For treasurers and other finance managers who've spent their careers in the United States, bribery and corruption may seem far-removed from reality. But for those who are responsible for financial management in other parts of the world, an insular attitude may be setting them—and their companies—up for some unpleasant surprises. A recent global study by Ernst & Young titled “Navigating today's complex business risks: Europe, Middle East, India, and Africa Fraud Survey 2013” reveals that some activities which seem taboo to most businesspeople in the United States are not as uncommon in the developing world.

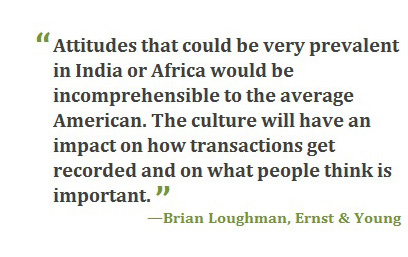

“Sometimes it's a challenge for U.S.-based finance managers or treasury folks who have never worked abroad to understand that people in their foreign subsidiaries may have a completely different perspective on how the world works,” says Brian Loughman, Americas leader for fraud investigation and dispute services with Ernst & Young. “That can lead to attitudes that could be very prevalent in India or Africa but would be incomprehensible to the average American. The culture will have an impact on how transactions get recorded. It will have an impact on the level of detail that gets recorded in the system, on what people think of as being normal, and on what people think is important versus what they think isn't important.”

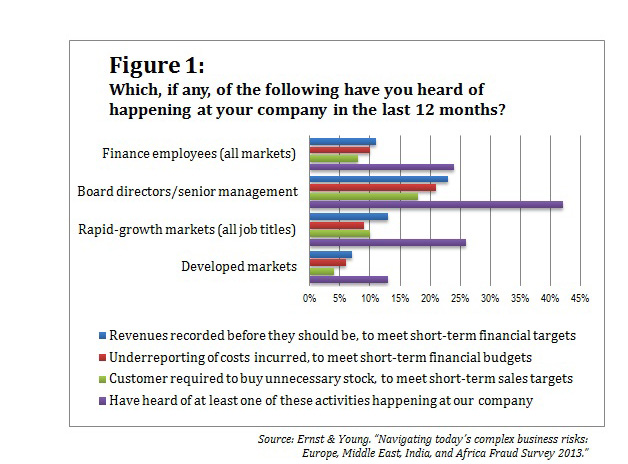

The survey polled more than 3,000 board members, executives, managers, and employees in 36 countries around the world. In rapid-growth markets, 26 percent of respondents have heard of people “cooking the books” in their company within the past year; see Figure 1, below. In the developed world, this number is half as large, although among respondents from all regions of the globe, 42 percent of board members and 24 percent of finance staff are aware of occurrences of financial manipulation in their organization.

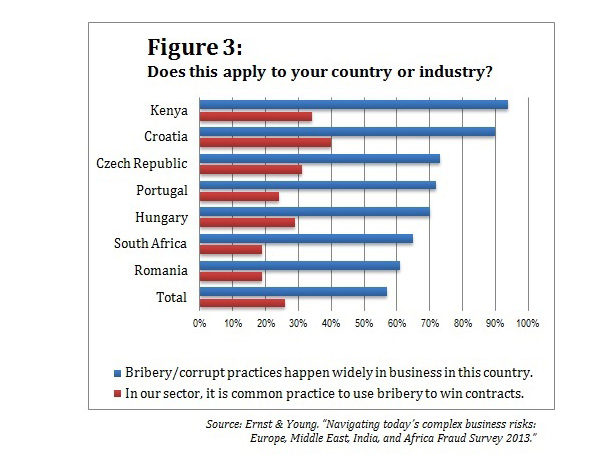

Bribery and corruption are also more widespread in the developing world than a U.S.-based management team might expect. In the Ernst & Young survey, 57 percent of respondents in the developing world said that bribery or corrupt practices happen widely in business in their country.

“What's interesting is that in a lot of cases, a large percentage felt that bribery and corruption was widespread in their country, but a smaller percentage felt it was applicable to the sector that their business is in,” Loughman says (see figure 3). “Clearly, that can't hold water. If two-thirds of people think there's a problem in their country but only 20 percent think it occurs in their industry, finance managers with operations in that country should make sure their controls are attuned to that sort of thing.”

