A trader works on the floor of the New York Stock Exchange on May 4, 2026. Photographer: Michael Nagle/Bloomberg.

A trader works on the floor of the New York Stock Exchange on May 4, 2026. Photographer: Michael Nagle/Bloomberg.

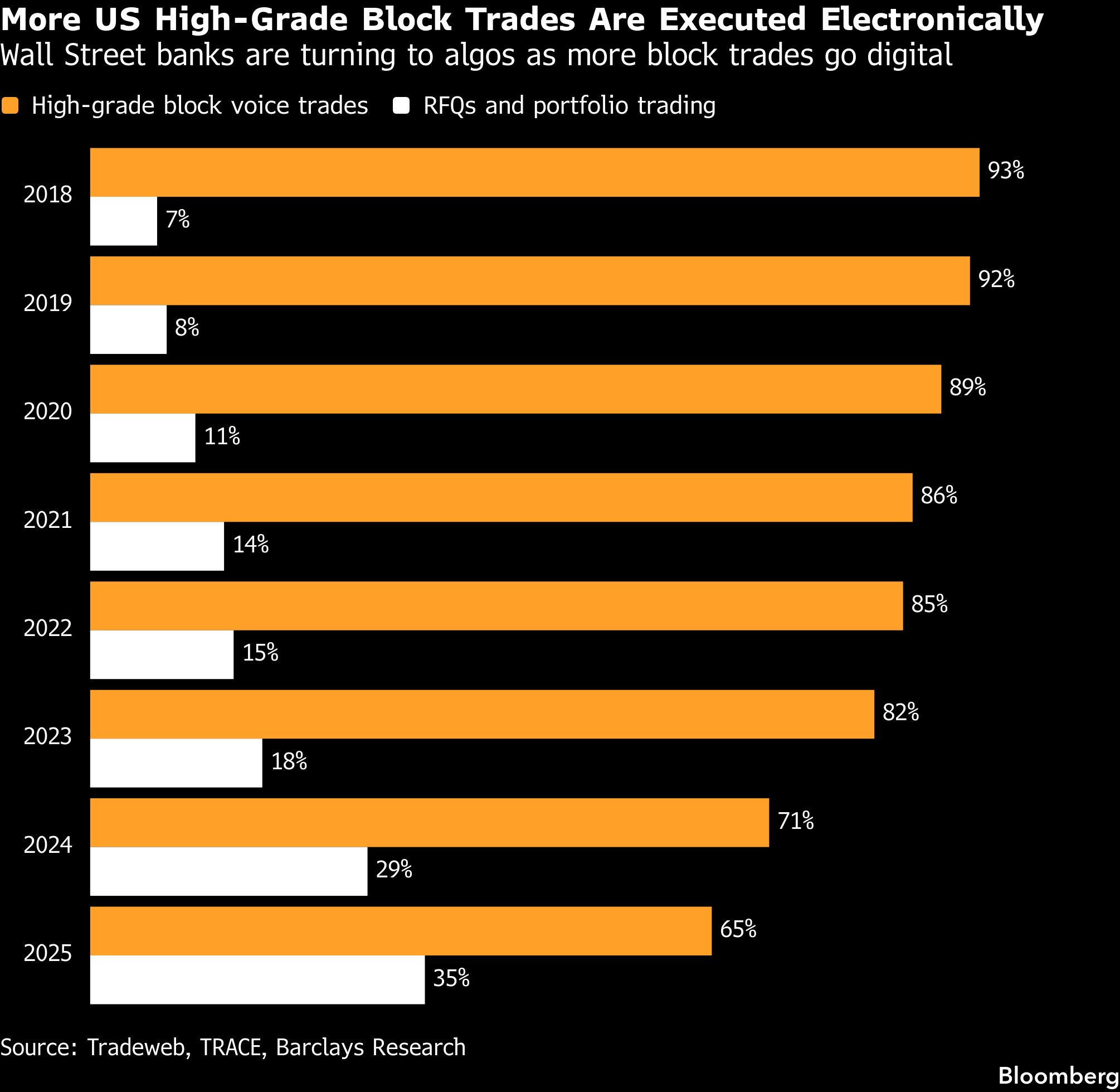

Wall Street securities dealers and money managers are increasingly relying on algorithms to execute even the biggest corporate-bond trades, the latest sign of movement toward electronic trading in a $12 trillion market that was long one of the biggest holdouts. Around 35 percent of block trades worth $5 million or more are now handled through RFQs, or electronic requests for quotes, and portfolio trades, which are mostly electronic, according to Barclays Plc's analysis of data on the investment-grade market through the end of last year. That's up from just 7 percent a little less than a decade ago.

