Exports have remained one of the few consistent bright spots in the otherwise sub-par U.S. economic recovery. Their growth at times has added as much as two percentage points to the pace of the economy's expansion and is a major reason why American manufacturing has staged a comeback in recent years, a "renaissance" some have called it. But of late, with the dollar rising against the euro as well as the yen and growth overseas slowing or, in Europe's case, falling, questions have arisen about the sustainability of this export strength. Doubtless, the pace of gain will slow, but growth in exports is likely to continue.

Exports have remained one of the few consistent bright spots in the otherwise sub-par U.S. economic recovery. Their growth at times has added as much as two percentage points to the pace of the economy's expansion and is a major reason why American manufacturing has staged a comeback in recent years, a "renaissance" some have called it. But of late, with the dollar rising against the euro as well as the yen and growth overseas slowing or, in Europe's case, falling, questions have arisen about the sustainability of this export strength. Doubtless, the pace of gain will slow, but growth in exports is likely to continue.

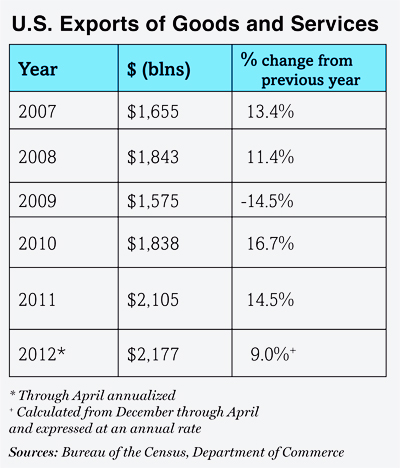

The U.S. export boom actually took off in 2007, held up remarkably well during the 2008-09 recession and has generally picked up momentum since. As the table below shows, exports of goods and services jumped 13.3% in 2007 and continued to grow almost apace in 2008, even as the global financial crisis rocked world economies. Unsurprisingly, exports fell in the global recession year of 2009, but they rebounded into 2010 and 2011 despite the disappointing pace of the global expansion. So far this year, as China reduced its overall growth expectations and Europe fell into recession, export growth has actually accelerated. Because exports amount to barely 15% of U.S. economic output, this performance, impressive as it is, could not turn a sluggish recovery into a rapid one, but it has been fast enough at times to add considerably to the pace of growth. In late 2007, net exports accounted for more than half the economy's expansion. In 2010 and early 2011, they accounted for one-third of the economy's growth.

The expansion of the global economy, especially in the emerging world, explains some of these gains. In particular, the 2007 export jump reflected the booms occurring in China, India and other emerging economies at the time, which sucked in industrial supplies and raw materials that the U.S. economy, among others, was in a good position to provide. Of course, the global downturn in late 2008 and early 2009 helps explain the export drop in 2009, but that picture quickly changed as emerging economies resumed their rapid growth trajectories in 2010 and the early part of 2011.

The expansion of the global economy, especially in the emerging world, explains some of these gains. In particular, the 2007 export jump reflected the booms occurring in China, India and other emerging economies at the time, which sucked in industrial supplies and raw materials that the U.S. economy, among others, was in a good position to provide. Of course, the global downturn in late 2008 and early 2009 helps explain the export drop in 2009, but that picture quickly changed as emerging economies resumed their rapid growth trajectories in 2010 and the early part of 2011.

Recommended For You

Also explaining the export picture are the declines in the dollar's foreign exchange rate that cumulatively enhanced U.S. producers' price competitiveness. Between 2002 and 2007, the euro rose about 40% against the dollar, while the yen rose more than 15%. The favorable currency patterns for exports continued through much of this more recent period too, further enhancing America's competitive position. In 2007 alone, the dollar cheapened almost 10% against the euro and it rose only slightly since, at least until much more recently.

The shift against the yen was even more dramatic. Between mid-2007 and late 2011, the yen rose almost 40% against the dollar. Not only did the currency moves help U.S. producers make inroads into European and Japanese markets, they gave them a huge edge against European and Japanese competitors in faster-growing markets such as China, India and Brazil.

There can be no denying, however, that if the dollar's recent gains persist, they will strip away some of this competitive edge. In recent weeks, for instance, the euro and the yen have each cheapened almost 5½% against the dollar. But because previous dollar declines gave American producers such huge pricing advantages, even recent dramatic currency moves leave much of this country's advantage intact. According to calculations by the Organization for Economic Cooperation and Development, underlying measures of comparable pricing—what econometricians refer to as purchasing power parity—put today's euro, at about $1.25, only just on a competitive par with dollar-based production. Comparable calculations for Japan show the yen still giving American producers a huge 35% pricing advantage against the Japan-based competition.

Though recent dollar strength combined with slowing global growth will retard the future rate of export gains, it should be clear that relative pricing advantages have hardly proceeded far enough to erase it. For one, trading arrangements are based on ongoing pricing and supply relationships built over long periods of time. Those that have developed in favor of American products during these years of great U.S. pricing advantages will take a long while to unwind. Given the American advantage implicit in the still pricey yen, it is doubtful that such a process has even begun or will begin for some time yet. If the euro is closer to competitive parity, it still offers no special pricing advantage that would prompt buyers to switch away from established American suppliers. On this basis, exports should continue to contribute to aggregate growth in the U.S. economy, albeit at a reduced rate of growth of say, 8% to 10%, rather than the 14%-to-17% range of the past three years.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.