The largest U.S. banks, flooded with requests for loans from blue-chip companies in recent weeks, are starting to use their newfound leverage over corporate America to insert safer, more favorable terms into billions of dollars of deals.

Anti–cash-hoarding stipulations, interest-rate floors, and mandatory prepayment clauses—provisions more commonly found in junk-rated transactions or bridge loans—are creeping into investment-grade financings as demand outstrips how much Wall Street is willing to lend. Banks are even starting to increase the rates some companies such as General Motors Co. have to pay, a rarity in a market where borrowing costs have largely been on a one-way track lower since the last financial crisis.

The changes underscore the shifting power dynamics in a business where, under normal circumstances, banks would often seek to undercut one another to provide cheap lines of credit—part of an effort to secure relationships with clients whom they hope will stick around for more expensive needs. Now, as the surge of borrowers tapping existing revolvers threatens to dent profitability and bankers seek to conserve liquidity for those that need it most, they're starting to push companies to make concessions.

"Banks have been met with a wall of requests for liquidity from their clients," said Robert Smalley, a credit-desk analyst at UBS Group AG. "They want to ensure that they can provide that liquidity on a timely basis, and they want to do it at the right price."

The concessions largely apply to new financings, where banks have more recourse to dictate terms. They stand in contrast to the waivers some borrowers—especially riskier ones—have recently been able to extract on existing loans from lenders worried about triggering defaults.

Many of the new provisions can be found in loans to companies near the bottom of the investment-grade ladder, or in industries directly affected by the coronavirus outbreak. While the exact clauses attached to transactions depend heavily on borrowers' specific circumstances, the fact they're making their way into new loans at all shows just how much the market has changed in recent weeks, industry watchers say.

Representatives for JPMorgan Chase & Co., Bank of America Corp., and Citigroup Inc., among the biggest lenders in the business, declined to comment. Wells Fargo & Co., another large player, said it's committed to helping clients but wouldn't comment on specific deals.

Details on the New Restrictions

Among the most novel changes popping up in new deals are anti–cash-hoarding measures designed to ensure companies don't tap revolving credit facilities until they actually have a need for the funds.

That's been a growing frustration among bankers over the past month and a half, as lending desks stretched to the limits operationally have been inundated with drawdown requests.

In the case of Valero Energy Corp.'s recent $875 million one-year revolver, the stipulation limits access to the funds to working capital needs, according to a company filing. A provision in a new credit facility for healthcare supplier Henry Schein Inc. prevents the company from exceeding a certain cash balance. Similar clauses are expected in other upcoming short-term loans currently in discussion, according to people with knowledge of the deals.

That's not the only protection starting to appear.

Interest guarantees for lenders, known as LIBOR floors, are more often associated with leveraged loans, but are increasingly turning up in blue-chip deals. Caterpillar Inc., DuPont Inc., and Mohawk Industries Inc. brought new transactions in recent weeks with safeguards of 0.75 percent.

Zero-percent floors, or no floors at all, have traditionally been the norm in the investment-grade loan business. But after the Federal Reserve cut rates below 0.25 percent in response to the Covid-19 pandemic, banks are seeking protections that guarantee minimum payouts, especially as their funding costs increase.

Mandatory prepayment clauses—provisions that ensure banks are the first to be paid back when companies regain access to the bond market—are also being added onto some deals.

The stipulation, typically associated with short-term bridge financing used for acquisitions, was part of Pioneer Natural Resources Co.'s $905 million revolver earlier this month, according to a company filing.

Loans Are Also Getting Pricier

While demand for bank financing has eased in recent weeks, as capital markets opened up to companies with less-pristine balance sheets, it nonetheless remains robust.

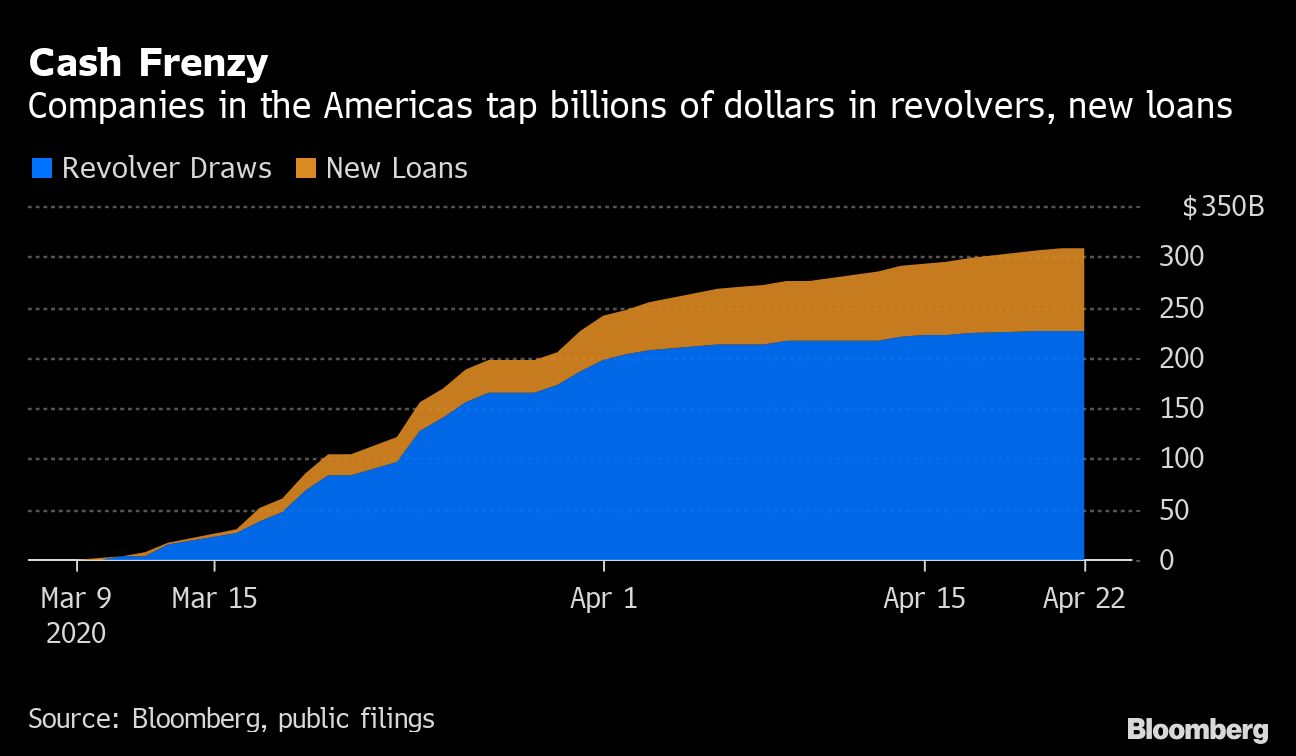

Across all credit ratings, corporations in the Americas have drawn $226 billion from revolving facilities and received $82 billion in new revolvers and term loans since March 9, according to data compiled by Bloomberg. That's allowed banks to simply charge some companies more to borrow.

General Motors earlier this month had to pay an extra 50 basis points to refinance part of its $16.5 billion revolver. GM's cost of funds was still relatively cheap compared with the rate on some of its similar-maturity bonds, but the increase—a product of the greater macro volatility and the mounting stress on the auto sector in particular—reflects the growing power of banks to dictate terms.

"When you get late into credit cycles, everything goes in favor of the borrowers—until it doesn't," said Noel Hebert, director of credit research at Bloomberg Intelligence.

—With assistance from Marcus Lefkandinos and Lara Wieczezynski.

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.