This trend underscores the broader shift across the finance industry, where the electronic trading that dominates the stock market has been making steady inroads with fixed-income securities that were once considered more difficult to standardize. In recent years, both JPMorgan Chase & Co. and Morgan Stanley have increased the ability of their algorithms to handle bigger block trades.

"The voice trading business is really fading away," said Adam Jones, former head of portfolio and electronic trading at RBC Capital Management, referring to the traditional approach of arranging trades over the phone. "The algo teams are getting bigger. They're adding quant power and technology."

The transition has cut the cost of trading and helped to lower corporate borrowing costs more broadly by reducing the yield premiums that investors demand in return for buying less-easy-to-sell securities. According to proprietary pricing data from electronic-trading platform MarketAxess Holdings Inc., the so-called bid-ask spread—a commonly used measure of transaction costs—dipped to about 4.7 basis points (bps) on trades of more than $5 million during the first quarter, down from about 7.6 bps two years earlier.

Mark Clegg, the senior fixed-income trader at Allspring Global Investments, is among those who have welcomed the shift. Even as the Iran war was rattling markets in early March, he said, it took him less than an hour to execute a $600 million portfolio trade using an electronic platform—a trade that involved selling some securities and buying others with shorter maturities. Just a few years ago, he said, it would have taken days and required a flurry of calls to multiple dealers to haggle over the best price.

"For the first time in a long while, the buy side has the advantage in execution, and we're leaning into it," said Clegg. Allspring's global fixed income team manages $57 billion.

The electronic venues have gained even more traction when analyzed for all kinds of trades, according to Barclays' Zornitsa Todorova and Andrea Diaz Lafuente. The two said 2025 was the first year in which the share of overall trades executed through electronic RFQs jumped to 40 percent, overtaking voice-based trading by 3 percentage points. Tradeweb Markets Inc. data shows the same pattern: Algorithms now make up roughly 54 percent of total U.S. high-grade trading volume executed through RFQs on the electronic trading platform.

The bots aren't expected to take over trading desks completely, and most high-grade block trades are still executed by human traders, who account for 65 percent of total block volumes, according to Barclays. But analysts at the bank say the ratio could potentially flip to push as much as 60 percent of these trades to electronic platforms.

"It's the natural evolution of the market, but I don't necessarily see it, to be honest, as bad news for voice traders," Todorova said. "The market is bifurcating, and this has many different dimensions. The big trades are getting bigger; the voice trades are becoming more nuanced. The algos are getting better as well."

To keep up with a surge of client orders—executed in near-instant time and under shrinking margins—Wall Street's biggest banks and high-tech trading firms are increasingly turning to sophisticated algorithms to deliver liquidity with little to no human touch.

At Morgan Stanley, the bank's algorithm is now able to execute deals of up to $12 million according to David Massingham, the firm's global head of credit automated trading. He said the $5 million-plus investment-grade segment has grown to 12 percent of total algorithmic volumes, up from just a couple of percentage points five years ago. The improvement to the bank's trading systems is "enabling us to meaningfully increase the amount of liquidity we're able to provide in this space," said Massingham in an interview.

At JPMorgan, the notional size the bank's algorithm can handle has increased fivefold in the past few years as a result of demand from clients, according to Chi Nzelu, head of quantitative trading and research at the bank. The banker declined to give the notional size the algorithm can handle. "We've meaningfully expanded our electronic and algorithmic execution capabilities, with human traders providing active oversight—much like a pilot monitoring a highly automated aircraft," Nzelu said in an interview.

Bloomberg LP, the parent company of Bloomberg News, competes with electronic platforms including MarketAxess and Tradeweb in fixed-income trading, as well as providing data and information to the financial services industry.

—————————————————————

Copyright 2026 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.