On Monday, the Association for Financial Professionals issued its “2013 AFP Estimating and Applying Cost of Capital Survey Report.” The survey of 424 finance professionals found that although financial planning and analysis (FP&A) might be the department that makes the most use of weighted average cost of capital (WACC) figures, it is generally not the department responsible for coming up with WACC estimates. In 46 percent of respondents' companies, treasury is responsible for WACC calculations. This responsibility falls to finance in 32 percent of companies and to FP&A in only 18 percent.

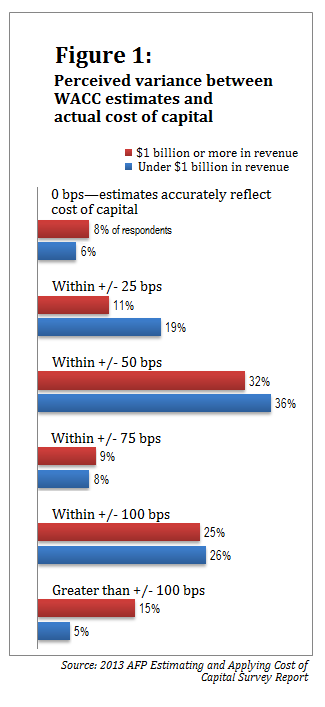

More than half of respondents think their organization's WACC estimate is within 50 basis points (bps) of its actual cost of capital, but 11 percent believe the WACC is off by more than 100 bps. Large companies are three times as likely to think their WACC calculations are more than 1 percentage point away from actual cost of capital (see Figure 1).

The survey delved into the calculations companies use to reach their WACC estimates. It found that the vast majority of companies (85 percent) use discounted cash flow (DCF) techniques to value their projects and investment opportunities; most of the remaining 15 percent of respondents use either projected return on investment (ROI) or a more generic means of cost-benefit analysis. Most DCF users (51 percent) discount explicit forecasted cash flows over the project's first five years. Twenty-six percent use a 10-year explicit cash flow forecast, only 3 percent use a 15-year forecast, and 12 percent use a three-year forecast.

Following their explicit discounted cash flow forecasting, respondents most commonly estimate the terminal or continuing value of the project or investment opportunity using a perpetuity growth model (42 percent). Thirty-seven percent use a long explicit cash flow forecast (most popular among smaller and privately held companies), and 15 percent use the value driver model.

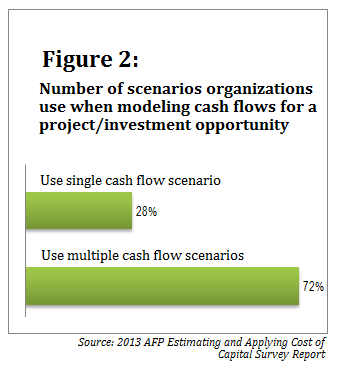

The survey also found that nearly three-quarters of respondents consider multiple scenarios (e.g., best-case, worst-case, and expected-case scenarios) when modeling cash flows for projects and investment opportunities (see Figure 2).

The survey also explored how companies estimate their cost of equity. Eighty-five percent of respondents use the Capital Asset Pricing Model (CAPM); only 4 percent use the Dividend Discount Model (DDM), and 2 percent use the Arbitrage Pricing Model (APM).

