The logo “AI” is displayed during the ninth edition of the VivaTech show at Parc des Expositions Porte de Versailles, in Paris, on June 11, 2025. (Photo by Chesnot/Getty Images)

The logo “AI” is displayed during the ninth edition of the VivaTech show at Parc des Expositions Porte de Versailles, in Paris, on June 11, 2025. (Photo by Chesnot/Getty Images)

Wall Street is gearing up to lend massive amounts of money to the biggest players in artificial intelligence (AI)—and simultaneously trying to figure out how to protect itself from any bubble that its financing may be helping to inflate.

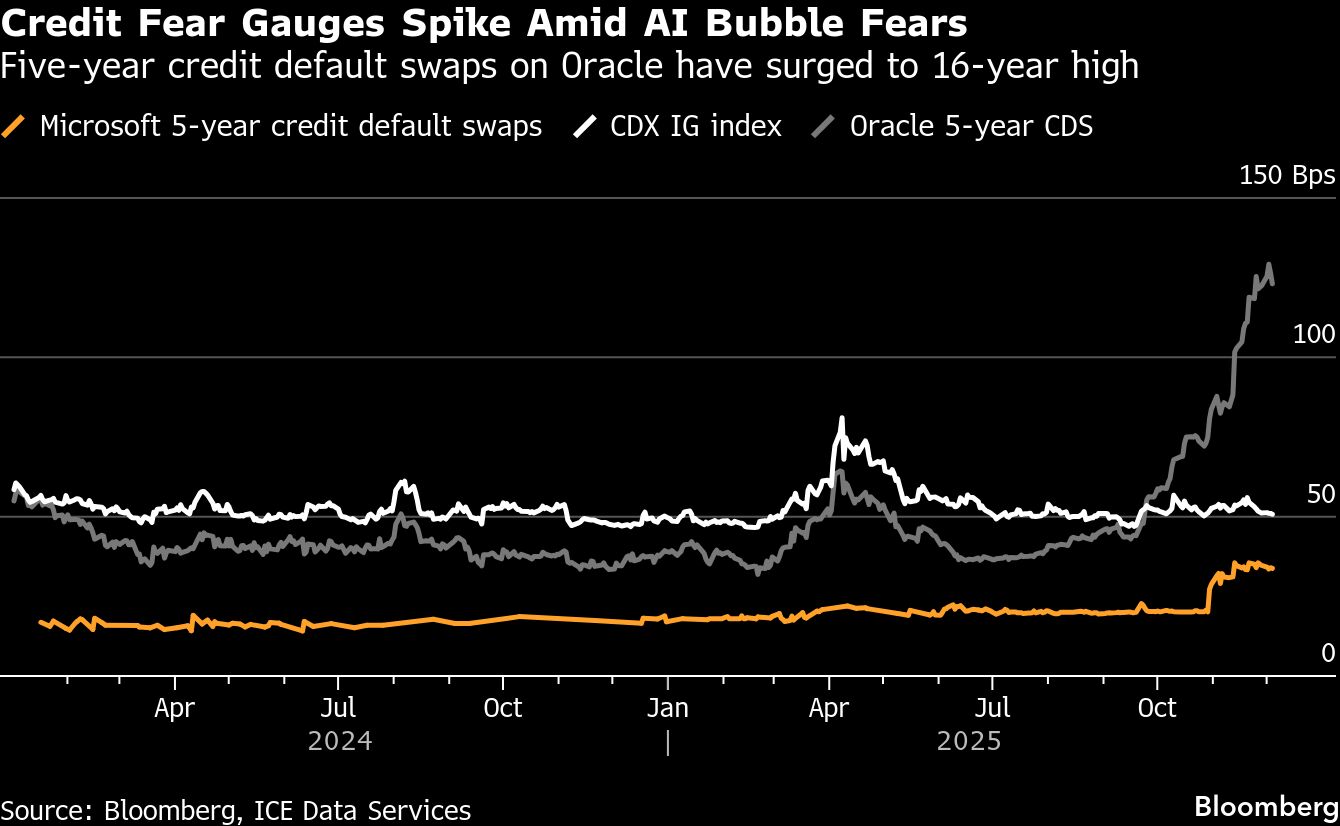

The urgency at banks to shed risk is visible all over credit markets. The cost of protecting Oracle Corp. debt against default using derivatives has risen to the highest since the global financial crisis. Morgan Stanley has looked at using a significant risk transfer—a form of insurance against loan losses—to diffuse some of the risk tied to its tech company borrowers.

Mega offerings from tech behemoths including Oracle, Meta Platforms Inc., and Alphabet Inc. have helped push global bond issuance to more than $6.46 trillion in 2025. These hyperscalers, along with electric utilities and other firms, are expected to spend at least $5 trillion as they race to build data centers and other infrastructure for a technology that’s promising to revolutionize the world’s economy.

