Regulatory oversight has intensified over the past few years for financial institutions around the world, and it's starting to have an impact on these institutions' business.

The Basel III framework will require banks to maintain a Tier 1 capital reserve equivalent to 7 percent of the value of their risk-weighted assets, and to maintain liquid assets equivalent to 30 days' worth of cash outflows. Solvency II places new capital requirements on insurance providers. In the United States, the Dodd-Frank Act requires periodic stress testing for many financial services providers, as well as placing tight restrictions on derivatives trading. At the same time, the European Market Infrastructure Regulation (EMIR) and Markets in Financial Instruments Directive (MiFID) are changing the regulatory landscape for European financial markets.

As lawmakers and regulators continue to sort out the details of these and other rules, many banks have begun reconsidering their risk management and compliance processes. The actions they take may result in changes to the pricing of their products and/or services, as well as changes to the portfolio of products/services they offer customers.

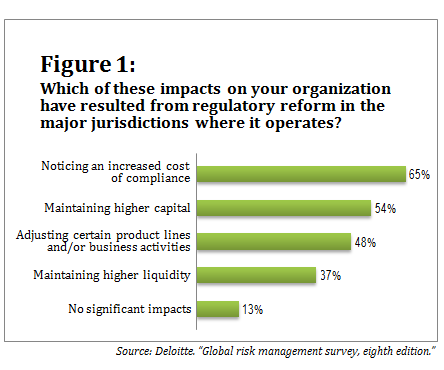

A recent survey by Deloitte of chief risk officers, or their equivalent, in global financial services companies found that 87 percent of these organizations are feeling significant impacts of the regulatory reforms in the major jurisdictions in which they operate. Nearly two-thirds are noticing an increase in the cost of compliance. More than half are holding higher levels of capital, and 37 percent are maintaining higher liquidity, to comply with new regulations. And 48 percent are adjusting their products lines and/or business activities. (See Figure 1.)

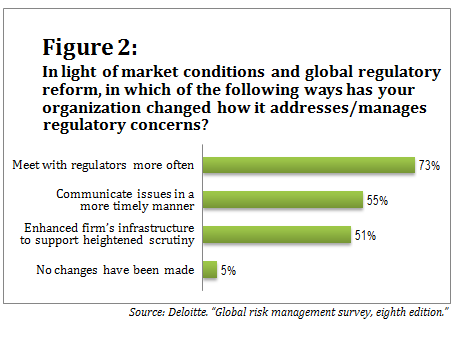

Survey respondents cite several factors as driving these changes. Almost three-quarters now meet with regulators more frequently than they used to, and more than half have enhanced their IT infrastructure. Only 5 percent of respondents have made no changes to the ways in which they manage regulatory concerns. (See Figure 2, below.)

Only time will tell how regulatory reforms in the financial services sector will affect banking and insurance customers over the long term. But it's likely that prices will rise and choices will decline, at least in certain financial services product lines.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.