CFOs, treasurers, analysts, and other financial management decision-makers have made in-roads in mitigating risk by increasing restrictions on which banks can hold their uninsured deposits and updating their investment policies frequently. But despite progress in both understanding and managing counterparty risk, many organizations still do not appear to have formal counterparty risk exposure policies or frameworks in place, nor do they appear to be able to adequately aggregate, analyze, and monitor their counterparty exposures.

CFOs, treasurers, analysts, and other financial management decision-makers have made in-roads in mitigating risk by increasing restrictions on which banks can hold their uninsured deposits and updating their investment policies frequently. But despite progress in both understanding and managing counterparty risk, many organizations still do not appear to have formal counterparty risk exposure policies or frameworks in place, nor do they appear to be able to adequately aggregate, analyze, and monitor their counterparty exposures.

These were two of the major findings revealed in the fourth annual Liquidity Risk Survey, a study of short-term investment, debt, and forecasting practices conducted by Capital Advisors Group, Inc. and Strategic Treasurer LLC. The 2014 survey, the results of which were released in May, elicited responses from 112 treasury and finance professionals, including CFOs, treasurers, assistant treasurers, vice presidents of finance/treasury, managers or directors of cash investments, treasury/cash managers, and treasury/cash analysts. Respondents spanned companies ranging in size from over $10 billion in annual revenue (21 percent) to those with less than $500 million (29 percent).

Progress in Some Areas of Risk Mitigation

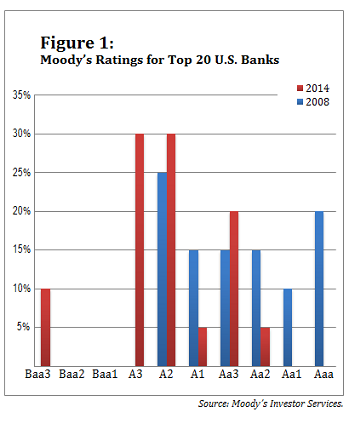

Bank ratings have declined significantly since the financial crisis. In 2008, 60 percent of the top 20 U.S. banks received Moody's ratings of Aa3 or better. This year, only 25 percent rank that high. Similarly, in 2008 Moody's didn't rate any of the top U.S. banks at A3 or below, whereas today 40 percent fall into that range. (See Figure 1, below.)

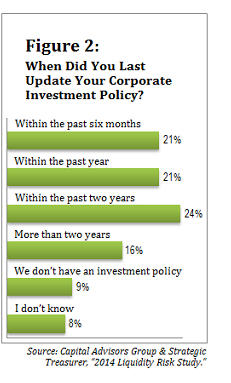

Perhaps in response, treasury and finance professionals appear to have continued the practice of paying close attention to risk in their investment portfolio. A half-decade after the peak of the financial crisis, survey respondents in 2014 report that their company is regularly reviewing and revising its investment policy. Forty-two percent said they have updated their corporate investment policies during the past year—half of those within the six months prior to the survey—and two-thirds said they've updated their policies within the past two years (see Figure 2 on page 2).

Perhaps in response, treasury and finance professionals appear to have continued the practice of paying close attention to risk in their investment portfolio. A half-decade after the peak of the financial crisis, survey respondents in 2014 report that their company is regularly reviewing and revising its investment policy. Forty-two percent said they have updated their corporate investment policies during the past year—half of those within the six months prior to the survey—and two-thirds said they've updated their policies within the past two years (see Figure 2 on page 2).

The content of those policies reflects heightened counterparty concerns. One-third of respondents said their company requires a minimum credit rating of AA- or better on uninsured bank deposits, up 9 percentage points (38 percent) in just the past year. Interestingly, the proportion of companies in which investment policies do not specify a minimum counterparty credit rating for banks holding uninsured deposits—or set a minimum credit rating of BBB+ or below—also increased 9 percentage points, from 26 percent in 2013 to 35 percent in 2014. This sub-trend bears monitoring in future surveys.

Ongoing concerns about the health of the global banking and financial system underscore the wisdom of taking measures to mitigate counterparty risks. Companies face exposures from multiple sources, including (but not limited to) bank deposit balances, money market fund holdings, separately managed account holdings, lines of credit, foreign exchange contracts, and vendor and customer accounts. Some businesses seem to be implementing strategies to mitigate risks across counterparties in a comprehensive way. Unfortunately, few organizations appear to have yet reached that level of sophistication in their risk management practices.

Ongoing concerns about the health of the global banking and financial system underscore the wisdom of taking measures to mitigate counterparty risks. Companies face exposures from multiple sources, including (but not limited to) bank deposit balances, money market fund holdings, separately managed account holdings, lines of credit, foreign exchange contracts, and vendor and customer accounts. Some businesses seem to be implementing strategies to mitigate risks across counterparties in a comprehensive way. Unfortunately, few organizations appear to have yet reached that level of sophistication in their risk management practices.

Major Hurdles Remain

Counterparty risk management and mitigation appear to continue to pose major challenges for the average corporation's treasury and finance teams. Results of our 2014 survey indicate that many companies lack formal policies for managing counterparty risk, and they lack techniques for accurately calibrating that risk.

For one thing, organizations seem to be having difficulty compiling a companywide view of risks. When survey respondents were asked to identify their company's most urgent need in the realm of counterparty risk management, 19 percent selected aggregation of risk exposures. Another 18 percent identified knowledge, transparency, and visibility as their most crucial concern.

