Corporate treasurers around the world will soon find themselves staring down deflation. Misunderstood by almost everyone, maligned by governments and central banks, and basically absent from the Western world for generations, deflation may be the most challenging environment in which businesses can operate. It is also an environment that highlights the vital importance of treasurers and financial risk managers—not only in mitigating losses, but also in helping businesses take advantage of opportunities that may arise.

The Corona Crash of 2020 (as February and March will likely become known) broke a number of records. U.S. stock markets declined at the fastest rate in history; the S&P 500 index fell by 30 percent in only 22 days. That same period also witnessed the quickest-ever rise in yield spreads in credit markets. Central banks and governments pumped trillions of dollars, euros, pounds, and yuan into financial markets to prevent a complete systemic failure. Even so, some corners of the credit markets seized up and may never return.

Why did this happen? The deliberate shutdown of huge swaths of the global economy, to prevent the spread of Covid-19, undoubtedly exacerbated the panic in financial and commodity markets. But it didn't cause the crash. To understand the cause of both the crash and the deflationary environment that we expect will follow, we need to go back and examine the definition of—and the key precondition for—deflation.

Deflation Defined

It is vitally important to understand the difference between a simple decline (or increase) in prices and actual monetary deflation (or inflation). The former describes what is happening to prices for a basket of consumer goods, but the monetary definition describes what is happening to money and credit across an economy.

In the 16th century, Nicolaus Copernicus and followers of the School of Salamanca noted that the overall prices of goods increased as traders brought gold and silver back from the Americas to Europe. That observation led to the "quantity theory of money," which hypothesizes a link between the prices of goods and the quantity of money and credit in an economy. Economists still argue over the exact nature of that link, but it's worth noting that the terms "deflation" and "inflation" were coined in reference to the money/credit side, not the price side.

Today, prices across an economy are generally believed to move in concert with its total supply of money and credit, multiplied by the "velocity" of money—in other words, the speed with which money circulates to support purchases. The true definition of "deflation" is a contraction in the total supply of money and credit in an economy. Consumer and producer prices generally fall during periods of deflation, but they can fall for other reasons as well, such as a production glut.

The Primary Precondition of Deflation: Met

Because deflation is a contraction in money and credit, it logically follows that deflation would occur only after a major societal buildup in the extension of credit and the simultaneous assumption of debt. In a 1957 letter, Hamilton Bolton, an expert in bank credit and the Elliott wave principle (a model of financial market cycles based on patterns of crowd psychology), summarized his observations this way:

"In reading a history of major depressions in the U.S. from 1830 on, I was impressed with the following:

- All were set off by a deflation of excess credit. This was the one factor in common.

- Sometimes the excess-of-credit situation seemed to last years before the bubble broke.

- Some outside event, such as a major failure, brought the thing to a head, but the signs were visible many months, and in some cases years, in advance.

- None was ever quite like the last, so that the public was always fooled thereby.

- Some panics occurred under great government surpluses of revenue (1837, for instance) and some under great government deficits.

- Credit is credit, whether non–self-liquidating or self-liquidating.

- Deflation of non-self-liquidating credit usually produces the greater slumps."

"Self-liquidating credit" is a loan that is repaid, with interest, in a moderately short time utilizing the financial returns generated by the production of goods or services that the loan makes possible. The full transaction adds value to the economy. "Non–self-liquidating credit" is a loan that is not tied to production. When financial institutions lend money to consumers for purchases of cars, boats, or homes—or for speculative purchases of stock certificates and financial derivatives, for example—no production activities are directly tied to the loan. Interest payments on such loans must come from other sources of income, and in the aggregate—contrary to a belief that is nearly ubiquitous—such lending adds costs to the economy, not value.

Over the past few decades, a number of developed economies, including the United States, have seen the momentum of their economic growth slow. At the same time, the total value of debt in these economies has exploded, not just in nominal terms but as a percentage of gross domestic product (GDP). Most of this debt was self-liquidating in the early 1980s, but as the bull market matured, non–self-liquidating debt became predominant.

By the end of 2019, global debt stood at more than $255 trillion, according to the Institute of International Finance (IIF). Global debt as a percentage of GDP had reached 322 percent, which is actually 40 percentage points higher than at the start of the Great Financial Crisis in 2008. Non-financial corporate debt, including both corporate bonds in general and non–self-liquidating debt, has surged in the past decade, a lot of it in the form of borrowing to finance unproductive share buybacks and leveraged buyouts.

