![]() Although four out of five companies have taken measures to address bribery and corruption risks, they're not making much progress in eliminating these dangers to their business. That's the key takeaway from the “13th Global Fraud Survey” that EY released last week. The poll was conducted from November 2013 to February 2014; it entailed interviews by a global research firm with 2,719 senior decision-makers in large companies across 59 countries and territories. Respondents were primarily CFOs, chief compliance officers (CCOs), general counsel, and heads of internal audit.

Although four out of five companies have taken measures to address bribery and corruption risks, they're not making much progress in eliminating these dangers to their business. That's the key takeaway from the “13th Global Fraud Survey” that EY released last week. The poll was conducted from November 2013 to February 2014; it entailed interviews by a global research firm with 2,719 senior decision-makers in large companies across 59 countries and territories. Respondents were primarily CFOs, chief compliance officers (CCOs), general counsel, and heads of internal audit.

Among these respondents, 82 percent said their company has an anti-bribery and corruption (ABAC) policy and code of conduct. Even more (83 percent) said senior management has “strongly communicated” its commitment to ABAC policies. Almost three-quarters (73 percent) said there are clear penalties for violating their company's ABAC policies, and 35 percent said people have been penalized for breaching the company's policies.

Nevertheless, 39 percent of all respondents—and 54 percent of those who work in emerging markets—said bribery and/or corrupt practices happen widely in business in their country. This perception is virtually unchanged from the 2012 EY survey, in which 38 percent of all respondents, and 56 percent in emerging markets, said bribery and corruption are widespread in their country.

Ten percent of C-suite survey participants said they have been asked to pay a bribe in a business situation, and twice that many CEOs have faced pressure to engage in bribery. The corruption problem is biggest in Egypt, Kenya, and Nigeria. But 40 percent of the countries included in the survey were fingered by more than half of their residents as having widespread corruption.

Bribery is not the only ethics challenge that companies face. Six percent of all respondents said that misstating financial performance can be justifiable if doing so helps the business survive an economic downturn. In certain locales, that proportion is much higher: 28 percent in Singapore, 24 percent in India, and 10 percent in South Africa. Not only that, but 7 percent of CFOs and other finance professionals think performance misstatements can be justified—as do 11 percent of CEOs.

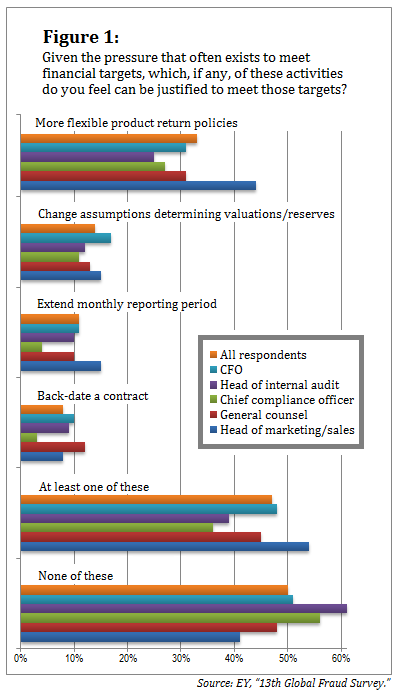

Ten percent of CFOs think back-dating a contract can be justified if it helps the company meet financial targets. Eleven percent are OK with extending the monthly reporting period, 17 percent with changing assumptions used to determine valuations or reserves, and 31 percent with increasing the flexibility of product-return policies. Only half of CFOs (51 percent) don't think any of these actions are justifiable when the company is falling short of performance goals. (See Figure 1, below.)

“While boards often set a zero-tolerance tone and encourage management to build teams to address the risks of bribery and corruption, our experience tells us that ongoing oversight from the board is essential if the risks are to be more effectively mitigated,” EY states in the survey write-up. “Our results show that in companies where the leadership is most engaged and demanding, there is a higher level of compliance activity across the firm. It is essential that the board sets a challenging plan, continues to ask tough questions, and actively holds senior management accountable for the results.”

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.