As Donald Trump ramps up efforts to control the Federal Reserve, investors worry he’ll use central bank tools to fix something that’s not supposed to be a central bank problem: America’s ballooning debt. Trump said Tuesday he’s ready for a legal fight over his attempt to oust Fed Governor Lisa Cook and he’s looking forward to having “a majority” on the central bank’s board. That could advance the president’s campaign for lower interest rates, which he says will save the country “hundreds of billions.”

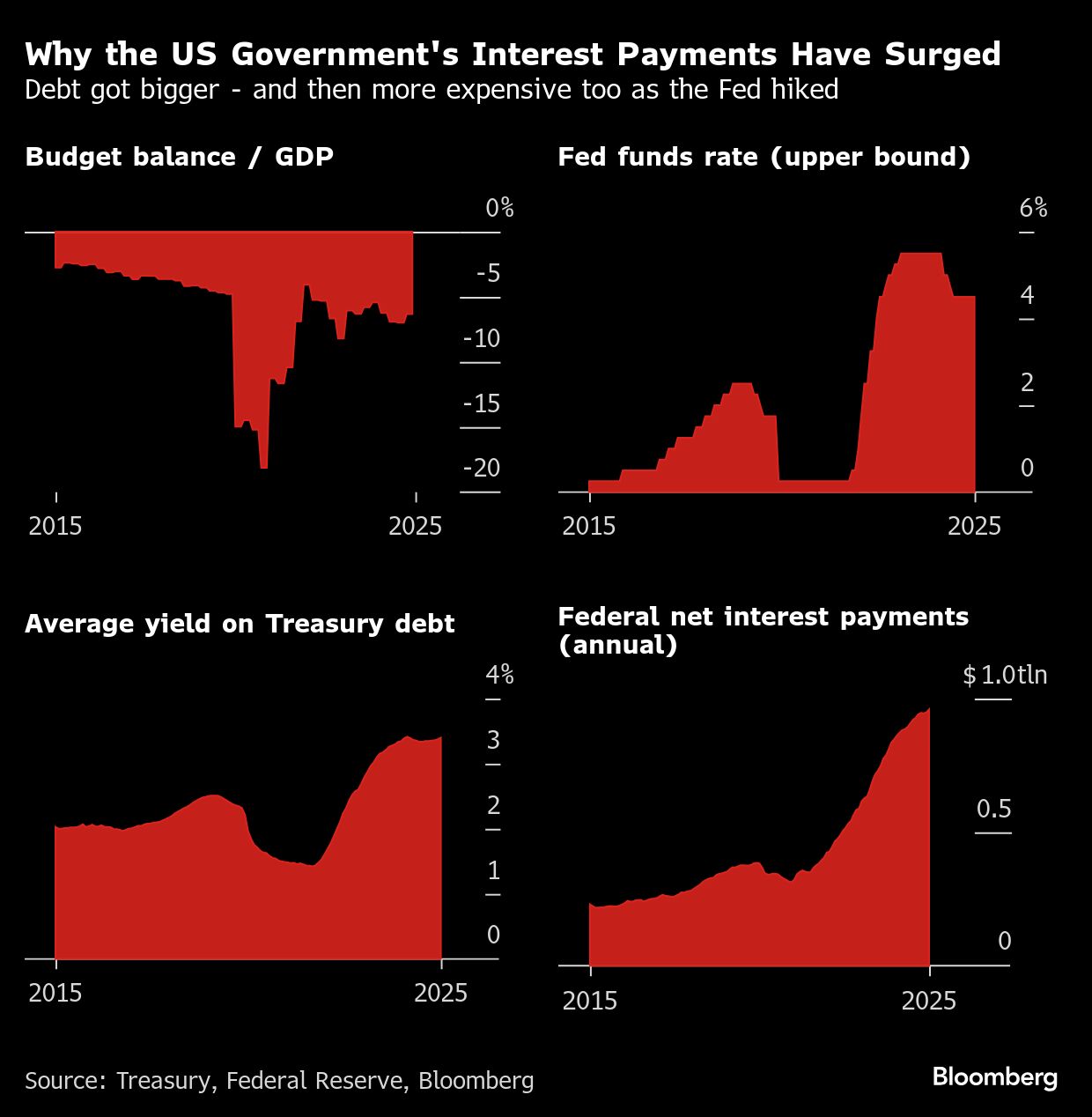

There are two main reasons why the government’s debt costs have soared lately: bigger budget deficits and higher interest rates. Most economists say the solution lies in borrowing less, via some combination of lower spending and higher taxes, rather than leaning on the Fed to make borrowing cheaper. That latter path is dangerous for central bankers who are tasked with keeping a lid on inflation—a task made harder when politicians juice the economy by pumping in money. Inflation could become not just difficult but impossible to control if interest rates—the main lever for curbing price pressures—were to turn into a tool for keeping the government solvent instead.