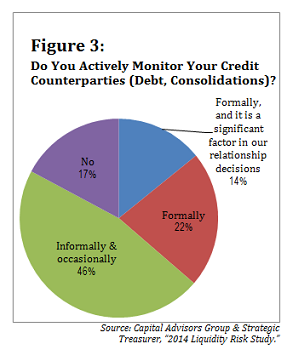

Another problem may be that there are critical gaps in many companies' processes for formally monitoring counterparty risk. For example, only 36 percent of companies surveyed said that they formally monitor credit counterparties with respect to debt. Moreover, only 14 percent view counterparty risk as a significant factor in their debt decisions, which represents a sharp contrast to the pervasive implementation and ongoing revision of their investment policies (see Figure 3).

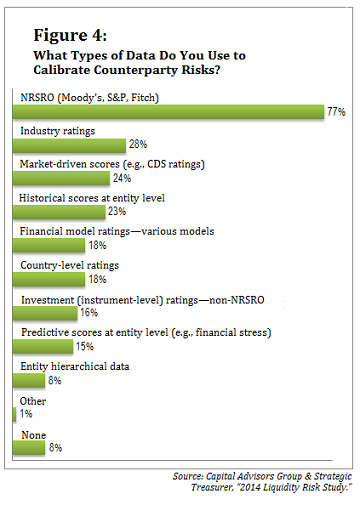

The techniques companies are using to calibrate counterparty risk raise yet another issue: Survey respondents appear to be using a limited set of variables to calculate the risks they face. More than three-quarters of respondents use data from nationally recognized statistical ratings organizations (NRSRO) like Moody's, Fitch Ratings, and Standard & Poor's to calibrate counterparty risks. Some also use industry ratings and market data, such as credit default swap (CDS) levels, in assessing counterparty risk—but those proportions are much lower (see Figure 4, on page 3.). Given the conflict of interest that arises because issuers pay the ratings agencies, using ratings data alone may be insufficient for gauging risk. It's important to pull together data from multiple sources and internally generate credit risk ratings. Independent multifactorial models that incorporate qualitative and quantitative variables may provide a clearer and more holistic view of risk, allowing finance and treasury professionals to more effectively limit and manage counterparty risk.

A Buyer's Market in Debt

The survey also revealed ways in which companies are shifting their approach to debt management, likely with the goal of minimizing their exposure to possible changes in debt markets. A reduction in the number of loan covenants, along with the possibility that interest rates will increase in the near future, may help to explain why 64 percent of survey respondents said their company has negotiated or renegotiated credit facilities in the past year, up from 56 percent in last year's survey. Twenty-eight percent of organizations had fewer loan covenants than the last time they negotiated debt agreements.

Additionally, 75 percent of organizations reported that their debt has more than one maturity date or that they have intentionally tried to stagger debt maturity dates, compared with just 58 percent in 2013. This shift suggests that organizations may be using multiple maturity dates to guard against unfavorable terms at the time of refinancing or to reduce the impact on their business if the debt markets freeze up at an inopportune time. The strong pace of credit facility negotiation and renegotiation is likely to continue as long as loans have fewer covenants and interest rates stay low. However, looming interest rate increases may impact the current buyer's market for debt by the time we conduct our 2015 survey.

This year's Liquidity Risk Survey shows a clear trend toward improvement in certain risk mitigation practices, and we expect that trend to continue into 2015. Last year, our survey indicated a complacency toward bank exposures, while this year's survey revealed that over the past year companies have taken meaningful steps to mitigate risk, including placing limits on uninsured bank deposits.

Yet this year's survey suggests that companies remain complacent toward counterparty risk management. Many practitioners appear to still lack appropriate frameworks for aggregating, assessing, and monitoring counterparty risk. They seem to be relying on limited data and credit ratings that may not enable them to truly grasp risk trends. We're hopeful that our 2015 survey provides better news about the adoption and maturation of corporate counterparty risk management metrics and tools.

——————————————————-

Benjamin K. Campbell is the founder and chief executive officer of Capital Advisors Group, Inc., which is an independent investment advisor specializing in institutional cash investments, credit and counterparty risk management, and debt financing. He has been named one of the “100 Most Influential People in Finance” by Treasury & Risk. Email him at [email protected].

Benjamin K. Campbell is the founder and chief executive officer of Capital Advisors Group, Inc., which is an independent investment advisor specializing in institutional cash investments, credit and counterparty risk management, and debt financing. He has been named one of the “100 Most Influential People in Finance” by Treasury & Risk. Email him at [email protected].

Craig A. Jeffery is the founder and managing partner of Strategic Treasurer, LLC, which provides corporate, educational, and government entities with direct access to comprehensive and current assistance with their treasury and financial process needs. He is the author of a book for treasury, “The Strategic Treasurer: A Partnership for Corporate Growth.” You can contact him at [email protected].

Craig A. Jeffery is the founder and managing partner of Strategic Treasurer, LLC, which provides corporate, educational, and government entities with direct access to comprehensive and current assistance with their treasury and financial process needs. He is the author of a book for treasury, “The Strategic Treasurer: A Partnership for Corporate Growth.” You can contact him at [email protected].

A webinar presenting this survey in full, hosted by Ben Campbell and Craig Jeffery, was held on May 6, 2014. An on-demand rebroadcast is available at www.capitaladvisors.com.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.