The European Market Infrastructure Regulation (EMIR) deadline for reporting derivatives trades is looming large. Tomorrow—February 12, 2014—all parties involved in derivatives transactions in Europe must begin reporting the transactions to trade repositories on a daily basis. EMIR covers a wide range of transactions, including foreign exchange (FX), interest rate, commodity, credit, and equity derivatives, as well as some instruments Dodd-Frank doesn't cover, such as FX forwards. And the rule applies to both financial institutions and their corporate clients.

“Buy-side firms will be deeply impacted by the arrival of EMIR, as the onus to report derivatives trades will be shared by both the sell-side and the buy-side,” says Rob Friend, global head of fixed income product for Bloomberg. “This will have a significant impact on their business processes, operations, and returns for their investors.” In fact, Anthony Kirby, executive director and head of regulatory reform for capital markets and asset management in the risk and regulation division of EY's financial services practice, has estimated that the costs associated with EMIR reporting could, at the extreme end of the spectrum, add two to three basis points to asset managers' cost-income ratios over the next few years.

“That's a main difference between Dodd-Frank and EMIR—that under EMIR both sides have to report their transactions,” emphasizes Guenther Peer, regional vice president, solutions consulting EMEA, for treasury and risk management software vendor Reval. “Intragroup transactions also have to be reported. If a U.S. multinational is trading with a European bank, there's not too much that needs to happen because the bank is going to report their side of the trade. But if a U.S. corporate has a subsidiary based in the EU [European Union], then the subsidiary needs to comply with EMIR.”

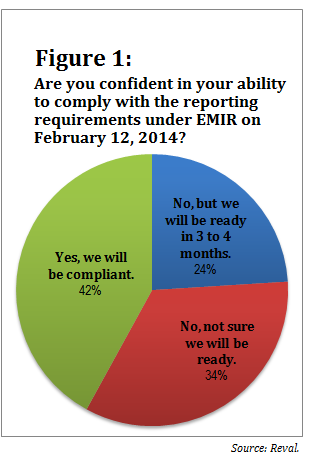

A poll conducted two weeks ago by Reval indicates that many organizations are not yet ready to do so. When asked whether they were confident that they'd be able to comply with EMIR's reporting requirements by tomorrow's deadline, only 42 percent of respondents said yes. (See Figure 1.)

A poll conducted two weeks ago by Reval indicates that many organizations are not yet ready to do so. When asked whether they were confident that they'd be able to comply with EMIR's reporting requirements by tomorrow's deadline, only 42 percent of respondents said yes. (See Figure 1.)

In response to another question in the same poll, about a third (32 percent) said they plan to do their own reporting to trade repositories. Nearly as many (28 percent) said they plan to contract with third parties to report on their behalf. But just two weeks ago, 40 percent said that they hadn't yet decided how they would convey information on their trades to the trade repositories.

“The EMIR timelines were pretty dense,” Peer says. “There was a very narrow window for trade repositories, financial institutions, and corporates to get ready. I think a lot of organizations have been working furiously, but they're still fine-tuning their processes.”

Nevertheless, Peer believes that the 65 percent of respondents in Reval's poll who said they expect a delay in implementation of the reporting requirements will be disappointed. “Local regulators are saying they're probably not going to fine for noncompliance on day one,” he says. “At the same time, they have made two things crystal clear: First, there's not going to be any relief, nor will they delay the deadline. And second, corporates need to be trying to comply. If they don't have the last field in their reports by tomorrow, that should be OK. At least, that's what the rumors suggest. But they can't simply sit back and expect to avoid scrutiny.”

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.