It's no secret that many companies, both in the United States and abroad, have dramatically increased the amount of cash they keep on hand, in large part by increasing their long-term debt load. REL Consulting, which is a division of The Hackett Group, and CFO Magazine recently analyzed the financial statements of the 1,000 largest U.S.-headquartered public companies that are not in the financial sector. They found that among these companies, long-term debt has more than doubled over the past 12 years and has grown nearly 20 percent in the past three years.

This trend is understandable, since many businesses struggled with liquidity during the recent downturn—but it's not sustainable. With interest rates rising and corporate credit ratings falling, borrowing is becoming much more expensive, and for some companies funding sources may completely dry up. Finance professionals across the United States are re-evaluating their cash and borrowing needs.

"Even if interest rates spiked a little too much in the short term, they're trending upward," says Dan Ginsberg, associate principal with REL. "The baseline is going up. We've reached a point where every treasurer and CFO is thinking, 'What are we going to do in a higher-interest-rate environment, where we simply can't borrow at the great rates that we've been getting?' Our answer to that is: Look at your own organization, at the working capital that is tied up in it right now. That's free money. It's already yours; you just have to get it."

Recommended For You

Huge Amounts of Cash Waiting to Be Tapped

Much has been written about improving the efficiency of working capital, but corporate treasurers may be surprised to learn how much cash they could potentially free up through better working capital management. In their analysis of large public companies, REL and CFO Magazine quantified the value of the opportunity available to each organization if it improved efficiency in three ways: by reducing its inventory levels, reducing its accounts receivable (A/R), and expanding the value of its accounts payable (A/P) by extending the length of time it takes to pay suppliers.

They separated the companies into industry groupings, then organized companies within each industry into quartiles in terms of days inventory on hand (DIO), days sales outstanding (DSO), and days payables outstanding (DPO). (See the sidebar "Headline Metrics for Working Capital Management" on page 3 of this article.) For every company outside the top quartile in one of these metrics, REL/CFO calculated how much additional cash the organization would have available if it improved efficiency in its inventory, A/R, or A/P processes enough to bring the associated metric to the levels achieved by the top quartile of businesses in its industry.

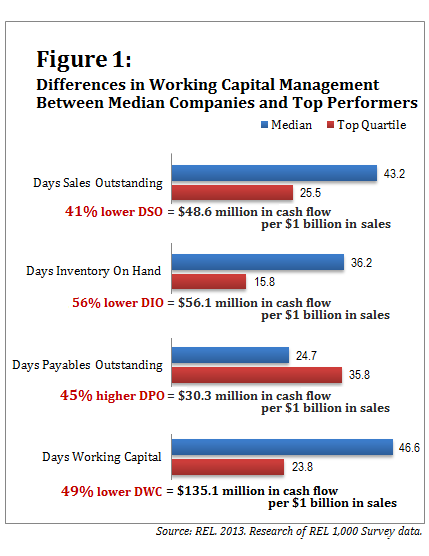

The results are astonishing. In aggregate, these companies have an opportunity to squeeze $285 billion out of accounts payable, $318 billion out of accounts receivable, and $459 billion out of inventory. So the 1,000 businesses in the study have an opportunity to free up a total of more than $1 trillion in cash by boosting their working capital management. As Figure 1 shows, companies in the top quartile have 49 percent less working capital tied up in operations than do the median performers in their industry, which translates into an additional $135.1 million in cash flow per $1 billion in sales. As borrowing becomes more difficult or even impossible for some companies, tightening working capital is a smart way to access cash.

Moving Forward, Eyeing the Past

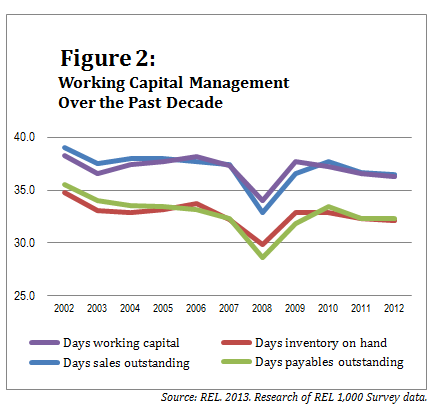

The results of REL's studies over the past decade show that working capital fell substantially during 2008 but has headed back up in the years since (see Figure 2, below). "In the recession, every number went down," Ginsberg says. "Revenue went down, profitability went down, costs went down, and working capital went down too. The reduction in working capital was a good thing, and it didn't happen by accident. Once companies reached stabilization, they were able to understand how to grow profitable revenue off a lower base of working capital. That means they were able to squeeze more profit out of every dollar they put into their business."

.png) Ginsberg allows that it sometimes make sense to let working capital slide a bit. For example, a small company that signs a major new customer might initially hold a bit more inventory than usual to keep that customer satisfied. "But decisions like that need to be made with an understanding of the trade-offs you have to make between customer satisfaction and profitability or whatever your objective for your cash is," Ginsberg says.

