll) and data roll-ups into broader category definitions, such as total customer receipts. Although not exact, this approach would provide some visibility, which is preferable to none.

Data mapping, for both the forecast and historical information, is useful in assessing the information's quality and reach. Documenting the source; definition; time horizon; coverage (How complete is the data over its horizon?); and accuracy, both in value and timing, provides a robust baseline to identify untapped data and to spot potential gaps where supplementary processes may be needed. Data mapping should underpin treasury's forecast design process.

2. Systems: Is there seamless access to data? Does functionality support the desired processes? Even if a company's liquidity forecasting data has no issues, the efficiency of the forecasting process may be compromised if the systems landscape is not fully integrated or lacks essential functionality.

A homogeneous technology architecture, such as an enterprise resource planning (ERP) system, will naturally support the forecasting process by ensuring data access and consistency across the organization. The same is true in relation to banking systems: A streamlined cash management structure will facilitate access to, and consolidation of, liquidity-related bank-reported data. Otherwise, the treasury team will need to rely on a variety of interfaces and data feeds to build a cash forecast.

Functionality to support liquidity forecasting should also cover process flow and compliance, flexible reporting, and modeling (to fill data gaps and facilitate scenario planning). Where these are lacking, the organization will need offline systems and/or manual processes, which will impact process efficiency and possibly reduce the robustness of outputs. A number of dedicated applications, such as Ripple Treasury's CashAnalytics, support liquidity forecasting with broader analytics, reporting, and modeling features, including artificial intelligence (AI).

Use of AI-generated modeling can be effective and save time. In fact, AI modeling might become a game changer as the solutions' algorithms improve. AI is skilled at identifying patterns in payment behaviors, seasonal variations, and operational disruptions at a much larger scale than humans can process in a given period of time. Natural-language processing can extract information about payment commitments from unstructured data sources, and predictive models can estimate the cash impacts of complex variables.

The potential to transform forecasting accuracy and reduce manual effort is substantial, but implementation of AI-based forecasting systems requires a clean data foundation. In addition, bear in mind that if an AI tool is not asked the "right" question, it may produce incorrect results. For example, an AI prediction of month-end customer receipts might be based on analysis of historical plus and minus days when, in reality, the customer always processes payments on the last Friday of the month.

3. People: Are the right people in place, and are they effectively focused? This can be one of the trickier aspects of forecasting to manage, but there are several common "human" factors that can reduce the effectiveness of the liquidity forecasting process—using personnel who lack needed skills and experience, focusing on low-value activities (e.g., number-crunching rather than analysis), and poor communication and engagement.

Having the right people managing the forecasting process is vital. Note that in selection of the "right" individuals, finance qualifications may be less useful than a solid understanding of the business's cash dynamics, together with an inquiring mind and a continuous-improvement attitude. Talent is expensive, but treasury teams must avoid the temptation of saving money by using junior staff to design and manage cash forecasts. That said, it would be counterproductive to employ senior-level treasury analysts in repetitive, mundane tasks. Treasury leaders will need to ensure that the organization invests appropriately in data and systems functionality, which, in turn, can free up resources to concentrate on analysis and interpretation, and can deliver actionable insights.

Poor communication and lack of feedback can also reduce employee engagement in—and, therefore, performance of—the forecasting process. Ensure that all participants in the process (both contributors of data and users of the forecast's outputs) are fully aware of the forecast framework, especially the underlying objectives and related KPIs, and that they fully understand what is expected of them. Specific features that support an effective cash forecasting process include troubleshooting guides and feedback mechanisms, consultation/involvement of all affected personnel whenever a process amendment is proposed, and appropriate change management practices.

Treasury can motivate participants to help optimize forecast results through incentives. Tying incentives to KPIs such as process compliance and forecast accuracy is one possible approach. But other, less formal mechanisms, such as recognition of performance ("naming and faming"), can also promote good practices.

On a wider front, treasury should use organizational structures to establish process champions, centers of expertise, and similar resources. Although there is no universal "best practice" in cash forecasting, there are clearly opportunities within each discrete business for sharing tips and experience.

One more people-related consideration: It's worth looking out for behaviors that can compromise forecast outputs. Common examples of such behaviors include deliberate underforecasting and altering normal business practices—for example, by holding back payments—in order to come in on target. Other problematic behaviors can be harder to spot, such as expediting "urgent" payments, which are not in the forecast, to bypass normal approval processes. Such actions can have significant impacts on both the forecast and business operations. Mitigating these risks requires constant vigilance, balanced incentives, and ongoing communication.

The Art of the Possible

Throughout the review of their existing forecasting infrastructure, the treasury team needs to keep expectations within the "art of the possible." Pragmatism is necessary to ensure that expectations are realistic, and compromise may be needed if infrastructure capabilities fall short of the perfect forecast process design.

At the same time, it's rare to find a team or department that isn't already stretched thin with projects. Treasury teams that simply don't have time for a full assessment of their cash forecasting needs and capabilities may want to focus on key areas with the potential to provide results in a shorter timeframe:

- Refreshing objectives, KPIs, and targets: Look at whether they reflect current business needs and stress points.

- Boosting employee communication and engagement: Determine whether there are specific performance issues that need to be addressed.

- Reviewing the technology: Look for opportunities to leverage advances in functionality and integration.

The organizations that excel at liquidity forecasting are those that clearly define what they're trying to achieve, build infrastructure appropriately scaled to their needs, and maintain discipline to evolve as conditions change. Treasury groups should review their fundamentals now, because the effort invested in getting the framework right will compound in value as uncertainties persist. And if the response, when treasury challenges the rationale behind current processes, is "because we've always done it this way," that is the surest possible sign that a process review is overdue.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.