Kevin Warsh during a news conference following a Federal Open Market Committee (FOMC) meeting in Washington, D.C., on June 17.

Kevin Warsh during a news conference following a Federal Open Market Committee (FOMC) meeting in Washington, D.C., on June 17.

It didn't take Kevin Warsh long to get the bond market's attention. Traders dumped short-term Treasuries, pushing some yields up by the most in over a year, and futures traders piled into bets on rate hikes as soon as next month, after Warsh forcefully drove home one point in his debut press conference as Federal Reserve chairman: The central bank won't tolerate high inflation.

"We're getting a message very clearly from policymakers that the rates trajectory is not lower in the near term," said Kate Moore, chief investment officer of Citi Wealth.

Before today's meeting, Wall Street had largely assumed the Fed was done cutting rates because the Iran war's oil shock has sent consumer prices surging by the most in three years. But markets had wavered over how quickly the Fed would pivot back into inflation-fighting mode. Investors also nursed some doubts about whether Warsh would give in to President Donald Trump, who elevated him to the central bank post after repeatedly lashing out at his predecessor, Jerome Powell, for not slashing rates enough.

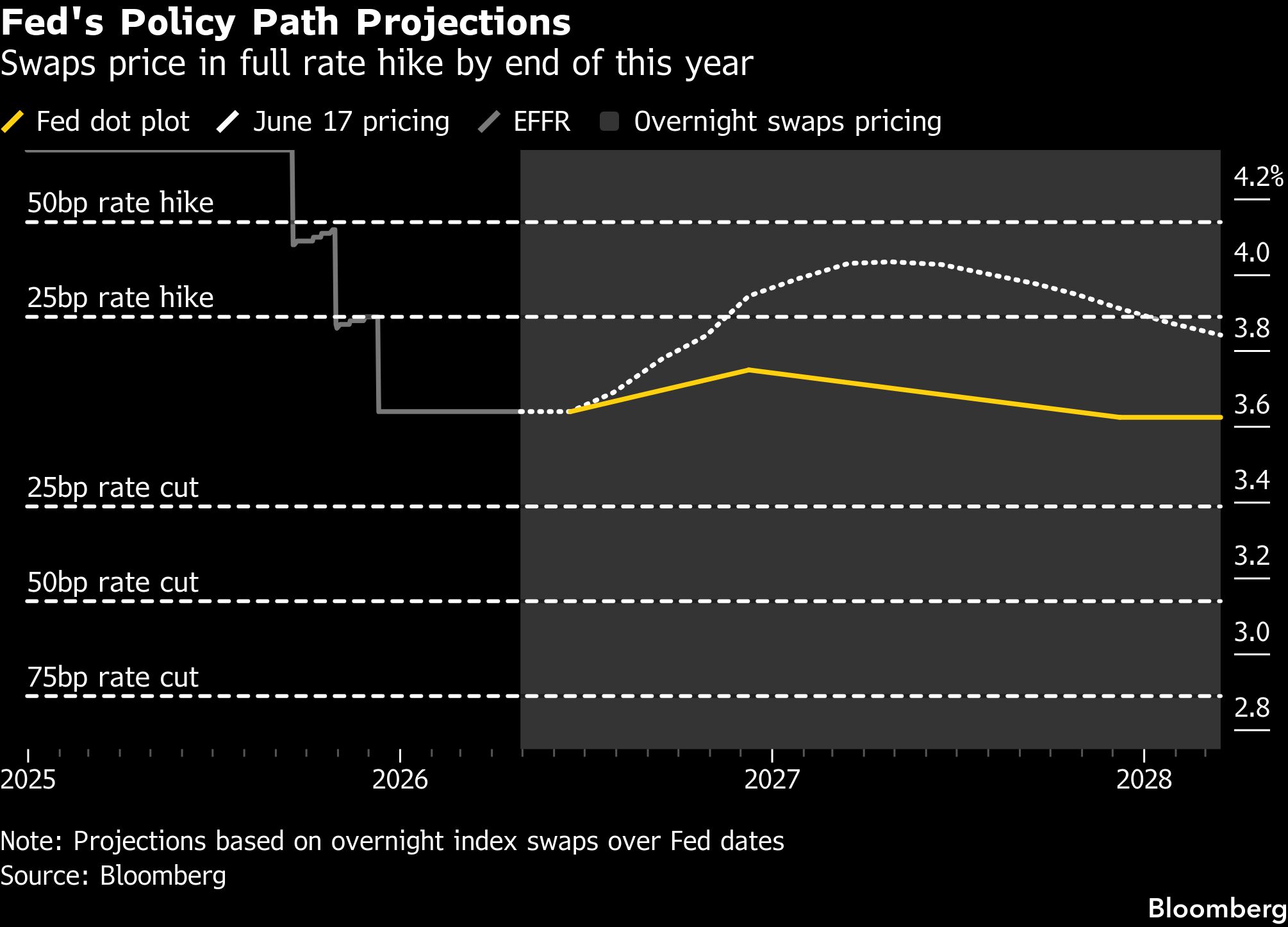

Both questions appear to be settled—at least for now—after Warsh again and again emphasized the Fed's commitment to getting inflation under control. He even criticized the central bank for its forecasting as the pace remained stuck over its 2 percent target since the pandemic. The hawkish message was driven home by the projections of individual Fed members, half of whom expect to hike rates by the end of the year.

"If nothing else, the market has renewed confidence in the Fed's inflation fighting ability and conviction," said Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets. "It was a good day for central banking independence."

