Superstorm Sandy may have put a dent in the insurance industry's reversal of fortunes after a catastrophe-filled 2011, but commercial-property pricing may not increase as much as one might expect after the second-most damaging named storm to hit the U.S., a new report says.

In its “Marketplace Realities 2013 Spring Update,” insurance broker Willis says capacity remains abundant even for catastrophe perils. “Even with Sandy,” says Willis, “property losses totaled $65 billion in 2012, a 44 percent improvement over 2011's total, and the P&C insurance market saw policyholder surplus increase from $550 billion in 2011 to $570 billion in 2012.”

The market, the broker continues, was well capitalized to absorb 2012's losses.

The market, the broker continues, was well capitalized to absorb 2012's losses.

Recommended For You

Willis expects capacity to remain abundant in 2013, and while new capacity has not entered the market this year, the property space has not contracted.

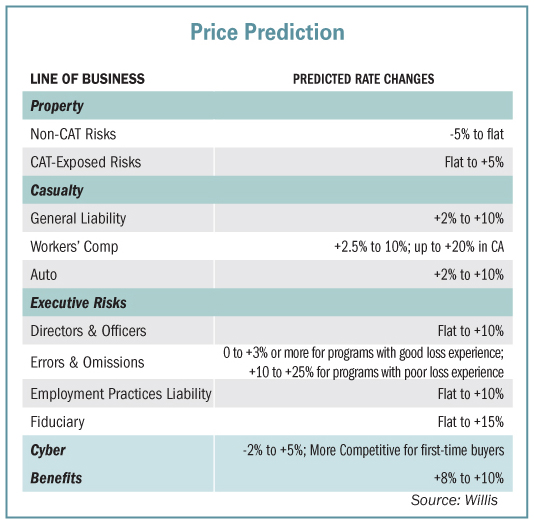

As such, Willis says it expects non-catastrophe rates to range from down by 5 percent to flat, and catastrophe rates to range from flat to up by 5 percent. Sandy-impacted areas though, “especially those accounts where flood limits are being reduced on renewal and [where] flood limits need to be restructured,” could see steeper increases.

While the storm may not have been a game changer with respect to rates, Sandy has altered underwriting, Willis says. “Insurers are reviewing definitions of Named Storm and Flood,” states the report. “In some cases, insurers are moving storm surge from the 'Named Storm' definition and including it under 'Flood.'”

Insurers are also expanding the northern boundary of the “Named Storm” territory from Virginia to Maine, and reducing limits and increasing deductibles for flood and high-hazard flood coverages.

Limits and deductibles are being looked at in the broader property market beyond flood as well. Willis says, “After Sandy, many insurers were caught by surprise, with numerous policies providing large limits ($100 million or more) and low deductibles ($100,000). This situation is being amended even if the account did not experience a loss from Sandy.”

For casualty risks, Willis says carriers are pushing for moderate rate increases generally for primary and umbrella/XS placements, “largely due to the sustained low interest rate environment.” The broker says capacity will keep the casualty market competitive though.

For workers' comp, Willis says claim frequency may be creeping up. “We have not definitively identified a driver, but candidates include the impact of economic conditions on employment opportunities, hiring of new or less experienced workers, the aging work force and consideration of how changes introduced by the Affordable Care Act will impact workers' comp.”

Some markets in the cyber risk space are looking to increase rates due to increased losses, but Willis says the market remains competitive, with rates ranging from down by 2 percent to up by 5 percent. In 2012, more than 2,600 breaches were reported in the U.S., or about seven per day, which is a new record high, says Wilis, citing Risk Based Security's 2012 Data Breach Quick View.

The directors and officers market continues to firm, although coverage terms and conditions are generally still competitive.

PropertyCasualty360

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.