The term economists use for this kind of scenario is “fiscal dominance.” It’s typically associated with emerging-market nations, where monetary policy is subject to political pressure. As Trump’s campaign against the Fed escalates, many analysts see the United States sliding in a similar direction.

Eric Leeper, an economics professor at the University of Virginia, reckons we’re already there. “Ultimately, it’s fiscal policy that needs to be in place in the right way if you’re going to keep inflation under control,” says Leeper, a former Fed economist. Instead, “what we hear is, ‘We need lower interest rates because interest payments are exploding,’” he says. “It’s admitting that fiscal policy is not going to take care of itself, and so they’re trying to find some other way out. This is fiscal dominance.”

To be sure, many investors and economists who are worried about such risks wouldn’t go that far. There’s no sign that interest rate decisions have yet been swayed by the state of U.S. public finances. To tame post-Covid inflation, Fed officials enacted the sharpest interest rate hikes since the 1980s, even though that added hundreds of billions of dollars in debt costs to the budget.

This year, as the Fed held rates steady amid concern about tariff-driven inflation, Chair Jerome Powell has insisted that the Fed is basing its policy solely on the economic outlook, a point he reiterated at the Fed conference in Jackson Hole, Wyoming, last week. Powell has often said U.S. debt is on an unsustainable path. But he told reporters last month that it “wouldn’t be good” to consider the government’s fiscal needs in setting Fed policy, adding that “no advanced-economy central bank does that.”

Still, there’s mounting concern that the Fed might end up doing precisely that. Trump will pick a successor to Powell, whose term as chair ends next May. The president already named his economic adviser Stephen Miran to fill one vacancy on the Fed board, and he will create another opening if his attempt to fire Cook over alleged financial misconduct is successful. His team is hinting at a wider overhaul and looking for ways to exert more influence over the Fed’s 12 regional banks. Behind all this is a steady drumbeat of demands for lower rates.

“The Fed is now subject to intensifying fiscal dominance risks,” George Saravelos, global head of FX research at Deutsche Bank AG, wrote in a report on Tuesday. “What is a bigger surprise to us is that the market is not more concerned.” Thirty-year Treasury bonds and the dollar both posted declines on Tuesday as Trump pressed ahead with his bid to oust Cook. However, both are still trading well above the lows reached earlier this year amid concern over U.S. trade and budget plans.

Fears of a shift in the Fed’s focus would undermine the greenback and lift bond yields, while potentially generating interest in cryptocurrencies and gold as alternatives, according to Steve Barrow, head of G-10 strategy at Standard Bank in London. More than half of fund managers in a recent Bank of America Corp. poll said they expect the next Fed chair to resort to quantitative easing or yield curve control—policies that involve buying government bonds to cap borrowing costs—in order to ease the U.S. debt burden.