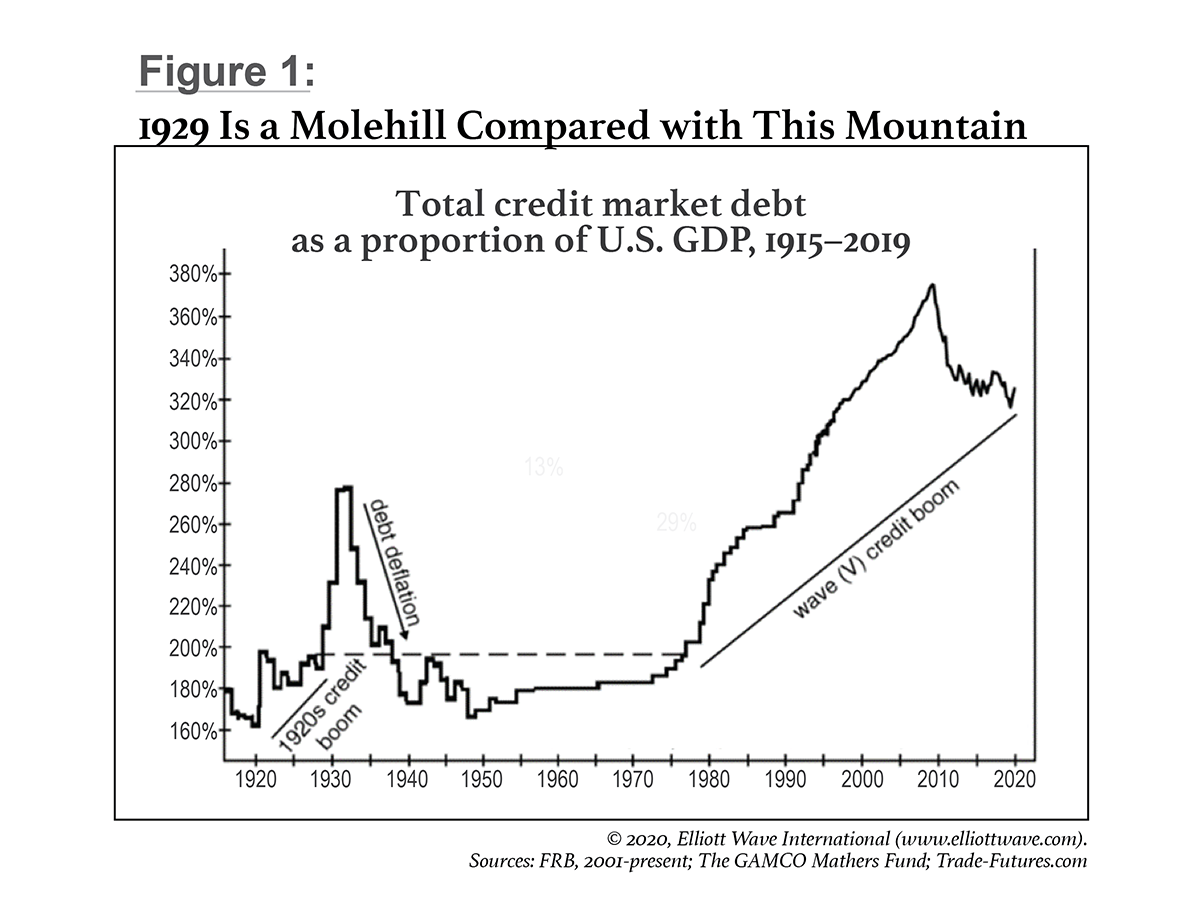

Figure 1 shows the history of borrowing in the United States over the past century. Today's debt bubble, as a percentage of GDP, is far greater than the bubble whose deflation coincided with the Great Depression. The debt-to-GDP ratio is down from its peak in 2009, much as it receded slightly in the late 1920s when a financial boom temporarily juiced the economy. However, as the response to Covid-19 sends GDP plunging, this ratio will soar, just as it did in the early 1930s. After that, history suggests, the full wrath of credit deflation will be unleashed.

Why Central Banks Can't Prevent Deflation

It would be hard to overstate the degree to which psychology drives an economy's shift to deflation. When the prevailing economic mood in a nation changes from optimism to pessimism, creditors, debtors, investors, producers, and consumers all change their primary orientation from expansion to conservation. As creditors become more conservative, they slow their lending. As potential debtors become more conservative, they borrow less or not at all. As investors become more conservative, they commit less money to debt investments. As producers become more conservative, they reduce expansion plans. And as consumers become more conservative, they save more and spend less.

These behaviors reduce the velocity of money, which puts downward pressure on prices. Money velocity has already been slowing for years, a classic warning sign that deflation is impending. Now, thanks to the virus-related lockdowns, money velocity has begun to collapse. As widespread pessimism takes hold, expect it to fall even further.

In addition to the psychological drivers, there are structural underpinnings of deflation as well. A financial system's ability to sustain increasing levels of credit rests upon a vibrant economy. A high-debt situation becomes unsustainable when the rate of economic growth falls beneath the prevailing rate of interest owed. As the slowing economy reduces borrowers' ability to pay what they owe, creditors may refuse to underwrite interest payments on existing debt by extending even more credit. When the burden becomes too great for the economy to support, defaults rise. Moreover, fear of defaults prompts creditors to reduce lending even further.

The resulting cascade of debt liquidation leads to a deflationary crash. In desperately trying to raise cash to pay off loans, borrowers bring all kinds of assets to market, including stocks, bonds, commodities, and real estate, causing the prices of these assets to plummet. The cycle ends only after the supply of credit falls to a level at which the surviving creditors are satisfied with the collateralization borrowers have to offer.