Ginsberg allows that it sometimes make sense to let working capital slide a bit. For example, a small company that signs a major new customer might initially hold a bit more inventory than usual to keep that customer satisfied. "But decisions like that need to be made with an understanding of the trade-offs you have to make between customer satisfaction and profitability or whatever your objective for your cash is," Ginsberg says.

While he doesn't advocate spending too much time looking backward at recession-era practices, Ginsberg does believe companies should take a basic lesson from the downturn: "You don't need to relax working capital management and suffer on the cash flow side in order to get profits," he says. "That's an enlightenment for a lot of companies. A lot of times, the culture will dictate 'It's a new paradigm, and we're doing things differently.' But that's not really true when it comes to things like customer payment terms, supplier terms, and maintaining delivery commitments you've made on the inventory side. Some things really haven't changed at the core of the business. We recommend taking a historical look at what your company can achieve."

The first step in analyzing a company's opportunities for improvement is to look at the root causes of deterioration in working capital performance. For example, Ginsberg says, "you might find your DSO has increased 20 percent since 2008. You have to find out why that is. There's a mechanical aspect to analyzing the numbers, but then you have to look at the business as well." It makes sense to ask questions like: Did we have any divestitures or acquisitions over the past five years? How has the absorption of any acquisitions affected our business? Does one business unit have better practices than another? Can we standardize working capital management across all our lines of business?

Setting Targets and Monitoring Metrics

According to the REL analysis, inventory is the area of working capital management that presents the most opportunity to free up cash—$459 billion total among the 1,000 companies in the study. "In 2009, companies started moving into growth mode," Ginsberg explains. "In growth mode, there tends to be a buildup of inventory, a replenishment of stock inventories and the creation of more inventory in raw materials and intermediate products. But a careful balance is required because you're making a forecast of customer demand, which is still volatile."

Achieving the right balance can be very difficult, according to Prathima Iddamsetty, senior manager with REL. "What we see in our practical experience with customers is that inventory is one of the hardest areas of working capital management to improve because it's very industry-specific," she says. "What works in one industry doesn't necessarily work in other industries. Figuring out the balance between what works best for operations and what sales wants, in addition to all the forecast inaccuracies based on demand volatility, is always a challenge."

Usually companies err on the side of caution and build up more inventory than they need because they don't want to risk being unable to fulfill a customer order, Iddamsetty says. "But in the long scheme of things, that's not the right attitude," she adds. "You have to think about the trade-offs between costs, profitability, keeping your machines running, and customer service. The trade-offs are harder to manage with inventory than with the other components of working capital."

To help clients get a handle on their inventory levels, REL asks them to concentrate their efforts on product range management, or management of the product mix they're offering to customers. "A lot of companies have big issues in determining which items they need to carry and how much demand there is for each of them," Iddamsetty says. "Everything starts with product range management; it affects how you're sourcing your raw material, how you're scheduling and manufacturing downstream, and whether you're achieving your objectives in profitability, customer satisfaction, and proper utilization of your assets. If you get the product mix right, everything works better downstream in terms of your supply chain management and inventory."

She recommends that companies divide their products into groups that make sense from the perspective of inventory metrics. Then they should measure the performance of each product group in terms of metrics such as turnover and DIO. "Our best practice is to biannually review your product range and how your product portfolio moves, then set your metrics accordingly," Iddamsetty says. "So halfway through the year, re-evaluate your working capital objectives. What you set at the beginning of the year won't necessarily still hold true by the midpoint of the year. Demand might change—your whole demand pattern could change—and hence your DIO targets should change."

For receivables, the most important metric is DSO, Ginsberg says. "But we recommend looking at operational-level metrics as well. For accounts receivable, these would measure the efficiency of the people sending invoices, doing billing and credit reviews and collections. You want to look at things like percentage current invoices—how many of the invoices outstanding right now are current vs. past due? And you want to look at your terms. Are you invoicing your customers appropriately and on time, and are customers paying within the agreed-upon term? If not, you need to look at metrics around disputes and customer service to understand why customers aren't paying on time."

For monitoring payables, Ginsberg recommends using DPO, as well as weighted average days to pay vs. weighted average terms—in other words, whether your payments are meeting contracts' terms. "You could also look at early vs. late payments," he adds. "For low-hanging fruit, you want to make sure you're not paying anybody early. But you also want to look at late payments. If you're paying late, you might be incurring penalties for that."

The Time Is Right

For companies that have let working capital management slide in the economic recovery, now is the time to restore the rigor they developed during the recession. Many businesses are still sitting on large amounts of cash; in fact, the companies in the REL/CFO study have four times as much cash on hand today as they had 12 years ago ($981 billion in 2012 vs. $219 billion in 2000). Nevertheless, the study found that companies' free cash flow—the amount of cash that a company is able to generate after laying out the money required to maintain or expand its asset base—is falling. That figure dropped 14 percent from 2011 to 2012. This means that although their cash on hand increased slightly last year, businesses have less cash available today for debt reduction, acquisitions, dividends, and new product launches than they had a year ago.

"Our study highlights the reasons why treasurers need to be thinking about working capital right now," Ginsberg concludes. "Their own operations are a great source of funding relative to the debt markets, where interest rates are going up."

——————

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Meg Waters

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.