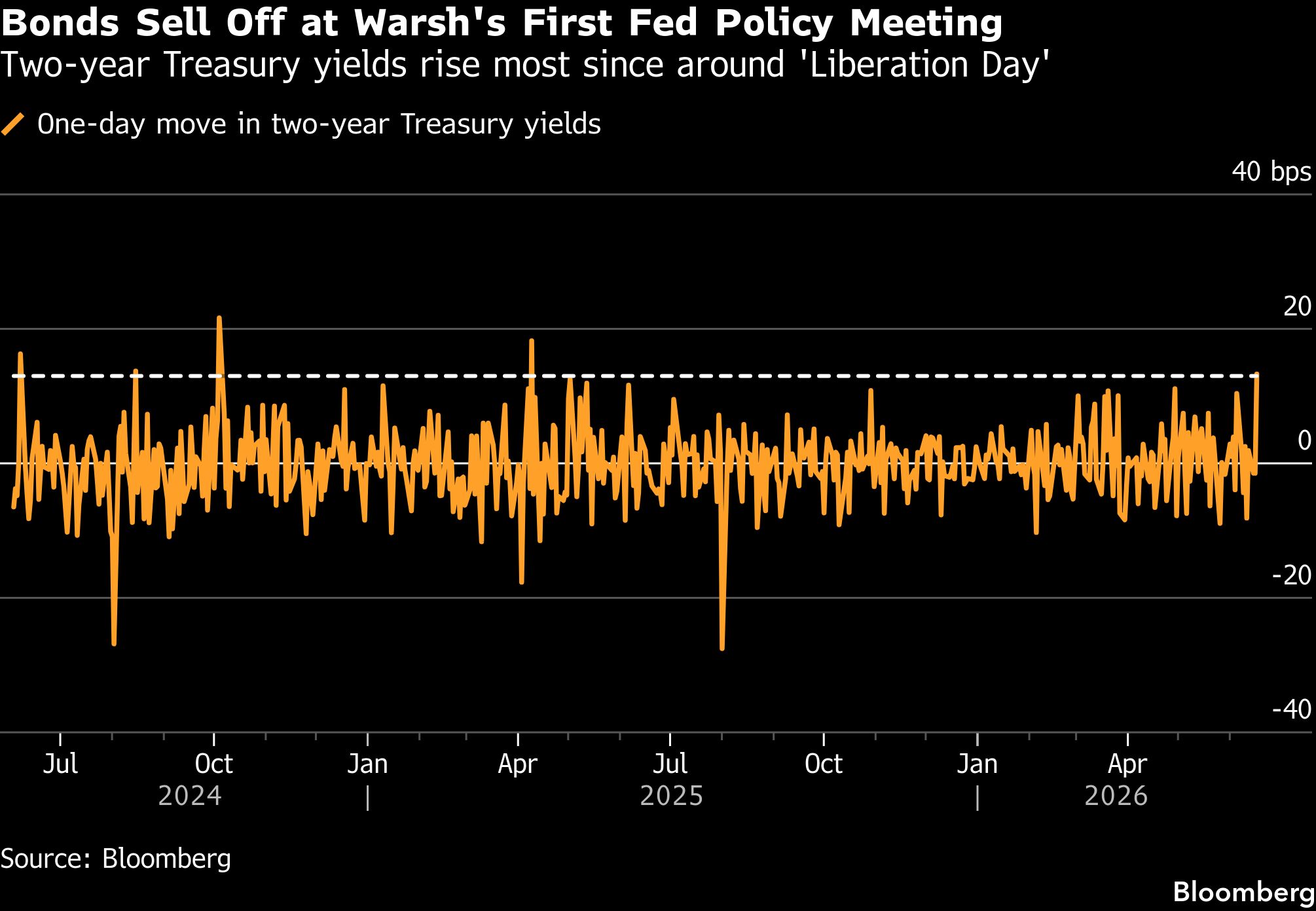

The Fed's message triggered waves of repositioning in markets as traders rushed to get ahead of its moves. Two-year Treasury yields, which closely track expectations for monetary policy, shot up 13 basis points (bps), the biggest jump since April 2025. That matched the largest increase on a Fed meeting day since 2008. At the same time, futures traders started fully pricing in a quarter-point rate hike by October, just before the midterm elections, if not sooner. And 30-year Treasuries rose, pulling their yields down, in a sign of faith that inflation will ultimately be contained over the long haul.

The movements cap what has been a stark shift in the market's expectations for the direction of interest rates over the past few months, one that's persisting even as oil prices pull back while the U.S. and Iran move closer to ending the war.

But energy prices have only been one factor keeping inflation stubbornly above the Fed's target. Job growth has picked up and the economy has remained surprisingly resilient, bucking periodic calls that an recession was on the horizon. The record-setting stock market rally has bolstered consumer spending, helping to offset the hit of higher gas prices. And the artificial intelligence (AI) boom has unleashed a flood of investment spending by big tech companies.

Warsh didn't commit to raising rates, and—after the Fed held rates steady again today—indicated he saw little reason to try forecasting such moves in advance. He also largely sidestepped a question on why the Fed didn't go ahead and raise rates now, given that inflation is so high, and characterized the bank's internal deliberations as "a good family fight."