The resulting cascade of debt liquidation leads to a deflationary crash. In desperately trying to raise cash to pay off loans, borrowers bring all kinds of assets to market, including stocks, bonds, commodities, and real estate, causing the prices of these assets to plummet. The cycle ends only after the supply of credit falls to a level at which the surviving creditors are satisfied with the collateralization borrowers have to offer.

Recognizing the role of psychology in this cycle is vital to understanding why no amount of intervention by governments and central banks can prevent deflation. Unfortunately, because society at large thinks of deflation as an economic condition we should fear, central banks borrow and print money to avoid it. That's what some are doing right now, through programs ranging from quantitative easing to sending citizens checks in the mail. As they do so, they are increasing the volume of base money in their economies. However, the deflation that we see coming will result from a swift contraction in credit, not base money. And even the trillions of dollars central banks are injecting into the money supply are insignificant compared with the total amount of credit in the global economy.

Consider the situation in the United States. In 2008, the U.S. monetary base was less than $900 billion. Then, in response to the Great Recession, the Fed started printing vast amounts of money. Today, the U.S. monetary base is around $3.8 trillion. This fourfold increase is remarkable—but compare it with total U.S. debt, which statista.com pegged at $72 trillion at the end of 2018. Add in derivatives, which are just another form of credit (I owe you $X if Y happens), and the number is much higher. While we have found no reliable source of U.S.-only derivatives exposure, at a global level, total credit can be estimated to be in the range of $1.1 quadrillion to $1.8 quadrillion. Quadrillion—in other words, a thousand trillion.

The deflation of such a stupendous amount of debt will overwhelm everything in its path. The U.S. Federal Reserve and other central banks are so desperate to avoid deflation that they are buying up toxic loans and junk bonds. In the long term, these debts must be repaid with tax revenues. And in a deflationary depression, tax revenues also plummet.

Central banks cannot prevent deflation. The Bank of Japan and the Japanese government have spent decades injecting money into that nation's economy, even buying huge amounts of stocks directly—in effect, nationalizing the stock market—to no avail. Private debt as a percentage of GDP in Japan is still declining from its peak nearly three decades ago, and consumer prices remain stagnant. When the massive credit bubble we're currently riding deflates, the size of government debt will only exacerbate economic problems in the U.S. and beyond.

From Surviving to Thriving

The key to survival in a period of deflation is to have as little debt as possible. Over the years, economists who have warned of the consequences of credit expansion, such as Austrians Ludwig von Mises and Friedrich Hayek, have mostly been ignored. However, debt becomes even more of a burden for businesses in a deflationary economy.

Think about a scenario in which Company A has bought Company B for $100 million and funded the transaction by issuing $75 million in debt. A deflationary environment might reduce the value of Company B's business to, say, $50 million. At the time of the acquisition, Company A took on debt worth 75 percent of the value of the asset it funded. Now, the same debt is worth 150 percent of the asset's value.

Even self-liquidating credit becomes burdensome in deflation. Suppose Company C borrows money to invest in a new widget-making machine. Under normal economic conditions, the expected return on selling extra widgets would compensate for the added debt, making the whole transaction viable. In a deflationary economy, however, the pessimistic social mood leads to stagnant or negative economic growth and demand for widgets declines. The debt-funded investment in new machinery cannot pay for itself.

Turnover is vanity and profit is sanity, but cash is king. Corporate treasurers and financial risk managers should inherently understand the wisdom in this age-old saying. Cash is not only the ultimate hedge, but also the only investment that rises in value during deflation. As stocks, bonds, real estate, and commodities are all losing value, the amount of cash required to purchase these assets is falling, by definition. In other words, the relative value of cash is going up.

Most people tend to gauge the value of cash according to the interest rate it can earn. Short-term interest rates in the major currencies will probably remain close to zero for the foreseeable future. Don't be fooled into thinking that this means a large cash holding is a wasted asset. On the contrary, as the vice-like grip of deflation takes hold, a company with significant cash reserves will be able to take advantage of the increasing numbers of opportunities that will present themselves.

Tightening credit and falling prices are natural byproducts of a normal business cycle. They are also indicative of an environment in which cash-rich companies will be able to buy some businesses and productive resources at bargain-basement prices. For companies with a substantial debt burden, deflation may mean a struggle to survive. But those that have made cash king can leverage the situation to gain even stronger competitive positioning when the cycle turns again and the economic recovery starts.

Murray Gunn is head of global research at Elliott Wave International (EWI) and the lead contributor to deflation.com. In his 30-year career, he has worked as a fund manager in global bonds, currencies, and stocks, including long posts at Standard Life Investments and the Abu Dhabi Investment Authority. Prior to EWI, he was head of technical analysis with HSBC Bank.

Murray Gunn is head of global research at Elliott Wave International (EWI) and the lead contributor to deflation.com. In his 30-year career, he has worked as a fund manager in global bonds, currencies, and stocks, including long posts at Standard Life Investments and the Abu Dhabi Investment Authority. Prior to EWI, he was head of technical analysis with HSBC Bank.