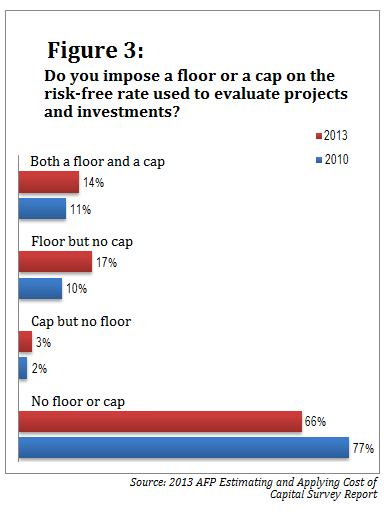

Among those that use the CAPM, the most popular instrument used in estimating risk-free rates is the 10-year Treasury (39 percent), followed by 90-day Treasuries (17 percent), 5-year Treasuries (14 percent), and 52-week Treasuries (12 percent). An increasing number of companies are imposing a floor, a cap, or both on the risk-free rate they use in evaluating projects and investments (see Figure 3). Among these, the average floor for the risk-free interest rate is 4 percent. The average rate cap is 8 percent, although the average among companies with less than $1 billion in annual revenue is 10 percent and the average among larger companies is 7 percent.

To determine the beta factor in estimating their cost of equity, nearly two-thirds of companies use Bloomberg data. Half use a raw beta factor, while the other half use an adjusted beta factor. This is a notable shift toward using raw beta; in 2010, considerably more respondents used adjusted beta (57 percent).

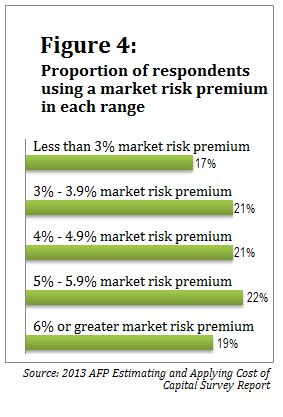

When asked about the market risk premium they use to determine expectations for return on an equity portfolio, roughly equal numbers use a premium of less than 3 percent, a premium of 6 percent or higher, and each full percentage in between the two (see Figure 4). The most common frequency of re-evaluating the market risk premium is once a year (36 percent of respondents), although 19 percent re-evaluate on a quarterly basis and 23 percent reconsider their market risk premium every time they estimate their cost of equity.

In figuring the cost-of-debt component of their WACC, 43 percent of respondents' companies use the current rate on their outstanding debt, 21 percent use the forecasted rate for new debt issuance, 21 percent use an average rate on outstanding debt over a defined period of time, and 12 percent use the historical rate on outstanding debt. The survey also inquired about which tax rate respondents use when calculating the after-tax cost of debt. Almost two-thirds (60 percent) use the effective tax rate, while more than a quarter (27 percent) use the marginal tax rate.

How do companies pull together all these calculations to determine their WACC? In establishing the relative weighting of debt and equity, 36 percent use their current book debt-to-equity ratio. Seventeen percent use their current book debt but use market values for the equity portion of the ratio. Twenty-four percent use their current market debt-to-equity ratio, while 18 percent use their target debt-to-equity ratio.

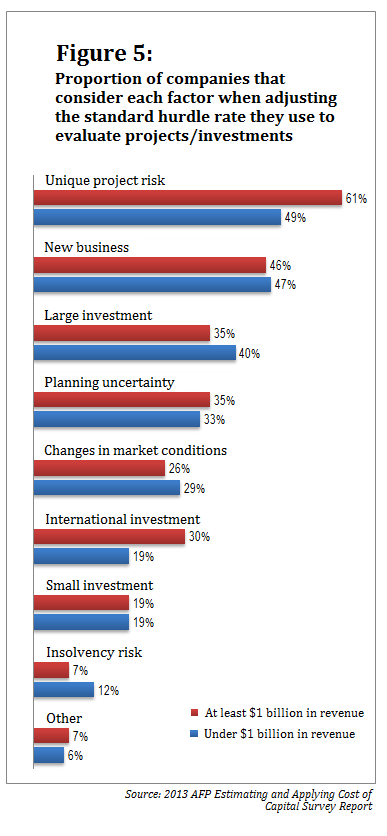

Ultimately, when determining whether to fund a specific project, 48 percent of large companies and 32 percent of smaller businesses use a standard hurdle rate above the WACC. Then many adjust the hurdle rate when characteristics of the project indicate that doing so is appropriate (see Figure 5).

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

s")