Last month, Chatham Financial released a benchmarking report on the state of financial risk management among U.S.-based businesses. Chatham studied the Securities and Exchange Commission (SEC) filings of more than 1,000 public companies with annual revenues between $500 million and $20 billion, excluding financial services and insurance companies, to determine how many of these organizations incur currency, commodity, and interest rate risks, and how they mitigate those risks.

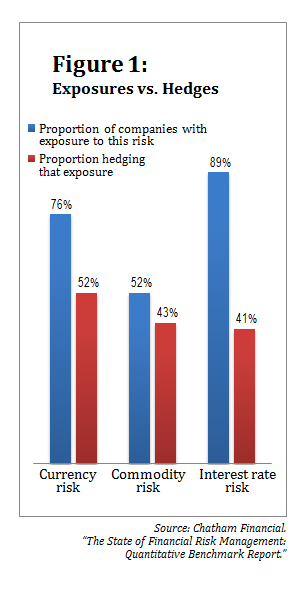

Many of these organizations have experienced a significant increase in financial risks over the past decade, as they've extended their operations abroad and as volatility has increased in global financial markets. Nevertheless, Chatham found that many companies with foreign exchange, interest rate, and/or commodity risks on their financial statements are not using derivatives to hedge these risks (see Figure 1).

About half of organizations that have currency risk are hedging their exposure; the Chatham report notes that this is “a surprisingly low percentage given the extreme volatility around the currencies to which the companies have exposure.” The majority of companies that are hedging foreign exchange (FX) risk are using both balance sheet and cash flow hedges.

Among the companies that Chatham found to have commodity risk, even fewer are using derivatives to hedge it. Commodity hedging is much more prevalent in industries where commodity risk is core to the business model—including natural resources and mining, transportation and utilities, and manufacturing. Larger companies are also much more likely to hedge commodity risks. From the combination of these factors, Chatham concludes: “Given the complexity of hedging commodities in the financial markets, it appears as though only sufficiently sophisticated corporations with commodities as a core exposure have a tendency to hedge in this manner.”

Finally, interest rate risk—from credit agreements, asset-backed loans, bonds, etc.—is a concern for 89 percent of the companies whose financial statements Chatham studied. However, only 41 percent of those businesses hedge their interest rate risk using derivatives. This is partly explained by companies' ability to mitigate some of the risk by issuing a combination of debt with fixed interest rates and debt with floating rates.

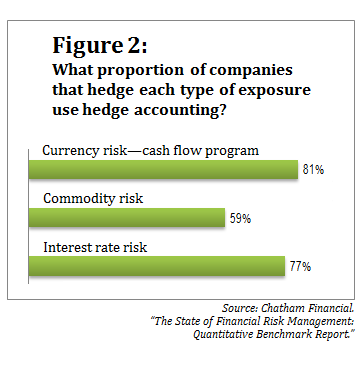

Most companies that hedge risks in each financial-risk category use hedge accounting under ASC 815 (formerly FAS 133), but hedge accounting is by no means universal. Figure 2 shows the breakdown, including for currency risk only cash flow hedging programs, as balance sheet programs generally don't require the use of hedge accounting.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Forfeiture Suit Gets Dismissed")