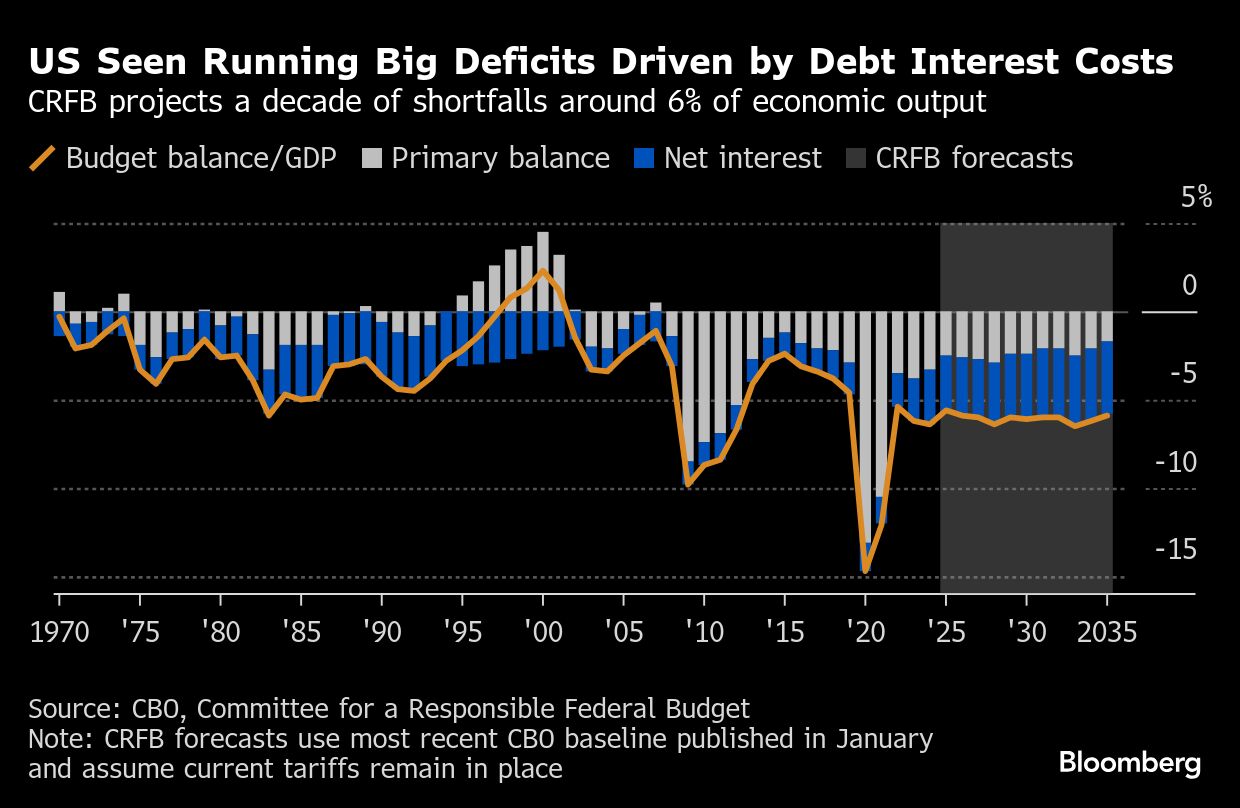

6% Annual Deficits Driving U.S. Toward Record Peacetime Debt Above 100% of GDP

Even as they browbeat the Fed, Trump and his allies have floated other ways to nudge down the government’s debt expenses. A proposed tweak to bank capital rules could boost demand for Treasuries, lowering yields. So could the new law to regulate stablecoins, which mandates that issuers back them with safe assets like government debt. There’s also talk of eking out some savings by issuing more short-term bonds. Republican Senator Ted Cruz has drafted legislation to bar the Fed from paying interest on reserves, touting the fiscal benefits it would bring.

All these ideas are indicators that budget pressures are increasingly shaping policy, according to David Beckworth, senior research fellow at the Mercatus Center at George Mason University. “We’re not at the textbook definition of fiscal dominance, but we’re getting closer,” he says. “I’d say we’re on that spectrum.”

As for the budget itself, Trump pushed a tax-cut and spending bill through Congress this summer that’s forecast to add $3.4 trillion to deficits over a decade. He’s also created a new revenue stream via his large tax hikes on imports. Add those up and it’s essentially a wash, S&P Global concluded. “Although fiscal deficit outcomes won’t meaningfully improve, we don’t project a persistent deterioration,” the credit rating company wrote. S&P predicts budget shortfalls of around 6 percent of GDP through the end of Trump’s term, roughly in line with other forecasters. That’s smaller than in the Covid aftermath but still large by historical standards—and double the 3 percent target set by Treasury Secretary Scott Bessent.

That leaves the U.S. national debt on track for a peacetime record above 100 percent of GDP. It’s built up under governments of both political parties, the result of rescue efforts during the Global Financial Crisis and the pandemic, coupled with a reluctance among most politicians to either raise taxes or trim major budget items such as social welfare and defense.

When governments run deficits, they typically finance the extra spending by issuing more bonds. That’s where central banks come into play. In crisis periods, they can step in to buy the debt themselves. Even in normal times, they set the short-term interest rates that influence the cost of longer-term sovereign debt. However, the two don’t always move in tandem. “No matter what the administration in any country may desire, in the end interest rates are set by markets,” said Fabio Natalucci, head of the Andersen Institute for Finance and Economics. “Especially at the long end of the curve.”

One recent example: When the Fed was easing monetary policy late last year, yields on 10-year and 30-year Treasuries actually rose, partly on concerns that bigger budget deficits after November’s election would rekindle inflation. That episode is a reminder that the Fed can’t automatically deliver cheaper government borrowing—and also that rising public debt can cause problems for central bankers, who want bond markets to be responsive to their moves.

Atlanta Fed President Raphael Bostic made this point in July, arguing that monetary policy could become less effective if investors are worried about fiscal risk. “You could see interest rates move to some extent independent of things that we do,” he said. “That would be really something that we’d have to think hard about.”

Who Will Blink First in This Game of Chicken?

There’s nothing unusual about fiscal and monetary policies pointing in opposite directions. What can be dangerous is if both sides keep pushing and neither is ready to give in. “I think of this as a game of chicken,” says George Hall, a professor at Brandeis University and former economist at the Chicago Fed. “Who blinks first? Is it going to be the Federal Reserve, or is it going to be Congress and the president?”

Central banks need to win any such game of chicken to maintain their credibility as inflation fighters, even if that means keeping rates high enough to make budget strains worse. If they lose, monetary policy will fall into a state of fiscal dominance, in which monetary policy becomes a tool of debt management and inflation targets get watered down or even abandoned. None of which applies in the U.S. right now. Nor is there any sign of the kind of economic emergency that’s tipped some countries into fiscal dominance in the past.

Instead, the concern is a political one—that pressure on the Fed is “opening the door” to that kind of regime—according to Dario Perkins, an economist at TS Lombard in London. “Every week, Trump says very clearly that these high interest rates are costing the government money,” he said. “It’s very clearly linked to debt problems rather than the inflation issue.”

————————————————————

Copyright 2025 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.