U.S. Capitol Police outside the U.S. Capitol in Washington, D.C. on February 11.

U.S. Capitol Police outside the U.S. Capitol in Washington, D.C. on February 11.

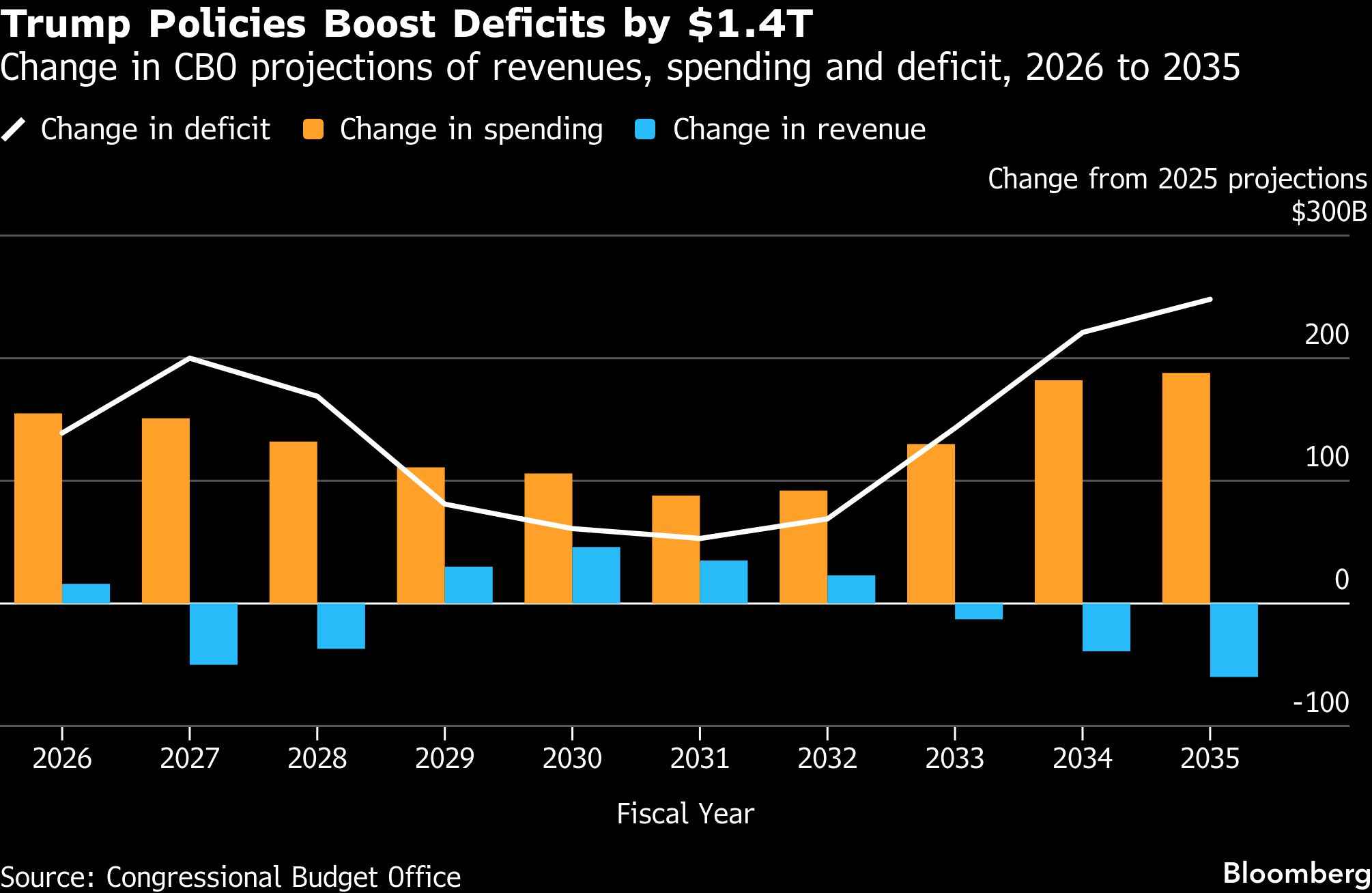

Today, the Congressional Budget Office (CBO) warned—yet again—that the United States is on an unsustainable fiscal path, jacking up its estimate of deficits for the coming decade by $1.4 trillion, thanks in part to President Donald Trump's 2025 tax law and immigration policies.

Trump's signature fiscal package from last July, which extended his 2017 tax cuts and implemented a number of new tax breaks, is estimated to increase deficits by $4.7 trillion over the next 10 years, the CBO said in a report. The administration's immigration enforcement actions are expected to add another $500 billion, it also said.