“If I were a finance manager sitting in Peoria, Illinois, I'd see this survey as a very good refresher for internal controls,” Loughman adds. “I would look at making sure all the checks and balances in place in my organization were tweaked appropriately to reflect the inherent risks that appear obvious from this survey.”

In many companies, treasury plays a key role in overseeing checks and balances that prevent bribery and related activities. One way is to keep a close eye on aspects of performance that can be verified independently, such as cash flows and bank accounts. In one company Loughman worked with, his team discovered bank accounts that the corporate treasury function was unaware of.

“It was a very large, U.S.-headquartered company, and treasury really didn't know how many bank accounts the company had in its overseas network,” he says. “When we went overseas to different locations, we found 10 or 15 bank accounts that treasury didn't know existed. That's not to suggest there was any fraud, but things happen over time away from the home office. Treasury could have been leveraging all those accounts, and it created a lot of issues from a governance point of view.”

lot of issues from a governance point of view.”

Cash is monitored even less closely in some companies. “Some divisions of a company may be a bit of an outpost,” Loughman says. “For example, if you're in the oil and gas industry in the Middle East, most of your locations are going to be remote.” These locations may have to pay local suppliers in cash, so the company may keep a lot of cash on hand. “We've found that a lot of companies fill out this type of function without building sufficient controls around it. I had one client that had $500,000 in cash in just one country with no controls. That probably started as an initial request for a $5,000 cash float, and then over time as the business grew, it got bigger and bigger and no one ever checked on it.”

This obviously opens doors for corruption. “In the Middle East or Africa, if you have a lot of cash lying around, a lot of business managers may be tempted to leverage it to get things done more quickly with the government,” Loughman warns. “That could create a lot of FCPA [Foreign Corrupt Practices Act] exposure for the company. And ultimately, it's a books and records issue, which comes back to finance.”

Loughman offers several suggestions for mitigating potential problems. First, treasury and finance can work with internal audit to rethink controls in parts of the world that may need deeper investigation, perhaps on a rotational basis. “As companies grow in developing markets, they need to allow their checks and balances to flex accordingly,” he says. “They don't have to go chasing everything down with a microscope, but an internal audit review in this part of the world shouldn't look the same as it looks for the operation in Cleveland. Companies really need to make sure they're touching things that they would take for granted in the U.S.”

Second, Loughman recommends reconsidering training for staff who handle money in far-flung locations. In the example of the company Loughman worked with that had bank accounts the central treasury team didn't know about, internal audit tweaked its processes, and the U.S.-based treasury function conducted training exercises. “Companies should recognize the risk inherent in doing business in these locations, especially when they need to use cash rather than checks or credit cards,” Loughman says. “They need to look at the training they provide around anti-corruption for folks who have access to a lot of cash.”

Training sessions can also have the benefit of bringing new information to light. “If you get people together in the same room as part of a regular training, you can talk about the sorts of risks and issues they're dealing with,” Loughman says. “You need to be sensitive to the right kind of format for the culture, but you might be amazed at how much candor you can get in these sorts of discussions. That can be very powerful for corporate treasury and finance staff because it gives you a defensible basis for tweaking your processes.”

Loughman's third recommendation is to bring as many of the company's locations as possible onto centralized electronic platforms. “I think the days of allowing overseas locations to do delayed reporting or batch processing are over,” he says. “The expectation now is that data will come into your system from every location in a way that is analogous to how you collect it in the home office.” This enables companies to engage in forensic data analytics and to proactively monitor data. “That leads to exception reporting and allows time for the company's limited resources to follow up on issues.”

Finally, he says, the best way for a company to prevent problems is to crack down anytime it discovers noncompliance with anti-corruption, financial management, or other corporate policies. “In my experience, the most effective way to get a far-flung overseas location on board with how things are supposed to happen is to have consequences of improper behavior,” Loughman says. “Although it's always difficult to deal with those things, when you do, people tend to pay attention. That's when they really get it.”

——————

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Meg Waters

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.