James St. Aubin, chief investment officer at Ocean Park Asset Management, said Warsh was trying to strike a balance by reassuring the market that he won't jeopardize the Fed's credibility while, at the same time, not drawing Trump's ire. In that sense, Warsh didn't leave himself boxed in. "He's really just trying to appease two masters," he said. "He's walking a fine line."

Warsh's takeover of the Fed came after it was subject to an unprecedented pressure campaign by the Trump administration, which included an effort to oust Governor Lisa Cook and a criminal investigation that Powell said was in retaliation for not bending monetary policy to the president's will.

Warsh was a staunch inflation hawk during his term as Fed governor between 2006 and 2011, when the housing-market collapse drove the United States into a deep recession. Yet he had gone on to become a fierce critic of the central bank and last year faulted it for continuing to forecast elevated inflation, saying AI will unleash a "significant disinflationary force" by increasing productivity, casting some doubts on his current views.

Nevertheless, the position he staked out at his maiden press conference underscored that the Fed's focus is shifting back to its its mandate to combat inflation after nudging rates down in late 2024 and again at the end of last year.

"This was a very solid debut for Warsh," said Win Thin, chief economist at Bank of Nassau 1982. "The key takeaway is that the Fed has become much more willing to hike rates in the second half of the year. "

————————————————————

Copyright 2026 Bloomberg. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

© Arc, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to TMSalesOperations@arc-network.com. For more information visit Asset & Logo Licensing.