These losses in federal government revenues are projected to outweigh Trump's new import duties, which have taken the nation's average effective tariff rate above 13 percent, according to an estimate from Bloomberg Economics—the highest since at least the 1940s. The CBO projects that the increased revenue from tariffs will reduce deficits by $3 trillion—a figure that assumes U.S. trade policies in place as of November 20,2025, remain on the books throughout the coming decade. Yet tariff rates may experience significant changes in coming months and years. The Supreme Court is set to rule on whether the president exceeded his authority in imposing many of his levies, while future administrations—along with Trump himself—may shift tack.

Net outlays on interest are also expected to drive deficits higher, surging from $1 trillion in 2026 to $2.1 trillion in 2036, due to the government's large amount of debt and higher average interest rates.

Should these CBO forecasts pan out, reality would undermine the hopes of Treasury Secretary Scott Bessent, who has continued to target getting the deficit down toward 3 percent of gross domestic product (GDP) by the end of President Donald Trump's term. For 2026, the CBO boosted its deficit projection to 5.8 percent of GDP, from the 5.5 percent it had projected prior to Trump taking office. For 2028, the predicted gap is 6 percent.

And by 2036, the CBO expects, the federal government will be running a deficit equivalent to 6.7 percent of GDP. That's well above the 3.8 percent average over the past 50 years, the CBO said. Total deficits are projected to equal or exceed 5.6 percent in every year from 2026 to 2036, setting a record as deficits have not been that large for more than five consecutive years since at least 1930, when the data was first reported, the CBO report shows.

The report also shows that CBO doesn't see the administration's recipe of tax reductions, tariff hikes, and deregulation as sufficient to generate a steeper trajectory for economic growth. The agency expects U.S. economic growth to be stronger in 2026, at 2.2 percent compared with the 1.8 percent it projected in January of 2025. It then projects a moderation of growth, to 1.8 percent in 2027 and 2028 and remaining at that rate on average through 2036. That's well short of the 3 percent growth rate Bessent is targeting.

The CBO's higher expectations around this year's economic growth did extended its forecast for when the government's debt ratio will hit a record high. Last year, the agency forecast that the U.S. would hit a 107 percent debt-to-GDP ratio by 2029, exceeding the 106 percent record set in 1946, just after the end of World War II. Now the agency doesn't expect to hit that ratio until a year later, in 2030.

Inflation Expected to Get back to 2 Percent ... Eventually

Much of the rise in the federal debt is thanks to elements outside of regular annual appropriations for discretionary spending categories such as defense, housing, or homeland security. Interest on the debt has surged in recent years, while outlays for the giant entitlement programs—Social Security, Medicare, and Medicaid—have also climbed.

As high as it is, the current level of debt shouldn't pose a problem, Federal Reserve Chair Jerome Powell said last month. The challenge, however, is that the government is on "an unsustainable path." "We're running a very large deficit at essentially full employment, and so the fiscal picture needs to be addressed—and it's not really being addressed," he said in a press briefing.

Despite the predictions of unprecedented deficit-to-GDP ratios, CBO does not anticipate a significant change in the government's cost of borrowing. The agency predicts that 10-year Treasury yields will rise from an average of 4.1 percent this year to 4.4 percent, on average, in 2031 through 2036. This relatively benign outlook is due to the expectation that the aging U.S. population and slower immigration will put downward pressure on long-term interest rates, partially offsetting the impacts of rising debt, CBO Director Phillip Swagel told reporters during a press briefing today.

The agency's forecast reflects continued investor confidence in the United States, but Swagel did acknowledge the potential for higher long-term rates if the independence of the Fed comes into question amid Trump's push for the central bank to lower interest rates. "We expect the Federal Reserve to remain independent, to fulfill its mission, to meet its target," Swagel said. "All of that is built into our forecasts, into our projections. But we're cognizant of the potential if things go in the other direction, the potential for higher interest rates, and then the impact on the economy and the budget."

As for inflation, the CBO does expect annual price increases to get back to the Fed's 2 percent target in time, averaging that pace over the half-decade from 2031 to 2036. But it also sees inflation remaining stubbornly high in the immediate term, staying at 2.7 percent for this year and ticking down to 2.3 percent in 2027. "Inflation from 2026 to 2029 is now expected to be higher than the agency projected last year, mostly because of the effects of higher tariffs," the CBO said.

Unemployment is expected to rise to 4.6 percent on average in 2026.

The CBO prepared this release in December, prior to today's jobs report.

————————————————————

Copyright 2026 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.