The sums are so large that issuers will have to tap just about all major debt markets, according to JPMorgan Chase & Co. And it could take years for these tech investments to pay off—if they pay off at all. The rush has left some lenders overexposed, so they’re using a series of tools—credit derivatives, sophisticated bonds, and some newer financial products—to shift the risk of underwriting the AI boom to other investors.

“The technology is impressive, but that doesn’t mean you’re going to profit from it,” said Steven Grey, chief investment officer at Grey Value Management.

Those risks became more real last week when a major outage halted trading at CME Group Inc. and reminded investors that data center customers can leave if there are repeated breakdowns. In the aftermath, Goldman Sachs Group Inc. paused a planned $1.3 billion mortgage bond sale for CyrusOne, the data center operator.

Banks are providing the bulk of massive construction loans for data centers where Oracle is the intended tenant, which is likely driving much of the Oracle hedging, according to a recent Morgan Stanley research report. These include a $38 billion loan package and an $18 billion loan to build multiple new data center facilities in Texas, Wisconsin, and New Mexico. And banks are turning to the credit derivatives markets to reduce their exposure. Trading of Oracle’s credit default swaps ballooned to about $8 billion over the nine weeks ended November 28, according to an analysis of trade repository data by Barclays Plc credit strategist Jigar Patel. That’s up from around $350 million in the same period last year.

Prices for other swaps are climbing, too. A five-year CDS agreement to protect $10 million of Microsoft Corp. debt from default would cost about $34,000 annually, or 34 basis points (bps), on Thursday. In mid-October, it was closer to $20,000 a year.

The spread on Microsoft default swaps is remarkably wide for a AAA rated company, according to Andrew Weinberg, a portfolio manager at Saba Capital Management, a hedge fund management firm that has been selling protection. By comparison, protection on Johnson & Johnson, the other U.S. company rated AAA, cost about 19 bps a year on Thursday.

“Selling protection on Microsoft at greater than 50 percent wider levels than fellow AAA rated J&J is a remarkable opportunity,” Weinberg said. A representative for Microsoft, which hasn’t issued debt this year, declined to comment.

There are similar opportunities with Oracle, Meta, and Alphabet. Despite their large debt issuances, their credit default swaps are trading at high spreads relative to their risk of default, so selling protection makes sense, Weinberg said. Even if the companies get downgraded, the positions should perform well because they already incorporate so much potential bad news, he said.

A spokesperson for Oracle declined to comment. Spokespeople for Meta and Alphabet didn’t respond to requests for comment.

Risk Managed Through Complicated Bonds

Morgan Stanley, a key player in financing the AI race, has considered offloading some of its data center exposure via a transaction known as a “significant risk transfer,” or SRT, which can give a bank default protection for between 5 percent and 15 percent of the value of a designated portfolio of loans. SRTs often entail selling bonds known as credit-linked notes, which can have credit derivatives tied to companies or a portfolio of loans embedded in them. If the borrowers default, the bank can get a payout to cover its loss.

In this case, Morgan Stanley held preliminary talks with potential investors about an SRT tied to a portfolio of loans to businesses involved in AI infrastructure, Bloomberg reported last Wednesday. A representative for Morgan Stanley declined to comment.

“Banks are fully aware of the market’s recent concerns with possible overinvestment and overvaluation,” said Mark Clegg, a senior fixed-income trader at Allspring Global Investments, which advised on about $629 billion as of the end of September. “It should be a shock to no one that they may be exploring hedging or risk transfer mechanisms.”

Private capital firms including Ares Management Corp. have been angling to take some of banks’ exposure in SRTs tied to data centers, according to people with knowledge of the matter. The firm has been talking to banks about possible transactions, the people said. Ares declined to comment.

Banks are looking to create other products to allow them to offload credit risk tied to hyperscalers. At least two firms have tried to put together baskets of credit derivatives tied to technology companies, akin to an equity sector exchange-traded fund (ETF), according to people with knowledge of the matter. Citadel Securities started making markets for two baskets of corporate bonds from hyperscalers, allowing investors to quickly add or reduce exposure to the companies.

Adding to the urgency is the massive size of the latest debt offerings. Not too long ago, investors considered a $10 billion deal in the U.S. high-grade market to be a big one. Marketing it might have taken a few days, including investor conference calls and individual meetings with money managers. But with multi–trillion-dollar market-cap companies and funding needs in the hundreds of billions of dollars, a $10 billion sale is a “drop in the bucket,” according to Teddy Hodgson, global co-head of investment grade debt capital markets at Morgan Stanley. “We raised $30 billion for Meta in a drive-by financing,” said Hodgson, referring to bond sales that take place in a single day. “That’s not historically a commonplace event. The investor base is going to have to get used to bigger deals from the hyperscalers because of how much they’ve grown and how much this opportunity is going to cost for them to capture.”

————————————————————

Copyright 2025 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.