Commuters in the La Defense business district of Paris. Photographer: Benjamin Girette/Bloomberg.

Commuters in the La Defense business district of Paris. Photographer: Benjamin Girette/Bloomberg.

Some companies are putting debt offerings on hold after tensions between the United States and Europe over Greenland, combined with a selloff in Japanese bonds, unnerved global markets.

At least three borrowers in Europe opted to stand down, followed by at least six investment-grade and junk borrowers in the U.S., according to people familiar with the matter. The U.S. leveraged-loan market saw only six issuers on what’s effectively the week’s first day of business, a fraction of last Monday’s tally of 24 deals.

The slowdown is a dramatic shift from the frenetic pace of debt offerings seen earlier in January, typically one of the busiest months for primary markets. Before this week, credit markets seemed virtually untouchable, having shrugged off events in Venezuela and tensions in Iran. New-issue concessions dropped despite a cascade of sales.

That changed after U.S. President Donald Trump threatened to renew tariffs on some European nations if they opposed his demand for Denmark to hand over Greenland. Some issuers in Europe stood on the sidelines on Monday, when U.S. markets were closed for a public holiday. The gamble was that today would be easier for sales, but a blowout in Japanese yields added to the market’s woes and sparked a global repricing for both sovereign bonds and risk assets.

The yield on 30-year U.S. Treasuries climbed as much as 11 basis points (bps), and gauges for credit risk on both sides of the Atlantic rose, although they’re still relatively low.

“The spread widening isn’t enough to support adding risk meaningfully,” Ian Horn, a portfolio manager at Muzinich & Co Ltd. “However, we’re likely to have a steady stream of headlines from meetings in Davos, and so could see more opportunity later this week or next week.”

Indeed, JPMorgan Chase & Co. credit strategists including Eric Beinstein and Nathaniel Rosenbaum see U.S. high-grade corporate bond spreads potentially widening. A measure of perceived risk in the U.S. high-grade market, which increases when credit risk climbs, rose the most since October.

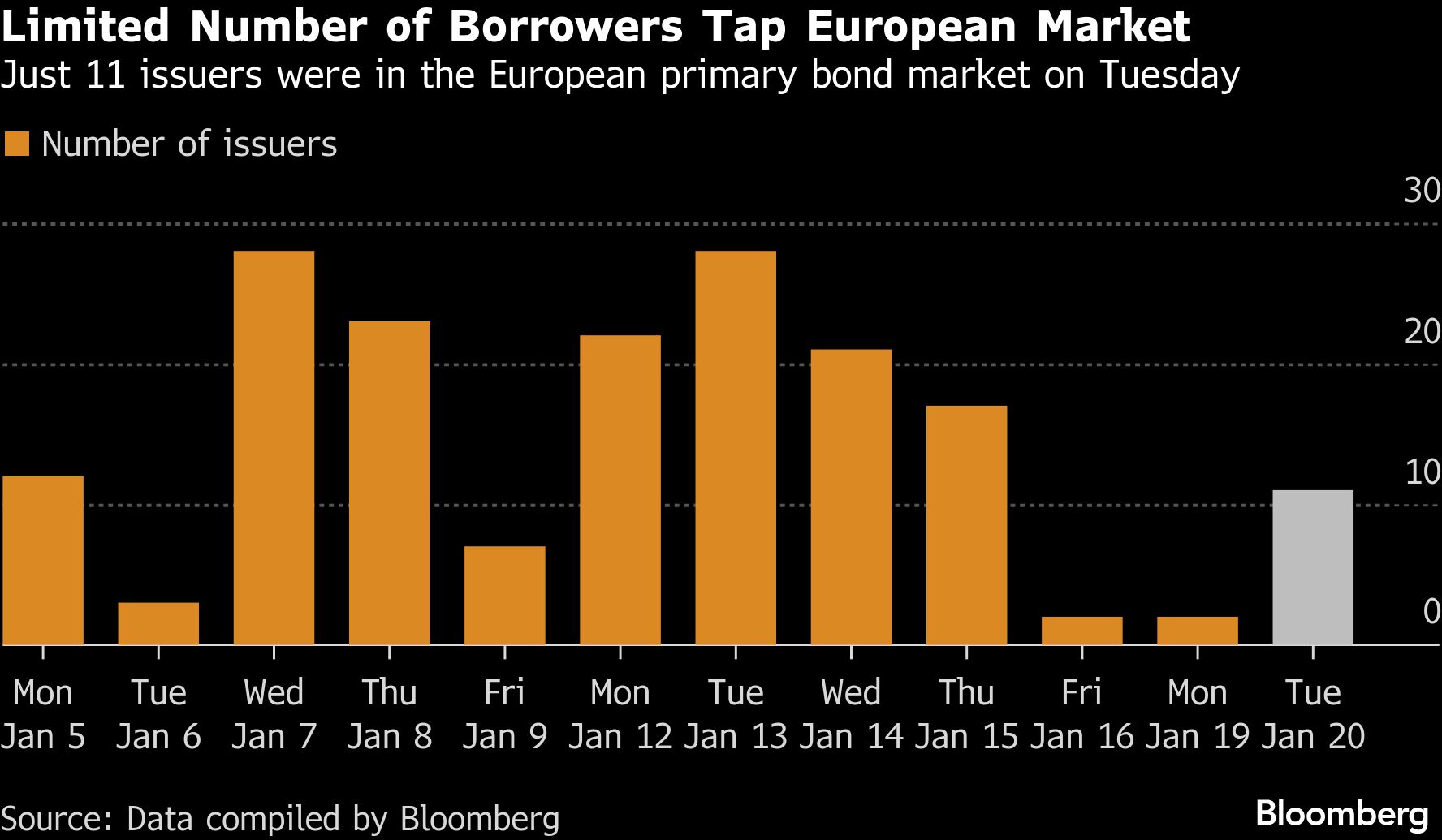

In the United States, at least four issuers are looking to raise bonds. And in Europe, where markets are winding down, 11 issuers are looking to raise at least €38.2 billion ($44.8 billion). The tally is sizable, but the majority has come from Spain’s €15 billion deal and the UK’s £7.25 billion ($9.8 billion) tap of an outstanding gilt, offerings that would have been planned long in advance. The number of issuers is about a third below an average Tuesday in January.

Just a handful of corporate issuers braved the market. BMW AG’s finance arm is selling a three-part euro deal, even though its shares slumped on Monday along with other automakers’. The tranches are offering new issue concessions from around 10 bps to more than 20 bps, well above this year’s corporate average of around 1 bps, according to calculations by Bloomberg, showing an effort to win investors over.

“Many market participants are assuming Trump will follow the playbook that we’ve seen before—high-impact initial demands, allowing him room to ‘compromise’ on a solution that’s closer to his underlying objective,” Muzinich’s Horn said. “What I think is a little different here is that we’ve seen clear and vocal opposition from other leaders. This may cause Trump to double down on his demands in a show of strength—I wouldn’t be surprised to see some escalation of rhetoric over the coming days.”

————————————————————

Copyright 2026 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.